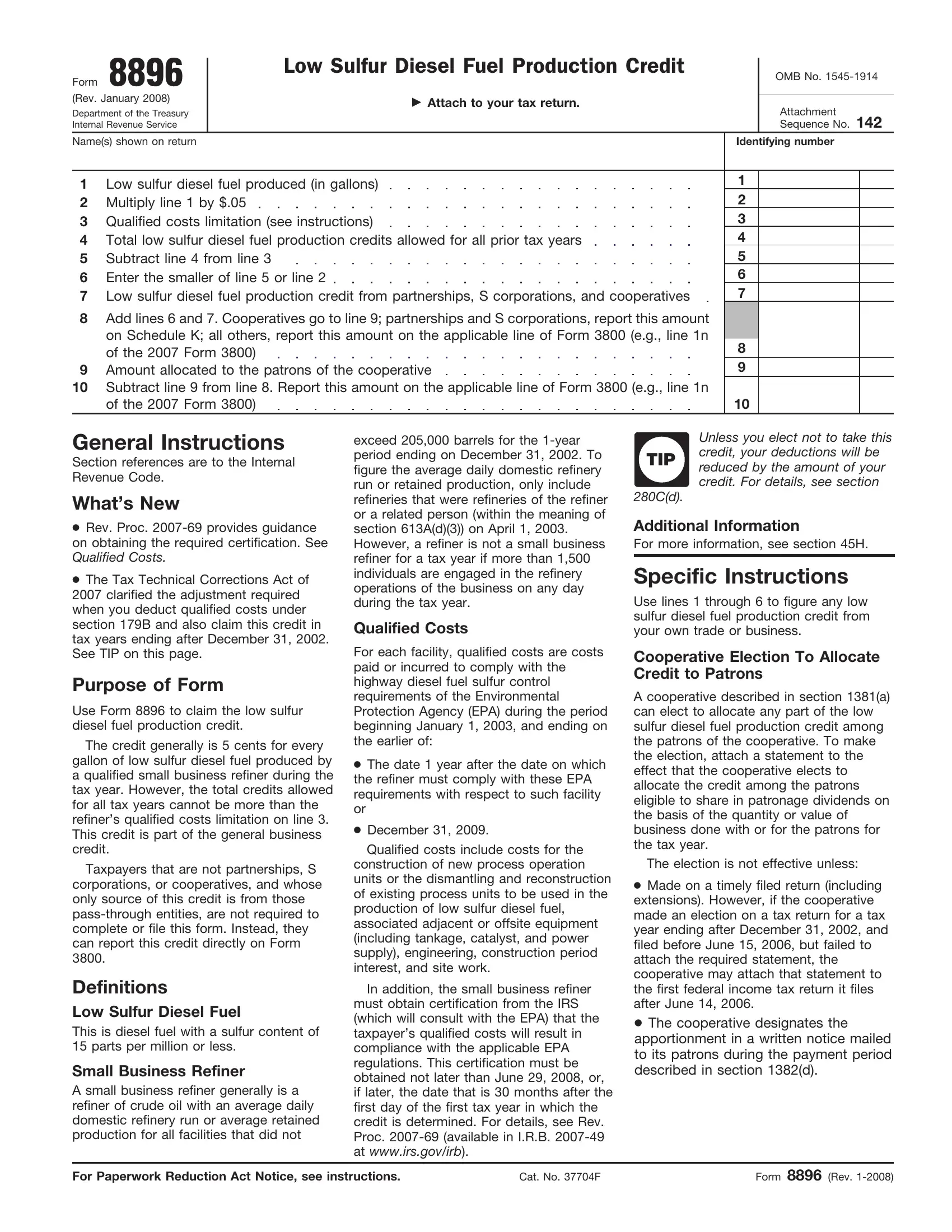

The Internal Revenue Service's Form 8896, dedicated to the Low Sulfur Diesel Fuel Production Credit, plays a crucial role for qualified small business refiners seeking to claim benefits related to the production of low sulfur diesel fuel. This form, revised in January 2008, acts as a gateway for businesses to secure a credit generally amounting to 5 cents for each gallon of low sulfur diesel, defined by a sulfur content of 15 parts per million or less, produced within a tax year. The potential credit, however, is capped by the refiner's qualified costs on line 3 of the form, ensuring that the total credits across all tax years do not exceed this predefined limit. It emphasizes the necessity to adhere to the Environmental Protection Agency's diesel fuel sulfur control requirements, where qualified costs entail expenditures on new constructions or modifications of existing units to produce compliant fuel. Moreover, this form underlines the importance of obtaining certification from the IRS, in consultation with the EPA, to verify compliance with the necessary regulations. Cooperative decisions to allocate the credit and the implications on deductions, as guided by section 280C(d), further delineate the parameters within which the credits can be claimed or passed through to different entities. This comprehensive approach, encapsulated in Form 8896, underscores the government's effort to incentivize the production of environmentally friendlier fuel choices while setting a structured framework for claiming these incentives.

| Question | Answer |

|---|---|

| Form Name | Form 8896 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | refiner, 45H, 8896 form, 280C |

Form |

8896 |

|

LOW SULFUR |

DIESEL FUEL PRODUCTION |

CREDIT |

|

OMB No. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

(Rev. January 2008) |

|

|

▶ Attach to your tax return. |

|

|

|

|

|

|

|

Attachment |

||||

Department of the Treasury |

|

|

|

|

|||

Internal Revenue Service |

|

|

|

|

|

Sequence No. 142 |

|

Name(s) shown on return |

|

|

|

Identifying number |

|||

|

|

|

|

|

|

||

1 |

Low sulfur diesel fuel produced (in gallons) |

|

|

1 |

|

||

2 |

Multiply line 1 by $.05 |

|

|

|

2 |

|

|

3 |

Qualified costs limitation (see instructions) |

|

|

3 |

|

||

4 |

Total low sulfur diesel fuel production credits allowed for all prior tax years |

|

4 |

|

|||

5 |

Subtract line 4 from line 3 |

|

|

|

5 |

|

|

6 |

Enter the smaller of line 5 or line 2 |

|

|

6 |

|

||

7 |

Low sulfur diesel fuel production credit from partnerships, S corporations, and cooperatives |

7 |

|

||||

8Add lines 6 and 7. Cooperatives go to line 9; partnerships and S corporations, report this amount on Schedule K; all others, report this amount on the applicable line of Form 3800 (e.g., line 1n

of the 2007 Form 3800) |

8 |

9 Amount allocated to the patrons of the cooperative |

9 |

10Subtract line 9 from line 8. Report this amount on the applicable line of Form 3800 (e.g., line 1n

of the 2007 Form 3800) |

10 |

General Instructions

Section references are to the Internal Revenue Code.

What’s New

●Rev. Proc.

Qualified Costs.

●The Tax Technical Corrections Act of 2007 clarified the adjustment required when you deduct qualified costs under section 179B and also claim this credit in tax years ending after December 31, 2002. See TIP on this page.

Purpose of Form

Use Form 8896 to claim the low sulfur diesel fuel production credit.

The credit generally is 5 cents for every gallon of low sulfur diesel fuel produced by a qualified small business refiner during the tax year. However, the total credits allowed for all tax years cannot be more than the refiner’s qualified costs limitation on line 3. This credit is part of the general business credit.

Taxpayers that are not partnerships, S corporations, or cooperatives, and whose only source of this credit is from those

Definitions

Low Sulfur Diesel Fuel

This is diesel fuel with a sulfur content of 15 parts per million or less.

Small Business Refiner

A small business refiner generally is a refiner of crude oil with an average daily domestic refinery run or average retained production for all facilities that did not

exceed 205,000 barrels for the

Qualified Costs

For each facility, qualified costs are costs paid or incurred to comply with the highway diesel fuel sulfur control requirements of the Environmental Protection Agency (EPA) during the period beginning January 1, 2003, and ending on the earlier of:

●The date 1 year after the date on which the refiner must comply with these EPA requirements with respect to such facility or

●December 31, 2009.

Qualified costs include costs for the construction of new process operation units or the dismantling and reconstruction of existing process units to be used in the production of low sulfur diesel fuel, associated adjacent or offsite equipment (including tankage, catalyst, and power supply), engineering, construction period interest, and site work.

In addition, the small business refiner must obtain certification from the IRS (which will consult with the EPA) that the taxpayer’s qualified costs will result in compliance with the applicable EPA regulations. This certification must be obtained not later than June 29, 2008, or, if later, the date that is 30 months after the first day of the first tax year in which the credit is determined. For details, see Rev. Proc.

Unless you elect not to take this credit, your deductions will be

TIP reduced by the amount of your credit. For details, see section

280C(d).

Additional Information

For more information, see section 45H.

Specific Instructions

Use lines 1 through 6 to figure any low sulfur diesel fuel production credit from your own trade or business.

Cooperative Election To Allocate Credit to Patrons

A cooperative described in section 1381(a) can elect to allocate any part of the low sulfur diesel fuel production credit among the patrons of the cooperative. To make the election, attach a statement to the effect that the cooperative elects to allocate the credit among the patrons eligible to share in patronage dividends on the basis of the quantity or value of business done with or for the patrons for the tax year.

The election is not effective unless:

●Made on a timely filed return (including extensions). However, if the cooperative made an election on a tax return for a tax year ending after December 31, 2002, and filed before June 15, 2006, but failed to attach the required statement, the cooperative may attach that statement to the first federal income tax return it files after June 14, 2006.

●The cooperative designates the apportionment in a written notice mailed to its patrons during the payment period described in section 1382(d).

For Paperwork Reduction Act Notice, see instructions. |

Cat. No. 37704F |

Form 8896 (Rev. |

Form 8896 (Rev. |

Page 2 |

|

|

If you timely file your return without making an election, you can still make the election by filing an amended return with the statement within 6 months of the due date of the return (excluding extensions). Enter “Filed pursuant to section

Once made, the election cannot be revoked.

Line 1

Enter the number of gallons of diesel fuel produced with a sulfur content of 15 parts per million or less.

Line 3

On line 3, enter 25% of the qualified costs (defined above) for the facility that produced the fuel reported on line 1 if your average daily domestic refinery runs were not more than 155,000 barrels for the

Example. Your average daily domestic refinery runs were 165,000 barrels for the

.8. Then multiply 25% by .8 to get 20%. On line 3, enter 20% of the qualified costs for the facility that produced the fuel reported on line 1.

Line 4

Enter the total low sulfur diesel fuel production credits allowed for all prior tax years (as determined for line 6).

Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the United States. You are required to give us the information. We need it to ensure that you are complying with these laws and to allow us to figure and collect the right amount of tax.

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents

may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

The time needed to complete and file this form will vary depending on individual circumstances. The estimated burden for individual taxpayers filing this form is approved under OMB control number

Recordkeeping, 6 hr., 13 min.; Learning about the law or the form, 45 min.;

Preparing and sending the form to the IRS, 2 hr., 5 min.

If you have comments concerning the accuracy of these time estimates or suggestions for making this form simpler, we would be happy to hear from you. See the instructions for the tax return with which this form is filed.