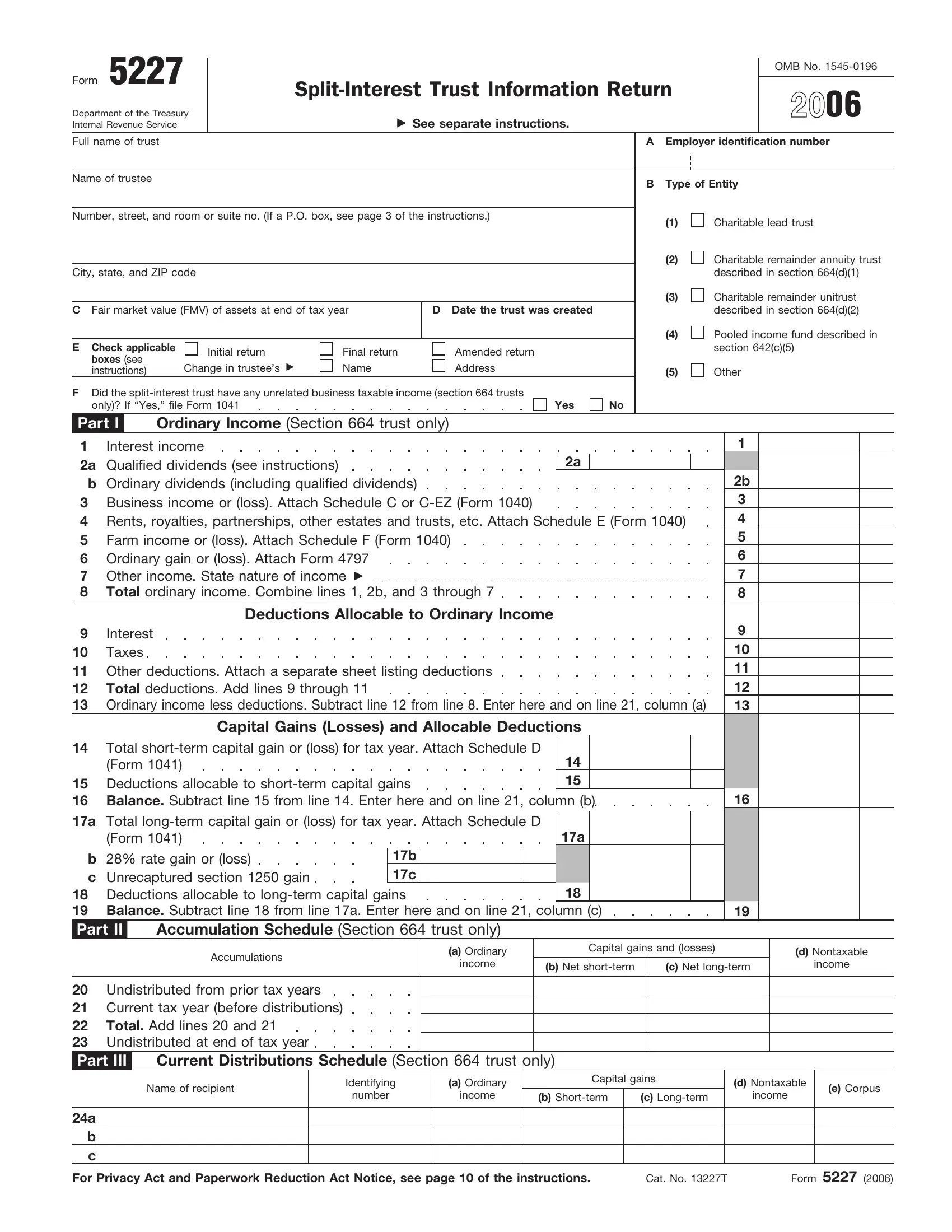

The Form 5227, titled Split-Interest Trust Information Return, serves as a critical document for managing the unique reporting requirements posed by split-interest trusts within the United States. Managed by the Department of the Treasury and overseen by the Internal Revenue Service (IRS), this form encompasses a detailed accounting of a trust's income, deductions, distributions, and balances for the tax year in question. It is meticulously designed to capture the specific data on charitable lead trusts, charitable remainder annuity trusts, charitable remainder unitrusts, pooled income funds, and other similar entities falling under section 664. The form outlines not just the ordinary income and deductions allocable to such income but extends to detail capital gains or losses alongside respective allocations. Moreover, it delves into intricacies such as the accumulation schedule for section 664 trusts, showcasing undistributed amounts from prior years alongside current tax year accumulations before any distributions. The document also probes into the distributions made over the course of the tax year, emphasizing the breakdown between beneficiaries on a granular scale. Form 5227's comprehensive approach to reporting is further exemplified in Part IV, which meticulously lays out the trust's balance sheet, capturing everything from cash and investments to liabilities and net assets. This level of detail ensures that both the IRS and the trusts involved have a clear, nuanced understanding of the financial movements and obligations affecting the charitable and financial landscape within a given tax period.

| Question | Answer |

|---|---|

| Form Name | Form 5227 |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | f5227 form 5227 for 2012 |