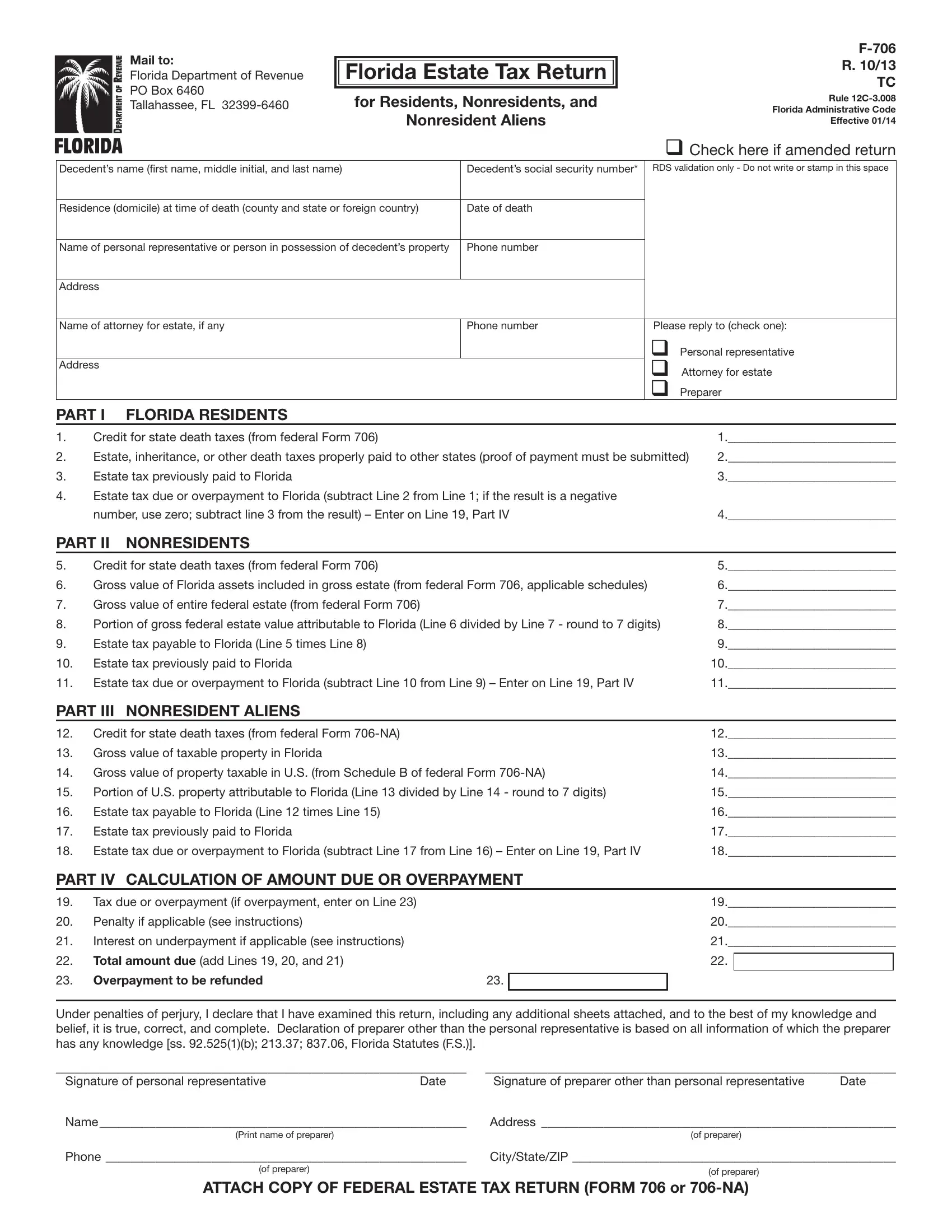

When it comes to estate management in Florida, understanding the intricacies of the Florida F 706 form, officially known as the Florida Estate Tax Return, is crucial for residents, nonresidents, and nonresident aliens alike. Mailed to the Florida Department of Revenue, this form serves as a cornerstone for those navigating the complexities of estate taxes within the state. Its significance is underscored by the varied sections it encompasses, such as credits for state death taxes, computation of estate tax due or overpayment, and specific segments dedicated to both residents and nonresidents—each tailored to address the unique scenarios faced by different estate profiles. Furthermore, it touches upon critical details like penalties, interest on underpayments, and the process for amending a filed return. Clarity on deadlines, the necessity of attaching a copy of the federal estate tax return (Form 706 or 706-NA), and guidelines for requesting extensions highlight the form's comprehensive nature. Notably, it also sheds light on the state's approach to social security numbers, emphasizing privacy and confidentiality in tax administration. As the F-706 form intertwines with federal estate tax requirements, understanding its nuances becomes indispensable for ensuring compliance and maximizing potential tax advantages under Florida law, hence making it an essential document for estate planners and personal representatives tasked with estate administration.

| Question | Answer |

|---|---|

| Form Name | Florida Form F 706 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | f706, 706 estate return residents form, f 706 tax return form, florida f estate tax get |

Mail to:

Florida Department of Revenue

PO Box 6460

Tallahassee, FL

|

||

Florida Estate Tax Return |

R. 10/13 |

|

TC |

||

|

||

for Residents, Nonresidents, and |

Rule |

|

Florida Administrative Code |

||

|

||

Nonresident Aliens |

Effective 01/14 |

q Check here if amended return

Decedent’s name (first name, middle initial, and last name) |

Decedent’s social security number* |

RDS validation only - Do not write or stamp in this space |

|

|

|

Residence (domicile) at time of death (county and state or foreign country) |

Date of death |

|

|

|

|

Name of personal representative or person in possession of decedent’s property |

Phone number |

|

|

|

|

Address |

|

|

|

|

|

Name of attorney for estate, if any |

Phone number |

Please reply to (check one): |

|

|

q Personal representative |

Address |

|

q Attorney for estate |

|

|

|

|

|

q Preparer |

PART I FLORIDA RESIDENTS

1. |

Credit for state death taxes (from federal Form 706) |

1.___________________________ |

2. |

Estate, inheritance, or other death taxes properly paid to other states (proof of payment must be submitted) |

2.___________________________ |

3. |

Estate tax previously paid to Florida |

3.___________________________ |

4.Estate tax due or overpayment to Florida (subtract Line 2 from Line 1; if the result is a negative

|

number, use zero; subtract line 3 from the result) – Enter on Line 19, Part IV |

4.___________________________ |

|||||

PART II |

NONRESIDENTS |

|

|

|

|

|

|

5. |

Credit for state death taxes (from federal Form 706) |

|

|

5.___________________________ |

|||

6. |

Gross value of Florida assets included in gross estate (from federal Form 706, applicable schedules) |

6.___________________________ |

|||||

7. |

Gross value of entire federal estate (from federal Form 706) |

|

|

7.___________________________ |

|||

8. |

Portion of gross federal estate value attributable to Florida (Line 6 divided by Line 7 - round to 7 digits) |

8.___________________________ |

|||||

9. |

Estate tax payable to Florida (Line 5 times Line 8) |

|

|

9.___________________________ |

|||

10. |

Estate tax previously paid to Florida |

|

|

10.___________________________ |

|||

11. |

Estate tax due or overpayment to Florida (subtract Line 10 from Line 9) – Enter on Line 19, Part IV |

11.___________________________ |

|||||

PART III |

NONRESIDENT ALIENS |

|

|

|

|

|

|

12. |

Credit for state death taxes (from federal Form |

|

|

12.___________________________ |

|||

13. |

Gross value of taxable property in Florida |

|

|

13.___________________________ |

|||

14. |

Gross value of property taxable in U.S. (from Schedule B of federal Form |

14.___________________________ |

|||||

15. |

Portion of U.S. property attributable to Florida (Line 13 divided by Line 14 - round to 7 digits) |

15.___________________________ |

|||||

16. |

Estate tax payable to Florida (Line 12 times Line 15) |

|

|

16.___________________________ |

|||

17. |

Estate tax previously paid to Florida |

|

|

17.___________________________ |

|||

18. |

Estate tax due or overpayment to Florida (subtract Line 17 from Line 16) – Enter on Line 19, Part IV |

18.___________________________ |

|||||

PART IV CALCULATION OF AMOUNT DUE OR OVERPAYMENT |

|

|

|

||||

19. |

Tax due or overpayment (if overpayment, enter on Line 23) |

|

|

19.___________________________ |

|||

20. |

Penalty if applicable (see instructions) |

|

|

20.___________________________ |

|||

21. |

Interest on underpayment if applicable (see instructions) |

|

|

21.___________________________ |

|||

22. |

Total amount due (add Lines 19, 20, and 21) |

|

|

22. |

|

|

|

|

|

|

|

||||

23. |

Overpayment to be refunded |

23. |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare that I have examined this return, including any additional sheets attached, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer other than the personal representative is based on all information of which the preparer has any knowledge [ss. 92.525(1)(b); 213.37; 837.06, Florida Statutes (F.S.)].

__________________________________________________________________ |

__________________________________________________________________ |

||

Signature of personal representative |

Date |

Signature of preparer other than personal representative |

Date |

Name___________________________________________________________ |

Address _________________________________________________________ |

||

(Print name of preparer) |

|

(of preparer) |

|

Phone __________________________________________________________ |

City/State/ZIP ____________________________________________________ |

||

(of preparer) |

|

(of preparer) |

|

|

|

|

|

ATTACH COPY OF FEDERAL ESTATE TAX RETURN (FORM 706 or

INSTRUCTIONS FOR FORM

R.10/13 Page 2

General Information

Florida’s estate tax is based on the allowable federal credit for state death taxes. Florida tax is imposed only on those estates subject to federal estate tax filing requirements and entitled to a credit for state death taxes (Chapter 198, F.S.). Estate tax is not due if a federal estate tax return (Form 706 or

Form

The requirement to file Form

Date of Death |

|

|

|

On or before December 31, 2004 |

Yes** |

|

|

On or after January 1, 2005 |

No |

|

|

**If required, Form

Due Dates and Extensions of Time

Form

us within 30 days of mailing the request and 30 days of receiving the federal approval. An extension of time to file does not extend the time to pay. Interest accrues on the Florida tax due from the original due date until paid.

Tax Paid to Other States

For Florida residents: if estate, inheritance, or other death taxes were properly paid to other states, proof of payment must be submitted to the Florida Department of Revenue. (Proof of payment means the final certificate of payment showing the specific amounts of tax, penalty, or interest assessed and paid.)

*Social Security Numbers

Social security numbers (SSNs) are used by the Florida Department of Revenue as unique identifiers for the administration of Florida’s taxes. SSNs obtained for tax administration purposes are confidential under sections 213.053 and 119.071, Florida Statutes, and not subject to disclosure as public records. Collection of your SSN is authorized under state and federal law. Visit our Internet

site at floridarevenue.com and select “Privacy Notice” for more information regarding the state and federal law governing the collection, use, or release of SSNs, including authorized exceptions.

Where to File

Mail your completed

Tallahassee, FL

If you are requesting a nontaxable certificate, include the $5.00 fee.

Signature

The personal representative must sign the return declaration under penalties of perjury. If someone else prepares the return, the preparer must also sign the return.

Amending Form

If you must change a return that has already been filed, you must complete another Form

Penalties and Interest

Penalties – If tax is not paid by the due date (or approved extension date) a late payment penalty of 10% of the unpaid tax is due. After 30 days, the late penalty increases to 20%. An added penalty of 10% per month up to a maximum of 50% of the tax due is imposed if the unpaid tax is due to negligence or intentional disregard. A fraud penalty of 100% of the tax due is imposed if the unpaid tax is due to willful intent to defraud. However, the Department of Revenue is authorized to compromise or settle these penalties pursuant to section 213.21, F.S.

Interest – Interest is due on late payments from the due date until paid. Interest rates are updated January 1 and July 1 of each year. To obtain current interest rates, visit our website at floridarevenue.com.

Need Assistance?

Information and forms are available on our Internet site at

floridarevenue.com.

If you have any questions, you may contact Taxpayer Services at

For a written reply to your tax questions, write:

Taxpayer Services MS

Florida Department of Revenue

5050 W Tennessee St

Tallahassee, FL

For federal estate tax information or forms, visit the IRS website at www.irs.gov.