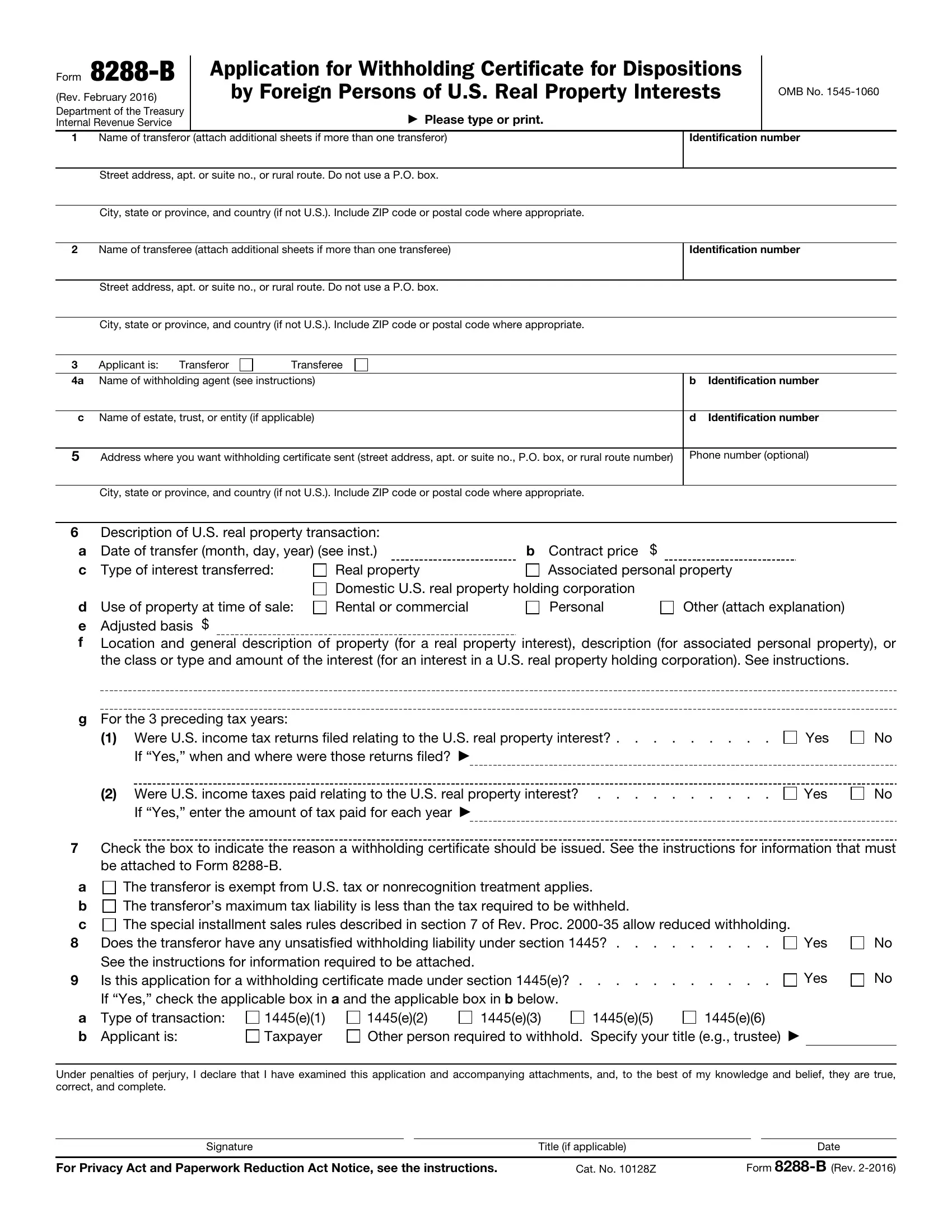

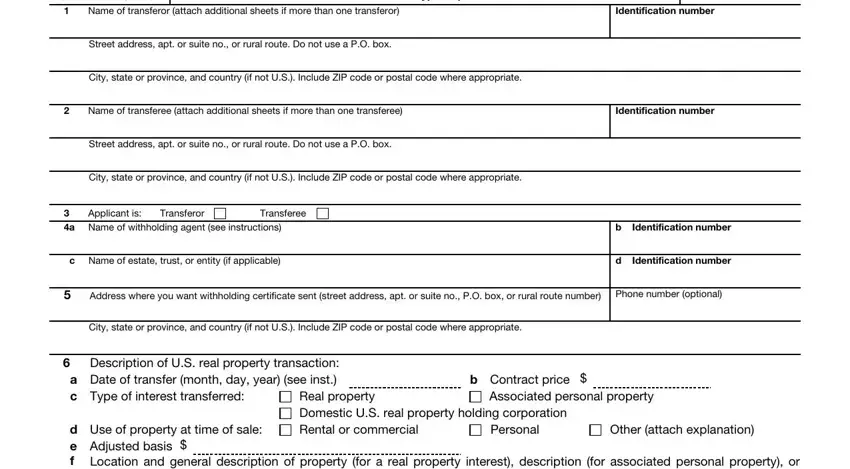

Line 4c. If you are acting on behalf of an estate or trust, or are signing as an authorized person for an entity other than an individual (for example, a corporation, qualified investment entity, or partnership), enter the name of the estate, trust, or entity.

Line 4d. Enter the EIN of the estate, trust, or entity.

Line 5. Enter the address you want the IRS to use for purposes of returning the withholding certificate.

Line 6a. Enter the year as a four-digit number (for example, “2013”).

Line 6c. “Associated personal property” means property (for example, furniture) sold with a building. See Regulations section 1.897-1.

Line 6d. Check “Other” if the property was used for both personal and rental use and attach an explanation.

Line 6f. Enter the address and description of the property (for example, “10-story,

100-unit luxury apartment building”). For a real estate holding corporation interest transferred, enter the class or type and amount of the interest (for example, “10,000 shares Class A Preferred Stock XYZ Corporation”). You may attach additional sheets. Be sure to include your name and TIN on each sheet you attach.

Line 6g. A U.S. income tax return includes Forms 1040NR, and 1120-F.

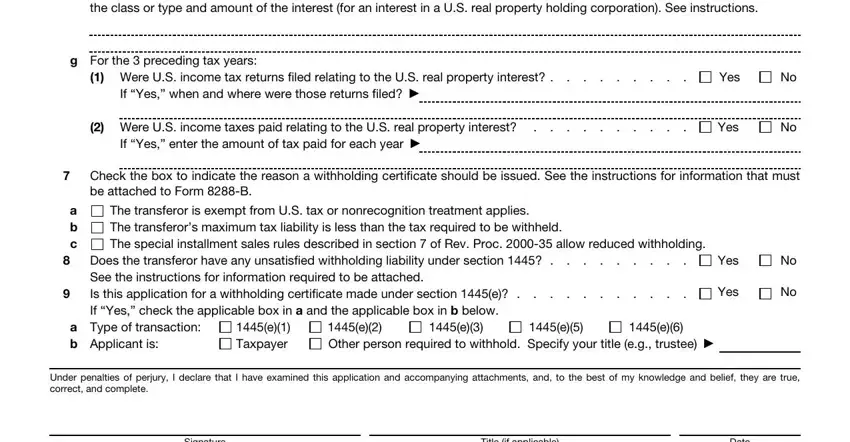

Line 7a. If you checked 7a, attach:

1.A brief description of the transfer,

2.A summary of the law,

3.Facts supporting the claim of exemption or nonrecognition,

4.Evidence that the transferor has no unsatisfied withholding liability, and

5.The most recent assessed value for state or local property tax purposes of the interest to be transferred, or other estimate of its fair market value. You need not submit supporting evidence of the value of the property.

A nonresident alien or foreign corporation must also attach a statement of the adjusted basis of the property immediately before the distribution or transfer.

Line 7b. If you checked 7b, attach a calculation of the maximum tax that can be imposed on the disposition. You must also include a statement signed by the transferor under penalties of perjury that the calculation and all supporting evidence is true and correct to the best knowledge of the transferor.

The calculation of the maximum tax that can be imposed must include:

1.Evidence of the amount to be realized by the transferor, such as a copy of the signed contract of transfer;

2.Evidence of the adjusted basis of the property, such as closing statements, invoices for improvements, and depreciation schedules, or if no depreciation schedules are submitted, a statement of the nature of the use of the property and why depreciation was not allowed;

3.Amounts to be recaptured for depreciation, investment credit, or other items subject to recapture;

4.The maximum capital gain and/or ordinary income tax rates applicable to the transfer;

5.The tentative tax owed; and

6.Evidence showing the amount of any increase or reduction of tax to which the transferor is subject, including any reduction to which the transferor is entitled under a U.S. income tax treaty.

If you have a net operating loss, see Rev. Proc. 2000-35, section 4.06, for special rules about the maximum tax calculation.

If the purchase price includes personal property not subject to tax under section 897, for the calculation of maximum tax, the transferor must also include a statement listing each such item of personal property transferred and the fair market value attributable to each item. The fair market value claimed should be supported by an independent appraisal or other similar documentation.

Line 7c. If you checked 7c, see Installment sales, earlier.

Line 8. You must provide a calculation of the transferor’s unsatisfied withholding liability or evidence that it does not exist. This liability is the amount of any tax the transferor was required to, but did not, withhold and pay over under section 1445 when the U.S. real property interest now being transferred was acquired, or upon a prior acquisition. The transferor’s unsatisfied withholding liability is included in the calculation of maximum tax liability so that it can be satisfied by the withholding on the current transfer.

Evidence that there is no unsatisfied withholding liability includes any of the following:

1.Evidence that the transferor acquired the subject or prior real property interest before 1985;

2.A copy of Form 8288 filed and proof of payment;

3.A copy of a withholding certificate issued by the IRS plus a copy of Form

8288 and proof of payment of any amount required by that certificate;

4.A copy of the nonforeign certificate furnished by the person from whom the U.S. real property interest was acquired (the certificate must be executed at the time of acquisition);

5.Evidence that the transferor purchased the subject or prior real property interest for $300,000 or less and a statement, signed by the transferor under penalties of perjury, that the transferor purchased the property for use as a residence within the meaning of Regulations section 1.1445-2(d)(1);

6.Evidence that the person from whom the transferor acquired the subject or prior U.S. real property interest fully paid any tax imposed on that transaction under section 897;

7.A copy of a notice of nonrecognition treatment provided to the transferor under Regulations section 1.1445-2(d)(2) by the person from whom the transferor acquired the subject or prior U.S. real property interest; or

8.A statement, signed by the transferor under penalties of perjury, explaining why the transferor was not required to withhold under section 1445(a) with regard to the transferor’s acquisition of the subject or prior real property interest.

Line 9a. If the transaction is subject to withholding under section 1445(e), check the box to indicate which provision of section 1445(e) applies.

Line 9b. Indicate whether the applicant is the taxpayer or the person required to withhold, and in what capacity that person is required to withhold.

Signature. The application must be signed by an individual, a responsible corporate officer, a general partner of a partnership, or a trustee, executor, or other fiduciary of a trust or estate. The application may also be signed by an authorized agent with a power of attorney. Form 2848, Power of Attorney and Declaration of Representative, can be used for this purpose.

Privacy Act and Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the United States. Section 1445 generally imposes a withholding obligation on the buyer or other transferee (withholding agent) when a U.S. real property interest is acquired from a foreign person. Section

1445 also imposes a withholding obligation on certain foreign and domestic corporations, qualified investment entities, and the fiduciary of certain trusts and estates. This form is used to apply for a withholding certificate to reduce or eliminate withholding on dispositions of U.S. real property interests by foreign persons if certain conditions apply.

You are required to provide this information. Section 6109 requires you to provide your identification number. We need this information to ensure that you are complying with the Internal Revenue laws and to allow us to figure and collect the right amount of tax. Failure to provide this information in a timely manner, or providing false information, may subject you to penalties. Routine uses of this information include giving it to the Department of Justice for civil and criminal litigation, and to cities, states, the District of Columbia, and to U.S. commonwealths and possessions for use in the administration of their tax laws. We may also disclose this information to other countries under a tax treaty, to federal and state agencies to enforce federal nontax criminal laws, or to federal law enforcement and intelligence agencies to combat terrorism.