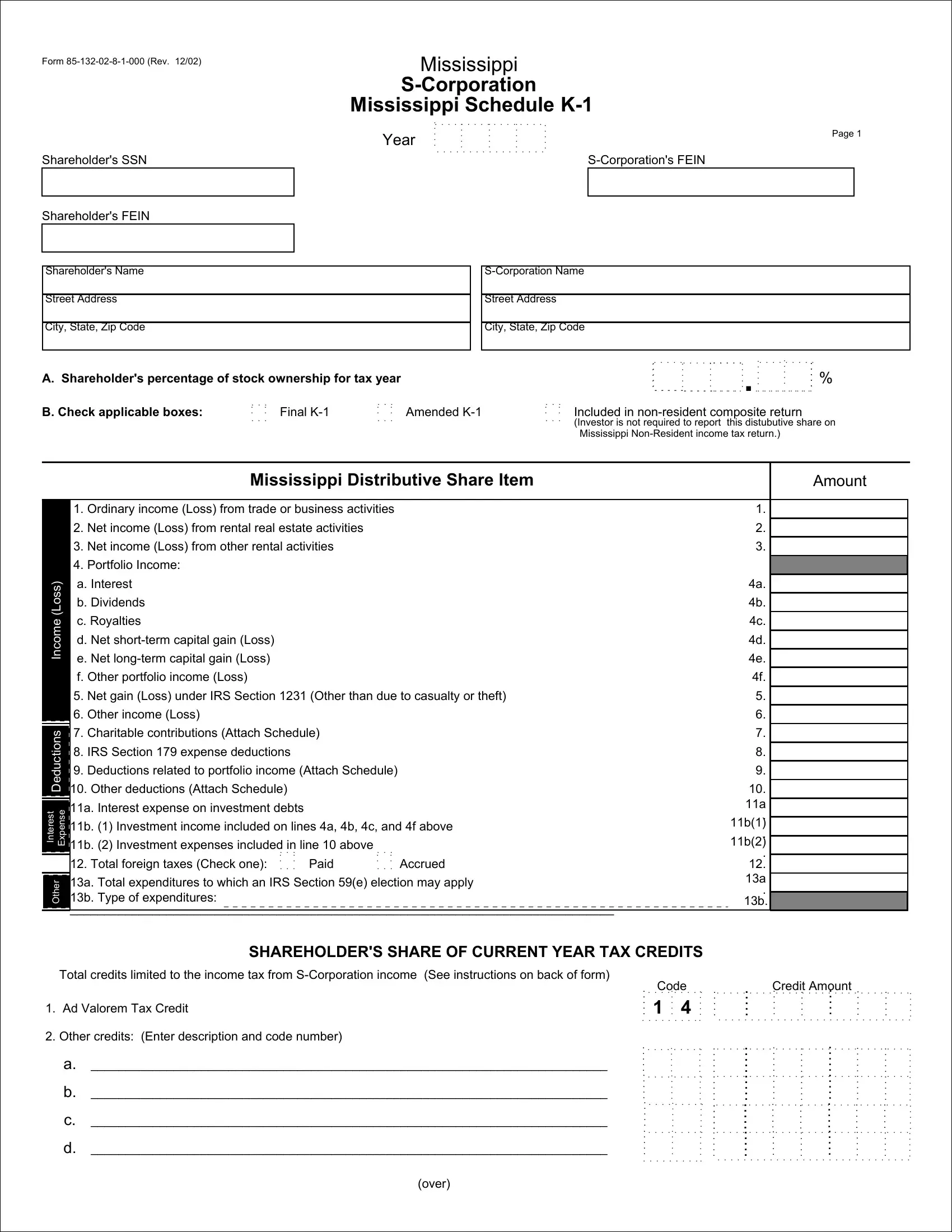

The Form 85-132-02-8-1-000, revised as of December 2002, serves as a critical document for Mississippi S-Corporations, providing a detailed Schedule K-1 for shareholders. This form comprehensively captures the shareholder's Social Security Number (SSN), the S-Corporation's Federal Employer Identification Number (FEIN), the shareholder's FEIN, and their respective names and addresses, alongside the shareholder’s percentage of stock ownership for the tax year. It facilitates the reporting of the Mississippi Distributive Share Items, emphasizing ordinary income or losses from various business activities, portfolio income, including interest and dividends, and specific income or losses such as those under IRS Section 1231 or from charitable contributions. Additionally, it itemizes deductions related to portfolio income, other deductions, and interest expenses on investment debts, presenting a methodology for the calculation of tax credits limited to income from S-Corporation activities. On page 2, the form outlines general restrictions on credits, detailing the utilization and carryforward guidelines for various tax credits available to shareholders, such as the ad valorem tax credit, the jobs tax credit, and the reforestation tax credit. This document not only provides key financial information for the year but also guides shareholders through the proper declaration and maximization of potential tax credits in accordance with Mississippi tax laws, making it an indispensable tool for S-Corporation shareholders within the state.

| Question | Answer |

|---|---|

| Form Name | Form 85 132 02 8 1 000 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | 85132028 mississippi schedule k1 2014 form |

Form

Mississippi

Mississippi Schedule

.. . . . . . . . .. . . . .. . . . . . |

|

|

|||||

. |

. |

. |

. |

. |

Page 1 |

||

. |

. |

. |

. |

. |

|||

|

Year .. |

. |

. |

. |

. |

|

|

|

|

. . . . .. . . . .. . . . .. . . . .. |

|

|

|||

Shareholder's SSN |

|

|

|

|

|||

|

|

|

|

|

|

|

|

Shareholder's FEIN

Shareholder's Name

Street Address

City, State, Zip Code

A. Shareholder's percentage of stock ownership for tax year

Street Address

City, State, Zip Code

........ ... ... ... ........... ... ... ... .......... ... ... ... .................................................. %

B. Check applicable boxes:

.. . .. |

Final |

. . |

|

. . . |

|

.. . .. |

Amended |

.. . .. |

. . |

. . |

|

. . . |

|

. . . |

Included in

(Investor is not required to report this distubutive share on Mississippi

|

|

Mississippi Distributive Share Item |

|||

|

|

Ordinary income (Loss) from trade or business activities |

|||

|

1. |

||||

|

2. |

Net income (Loss) from rental real estate activities |

|

||

|

3. |

Net income (Loss) from other rental activities |

|

||

|

4. |

Portfolio Income: |

|

|

|

(Loss) |

a. Interest |

|

|

||

b. Dividends |

|

|

|||

|

|

|

|||

Income |

c. Royalties |

|

|

||

d. Net |

|

|

|||

|

|

|

|||

|

e. Net |

|

|

||

|

f. Other portfolio income (Loss) |

|

|

||

|

5. |

Net gain (Loss) under IRS Section 1231 (Other than due to casualty or theft) |

|||

|

6. |

Other income (Loss) |

|

|

|

|

7. |

Charitable contributions (Attach Schedule) |

|

||

Deductions |

|

||||

8. |

IRS Section 179 expense deductions |

|

|

||

|

|

|

|||

|

9. |

Deductions related to portfolio income (Attach Schedule) |

|||

|

10. Other deductions (Attach Schedule) |

|

|

||

|

11a. Interest expense on investment debts |

|

|||

Interest Expense |

|

||||

11b. (1) Investment income included on lines 4a, 4b, 4c, and 4f above |

|||||

|

|||||

|

11b. (2) Investment expenses included. .in. |

line 10 above . . . |

|||

|

|

. . |

|

. . |

|

|

|

. . |

Paid |

. . |

|

|

12. Total foreign taxes (Check one): . . . |

. . . Accrued |

|||

Other |

13a. Total expenditures to which an IRS Section 59(e) election may apply |

||||

13b. Type of expenditures: |

|

|

|||

|

_______________________________________________________________________________ |

||||

|

|||||

Amount

1.

2.

3.

4a.

4b.

4c.

4d.

4e.

4f.

5.

6.

7.

8.

9.

10.

11a 11b(1).

11b(2).

.

12.

13a

.

13b.

SHAREHOLDER'S SHARE OF CURRENT YEAR TAX CREDITS

Total credits limited to the income tax from

1.Ad Valorem Tax Credit

2.Other credits: (Enter description and code number)

a. ___________________________________________________________________________

b. ___________________________________________________________________________

c.___________________________________________________________________________

d. ___________________________________________________________________________

|

Code |

|

. . . . . .. . . . .. |

||

. |

. |

. |

. |

. |

. |

. |

1 . |

4 . |

. |

. |

. |

. . . . . . . . . .

. . . . . . . . . . .. |

||

. |

. |

. |

. |

. |

. |

. |

. |

. |

.. . . . .... . . . ... |

||

. |

. |

. |

. |

. |

. |

. |

. |

. |

.. . . . .... . . . ... |

||

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. . . . . .. . . . .. |

||

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. . . . . . . . . .

. . . . . .... . . .Credit.. . . . .. .Amount. . ... . . . .. . . . . .. . . ..

.... . . . . .... . . . ..... . . . . ..... . . . .... . . . ..... . . . ..... . . . .....

. . . . . ... . . . . ... . . . .. . . . ... . . . .. . . . . .. . . ..

..... . . . . ...... . . . . ...... . . . ...... . . . ..... . . . ...... . . . . ...... . . ......

.... ... ... .... .... .... .... ....

.. . . . ... . . . . ... . . . .. . . . . . . . .. . . . . .. . . . .

......... .. .. .. .. .......... .. .. .. ............ .. .. .. ........... .. .. .. ......... .. .. .. ........... .. .. .. ............. .. .. ...........

(over)

Form

GENERAL RESTRICTIONS ON CREDITS

Mississippi

Mississippi Schedule

Page 2

Generally, partners share of current year's tax credits may only be used to offset income tax imposed on partnership income. The total of the jobs tax credit, headquarters credit, research and development skills credit, and the basic skills training and retraining credit cannot exceed 50% of the total income tax liability. The child/ dependent care credit can be used against 100% of income tax due. The export port charges credit cannot exceed 50% of the amount of income tax for the taxable year reduced by the sum of all other credits. The reforestation tax credit shall not exceed the lesser of $10,000 or the amount of income tax imposed upon the eligible owner for the taxable year reduced by the sum of all other credits allowable to the eligible owner. The ad valorem tax credit and gambling license fee credit may be claimed only in the year in which the ad valorem taxes and gambling license fees are paid. Any excess and/or unused ad valorem tax credit or gambling license fee credit, cannot be carried forward. Unused portions of the jobs tax credit, headquarters credit, research and development skills credit, child/dependent care credit, job training and retraining, and export port charges credit can be carried forward for up to 5 years. Any unused portion of the reforestation tax credit may be carried forward for succeeding tax years. The maximum reforestation tax credit that an eligible owner may utilize during their lifetime shall be $10,000 in the aggregate.

SUPPLEMENTAL INFORMATION