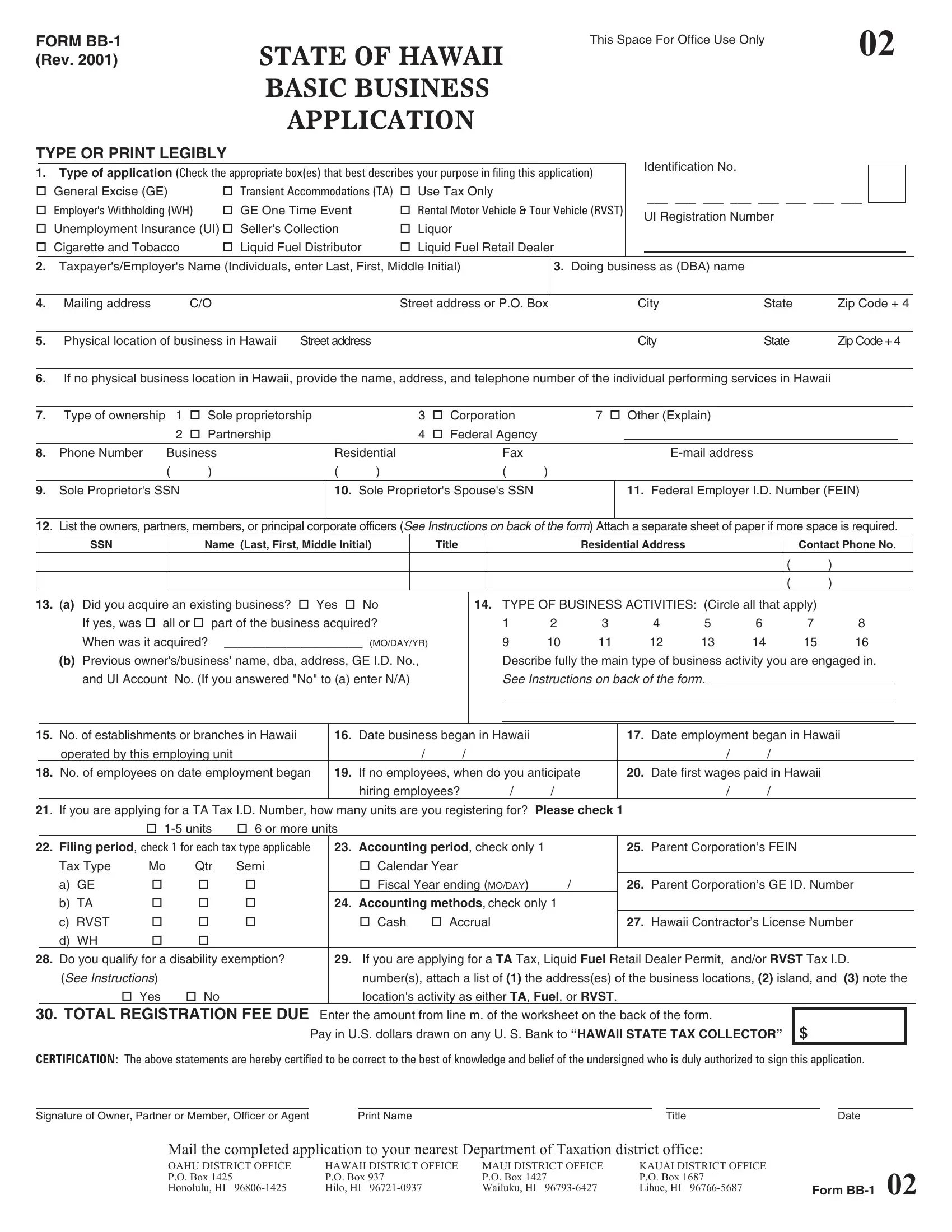

Stepping into the business landscape of Hawaii requires meticulous preparation, especially when it comes to compliance with state regulations. The Form BB-1, a fundamental document processed by the State of Hawaii, serves as a gateway for businesses to register for several pivotal state tax and employer licenses and permits. This includes, but is not limited to, General Excise (GE) tax, Transient Accommodations (TA) tax, withholding (WH) tax, and unemployment insurance (UI) tax. Its comprehensiveness ensures businesses can efficiently declare their activity types, ranging from rental motor vehicle services to liquor distribution, and report essential details about their operations, ownership type, and anticipated employment needs. Moreover, the form facilitates the registration for a TA Tax I.D. Number and the application for various other tax types depending on the business's specific activities in Hawaii. The fee structure outlined in the form, which differs based on the nature and timing of the business activity, underscores the state's approach to regulating and supporting businesses. Additionally, the form accommodates for disability exemptions and provides clear instructions on accounting and filing period selections, ensuring businesses are well-informed to comply with the state's taxation and employment laws. By detailing the process of acquiring an existing business and the responsibilities that come with it, the Form BB-1 acts as an all-encompassing resource for new and existing businesses to seamlessly integrate into Hawaii's commercial tapestry.

| Question | Answer |

|---|---|

| Form Name | Form Bb 1 |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | MAUI, LEGIBLY, 2001, form bb 1 |