Navigating the complexities of employee benefit plans can often feel like trying to decipher an intricate maze, with each turn introducing a new set of rules and requirements. Among the key components in understanding and adhering to these rules are various forms issued by the Internal Revenue Service (IRS), one of which is the notable Form 6045. Designed as an Employee Plan Deficiency Checksheet, this form serves a critical function in the auditing process for defined contribution plans by pinpointing areas where compliance with coverage and nondiscrimination requirements has fallen short. Issued in March 2010 by the Department of the Treasury, Form 6045 requires plan administrators to furnish amendments or provide demonstrations ensuring their plans meet specific sections of the Internal Revenue Code (IRC) and regulations concerning nondiscriminatory classification, testing rules, and the average benefit test, among others. It guides administrators through a detailed review process, asking for information on plans that are disaggregated, permissively aggregated, or restructured, and scrutinizes the manner in which benefits, rights, or features are currently available to all employees to ensure there is no bias towards highly compensated individuals. Form 6045 also demands proofs related to the nondiscriminatory allocation of contributions or benefits and adjustments in the plan's definition of compensation to conform to nondiscriminatory requirements. This meticulous examination underscores the IRS's commitment to maintaining fairness in employee benefits administration, making Form 6045 a pivotal tool in safeguarding the equitable treatment of all plan participants.

| Question | Answer |

|---|---|

| Form Name | Form 6045 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | IRC, III, Nondiscrimination, mandatorily |

|

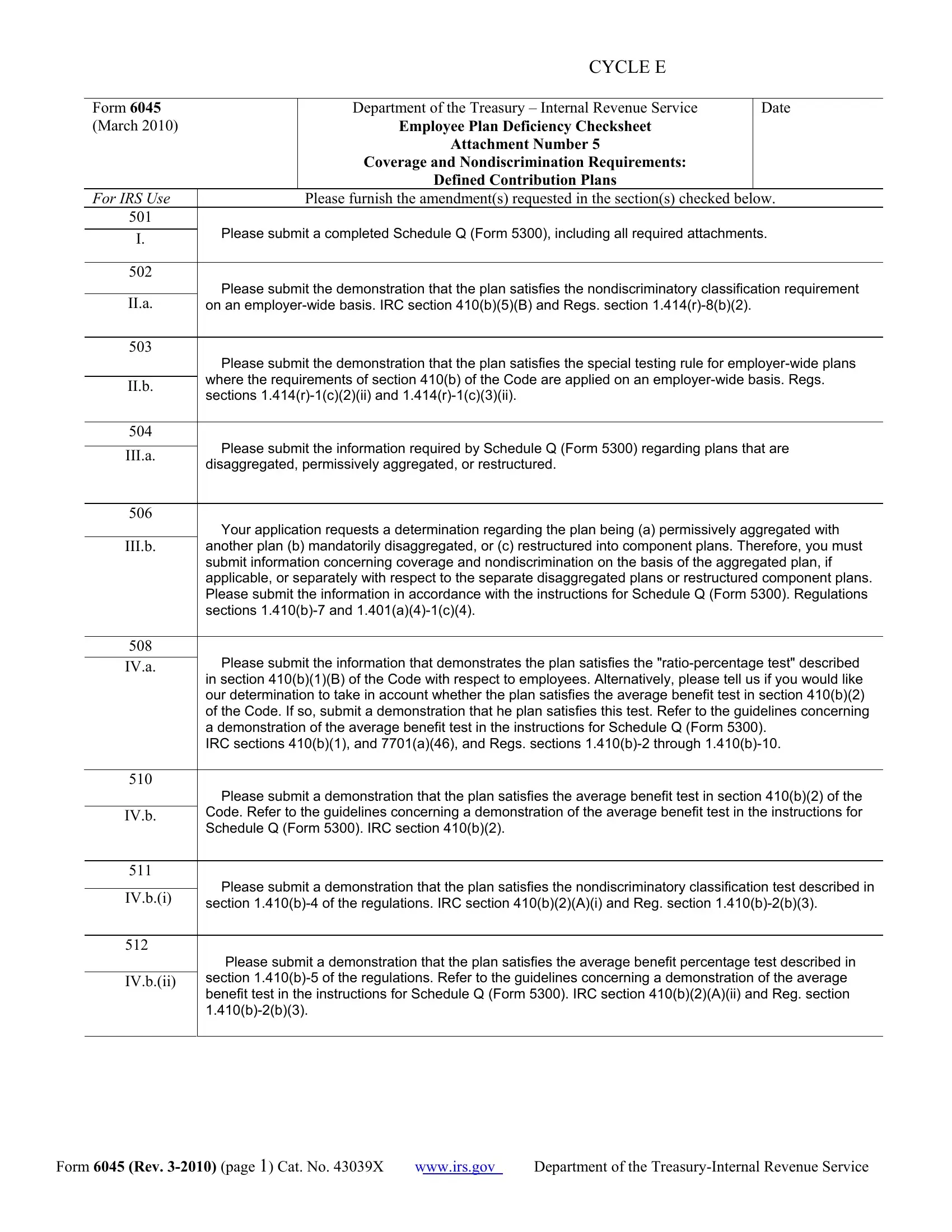

CYCLE E |

|

|

|

|

Form 6045 |

Department of the Treasury – Internal Revenue Service |

Date |

(March 2010) |

Employee Plan Deficiency Checksheet |

|

|

Attachment Number 5 |

|

|

Coverage and Nondiscrimination Requirements: |

|

|

Defined Contribution Plans |

|

FOR IRS USE |

Please furnish the amendment(s) requested in the section(s) checked below. |

|

501 |

|

|

I.Please submit a completed Schedule Q (Form 5300), including all required attachments.

502 |

|

|

|

Please submit the demonstration that the plan satisfies the nondiscriminatory classification requirement |

|

II.a. |

on an |

|

|

|

|

503 |

|

|

|

Please submit the demonstration that the plan satisfies the special testing rule for |

|

|

where the requirements of section 410(b) of the Code are applied on an |

|

II.b. |

||

sections |

||

|

||

|

|

|

504 |

|

|

|

Please submit the information required by Schedule Q (Form 5300) regarding plans that are |

|

III.a. |

||

disaggregated, permissively aggregated, or restructured. |

||

|

||

|

|

|

506 |

|

|

|

Your application requests a determination regarding the plan being (a) permissively aggregated with |

|

III.b. |

another plan (b) mandatorily disaggregated, or (c) restructured into component plans. Therefore, you must |

|

|

submit information concerning coverage and nondiscrimination on the basis of the aggregated plan, if |

|

|

applicable, or separately with respect to the separate disaggregated plans or restructured component plans. |

|

|

Please submit the information in accordance with the instructions for Schedule Q (Form 5300). Regulations |

|

|

sections |

|

|

|

|

508 |

|

|

|

Please submit the information that demonstrates the plan satisfies the |

|

IV.a. |

||

in section 410(b)(1)(B) of the Code with respect to employees. Alternatively, please tell us if you would like |

||

|

||

|

our determination to take in account whether the plan satisfies the average benefit test in section 410(b)(2) |

|

|

of the Code. If so, submit a demonstration that he plan satisfies this test. Refer to the guidelines concerning |

|

|

a demonstration of the average benefit test in the instructions for Schedule Q (Form 5300). |

|

|

IRC sections 410(b)(1), and 7701(a)(46), and Regs. sections |

|

|

|

|

510 |

|

|

|

Please submit a demonstration that the plan satisfies the average benefit test in section 410(b)(2) of the |

|

|

Code. Refer to the guidelines concerning a demonstration of the average benefit test in the instructions for |

|

IV.b. |

||

|

Schedule Q (Form 5300). IRC section 410(b)(2). |

|

|

|

|

511 |

|

|

|

Please submit a demonstration that the plan satisfies the nondiscriminatory classification test described in |

|

IV.b.(i) |

||

section |

||

|

||

|

|

|

512 |

|

|

|

Please submit a demonstration that the plan satisfies the average benefit percentage test described in |

|

|

section |

|

IV.b.(ii) |

||

benefit test in the instructions for Schedule Q (Form 5300). IRC section 410(b)(2)(A)(ii) and Reg. section |

||

|

||

|

Form 6045 (Rev. |

www.irs.gov |

Department of the |

|

CYCLE E |

|

|

|

|

513 |

|

|

|

You have requested a determination of whether benefits, rights, or features satisfy the nondiscriminatory |

|

V.b. |

||

current availability requirement under section |

||

|

||

|

specific benefit, right, or feature you wish considered. Reg. section |

|

|

|

|

514 |

|

|

|

Please submit a demonstration that the benefit, right, or feature described in section __________ of the |

|

V.c. |

||

plan meets the nondiscriminatory current availability requirement under section |

||

|

||

|

regulations. Reg. section |

|

|

|

|

515 |

|

|

VI. |

Please submit a demonstration in accordance with the instructions for Schedule Q (Form 5300) that the |

|

|

manner in which service is credited under section __________ of the plan is nondiscriminatory. Regs. |

|

|

section |

|

|

|

|

516 |

|

|

VII.a. |

Section __________ of the plan should be amended so that the manner in which employees vest in their |

|

benefits under the plan is nondiscriminatory. Regs. section |

||

|

||

|

|

|

517 |

|

|

VII.b. |

Please demonstrate, with respect to section _______ of the plan, that the plan satisfies the requirement |

|

|

that it be nondiscriminatory with respect to the availability of benefits, rights, or features provided to former |

|

|

employees. Regs. section |

|

|

|

|

518 |

|

|

|

Please submit a demonstration that the plan satisfies a general test for nondiscrimination in the amounts |

|

VIII.b.. |

||

of contributions or benefits under the plan. IRC section 401(a)(4); and Reg. sections |

||

|

||

|

||

|

|

|

519 |

|

|

VIII.c. |

Please submit a demonstration that the plan satisfies the safe harbor for plans with uniform points |

|

|

allocation formulas. IRC section 401(a)(4) and Reg. section |

|

|

|

|

520 |

|

|

|

Section __________ of the plan should be amended to provide a uniform allocation formula that will satisfy |

|

IX.a. |

the safe harbor described in section |

|

|

Regs. section |

|

|

|

|

521 |

|

|

|

Section __________ of the plan should be amended to satisfy the target benefit plan safe harbor |

|

|

described in section |

|

IX.b. |

||

|

||

|

|

|

522 |

|

|

|

The definition of compensation contained in section __________ of the plan should be amended to |

|

X.a. |

||

conform to one of the definitions described in sections |

||

|

regulations. Alternatively, submit a demonstration that the plan’s definition of compensation is |

|

|

nondiscriminatory. IRC section 414(s) and. Regs . section |

|

|

|

|

523 |

|

|

|

Section __________ of the plan should be amended to define compensation for |

|

III.e. |

||

in the manner described in section |

||

|

||

|

|

Form 6045 (Rev. |

www.irs.gov |

Department of the |