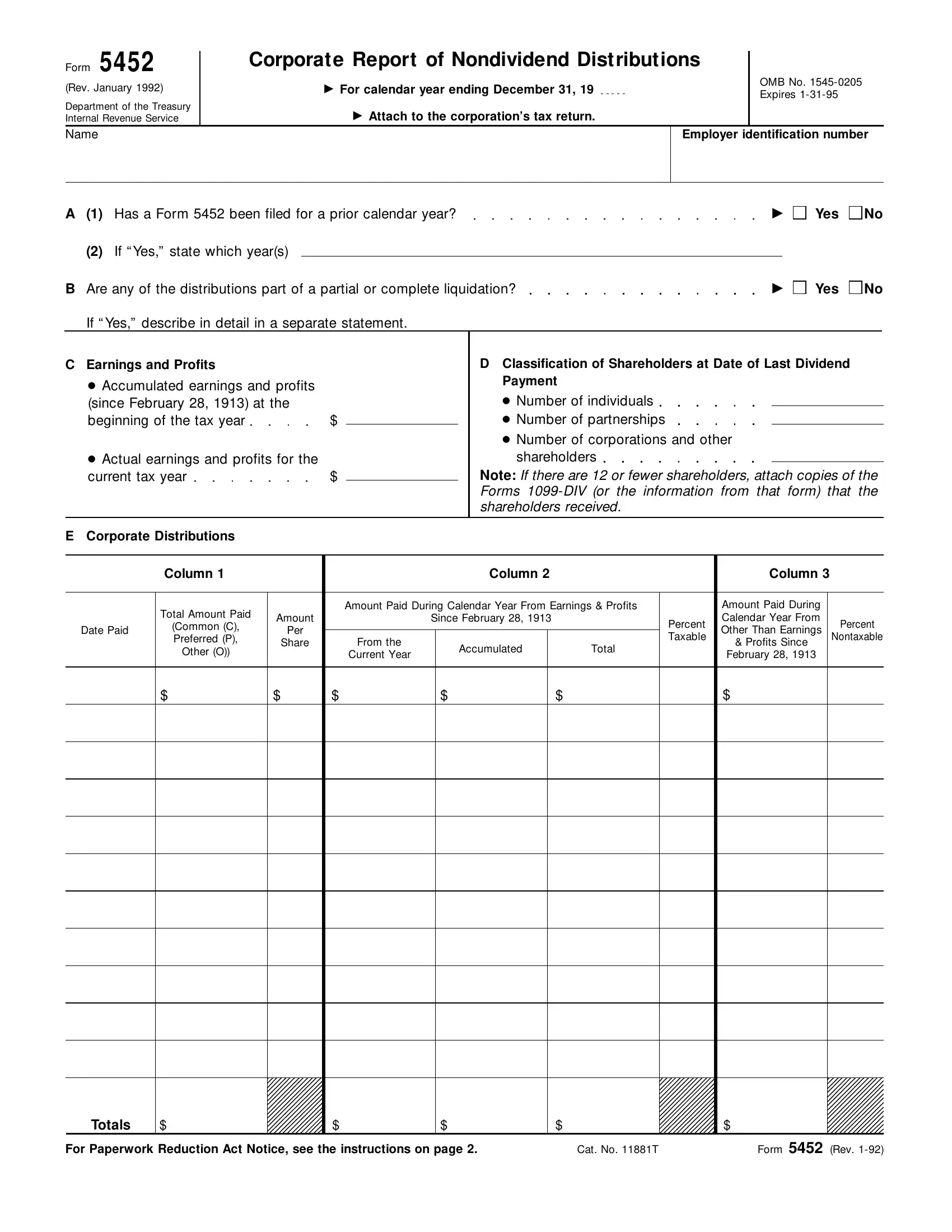

Understanding the intricacies of Form 5452, a Corporate Report of Nondividend Distributions, is pivotal for corporations navigating their annual tax obligations. Since its revision in January 1992, this form has been a crucial document for corporations recording distributions that are not considered dividends from the perspective of tax reporting. It is designed for use within the United States, with the Internal Revenue Service (IRS) mandating its submission alongside the corporation’s tax return for the relevant calendar year. Among its key aspects, Form 5452 encompasses questions regarding previous filings, detailed inquiries into whether distributions are part of a partial or complete liquidation, and requires a comprehensive breakdown of earnings and profits dating back to February 28, 1913. The form further categorizes shareholders at the date of the last dividend payment and details the total amount paid in distributions across various categories, thereby elucidating the tax implications of such distributions. These sections aim to clarify the taxable status of distributions reported to shareholders, distinguishing between those derived from current and accumulated earnings and profits and those that are not. With specific segments dedicated to supporting information, including calculations and adjustments related to earnings and profits for the tax year, Form 5452 encapsulates a systematic approach to reporting nondividend distributions. Instructions accompanying the form highlight both the necessity of adhering to the reporting requirements established under the Internal Revenue Code and the potential consequences of failing to do so. Detailed guidance is also provided for both the preparation of the form and the submission process, underscoring its significance in maintaining compliance with U.S. tax laws.

| Question | Answer |

|---|---|

| Form Name | Form 5452 |

| Form Length | 4 pages |

| Fillable? | Yes |

| Fillable fields | 1 |

| Avg. time to fill out | 1 min 12 sec |

| Other names | Nondeductible, 5452 form, Nontaxable, Distributions |