You are able to prepare Form 6252 effortlessly in our PDFinity® online PDF tool. The tool is continually upgraded by us, getting powerful functions and becoming greater. If you're seeking to begin, here is what it will take:

Step 1: Open the form inside our tool by hitting the "Get Form Button" above on this page.

Step 2: With our state-of-the-art PDF editing tool, it is easy to accomplish more than merely fill out blank fields. Edit away and make your docs look sublime with customized text put in, or fine-tune the file's original input to excellence - all comes along with the capability to add just about any graphics and sign the PDF off.

With regards to the fields of this specific document, here is what you should do:

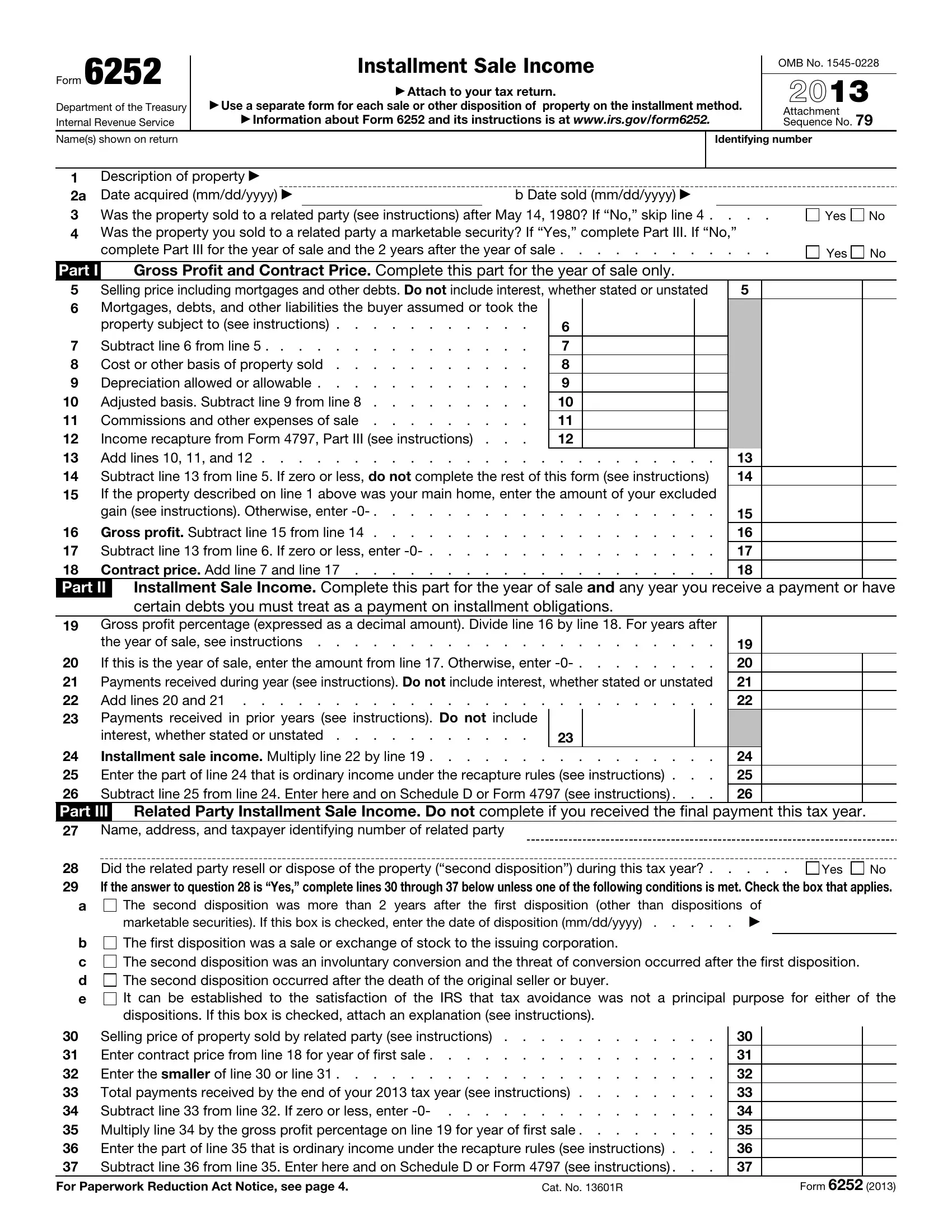

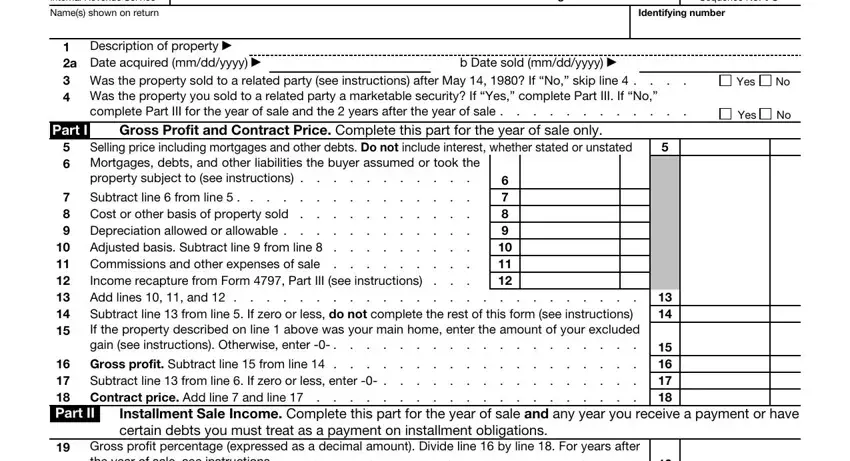

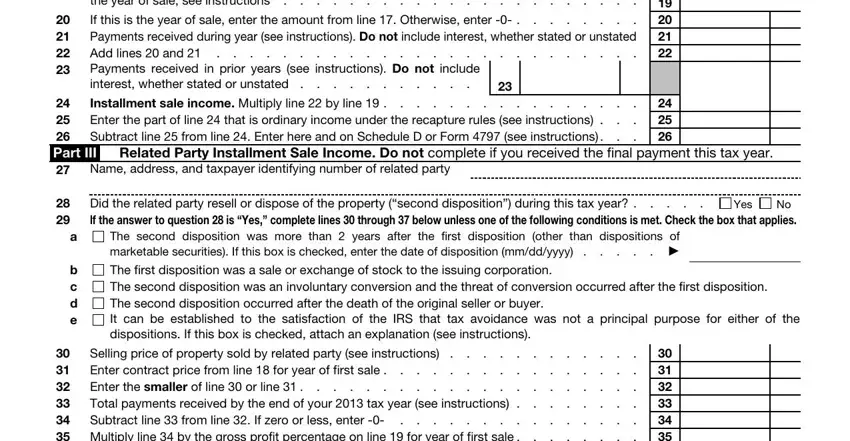

1. It is recommended to fill out the Form 6252 properly, therefore be careful when filling in the sections that contain these specific blank fields:

2. Once your current task is complete, take the next step – fill out all of these fields - Gross profit percentage expressed, the year of sale see instructions, If this is the year of sale enter, Installment sale income Multiply, Part III Name address and, Related Party Installment Sale, No If the answer to question is, Did the related party resell or, The second disposition was more, Yes, b c d e, The first disposition was a sale, Selling price of property sold by, Multiply line by the, and Enter the part of line that with their corresponding information. Make sure to double check that everything has been entered correctly before continuing!

3. In this specific part, have a look at Multiply line by the, Enter the part of line that, For Paperwork Reduction Act Notice, Cat No R, and Form. Each one of these should be taken care of with utmost focus on detail.

Always be really mindful when filling out Form and Cat No R, as this is where most users make a few mistakes.

Step 3: Proofread the details you've inserted in the form fields and click on the "Done" button. After creating a7-day free trial account here, you'll be able to download Form 6252 or send it through email promptly. The PDF document will also be available through your personal cabinet with all your modifications. FormsPal guarantees your information confidentiality by having a protected system that never records or shares any kind of private data provided. Feel safe knowing your docs are kept protected each time you use our editor!