In navigating the complexities of real estate taxation and compliance, owners of apartment buildings in California are acquainted with the BOE-571-R form, a crucial document intended for the declaration of costs and other related property information as of 12:01 A.M., January 1, 2012. This form serves a pivotal role in ensuring accurate property valuation by requesting detailed information about the property, including the number of units, furniture, appliances, and other equipment owned, possessed, or controlled by the property owner. It critically examines changes in ownership and control of real properties, requiring property owners to report if an individual or legal entity has acquired a controlling interest in their entity, potentially impacting the ownership of real property in California. Moreover, it asks for detailed accounts of any business or personal property located on the premises, furniture or equipment held on a loan, rental, or lease basis, and even supplies on hand, all of which influence the property's assessed value. Detailed depreciation schedules for both furniture and other equipment are required, ensuring a comprehensive account of property assets. This form must be completed with the utmost attention to detail and accuracy, as it is declared under penalty of perjury and is subject to audit, reinforcing the importance of full disclosure and compliance with state taxation laws. Overall, the BOE-571-R form encapsulates a significant part of the property assessment process, enabling the California tax authorities to maintain a fair and efficient system for real estate taxation.

| Question | Answer |

|---|---|

| Form Name | Form Boe 571 R |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | SM571r rev14 02 11 san mateo interactive form 571 r |

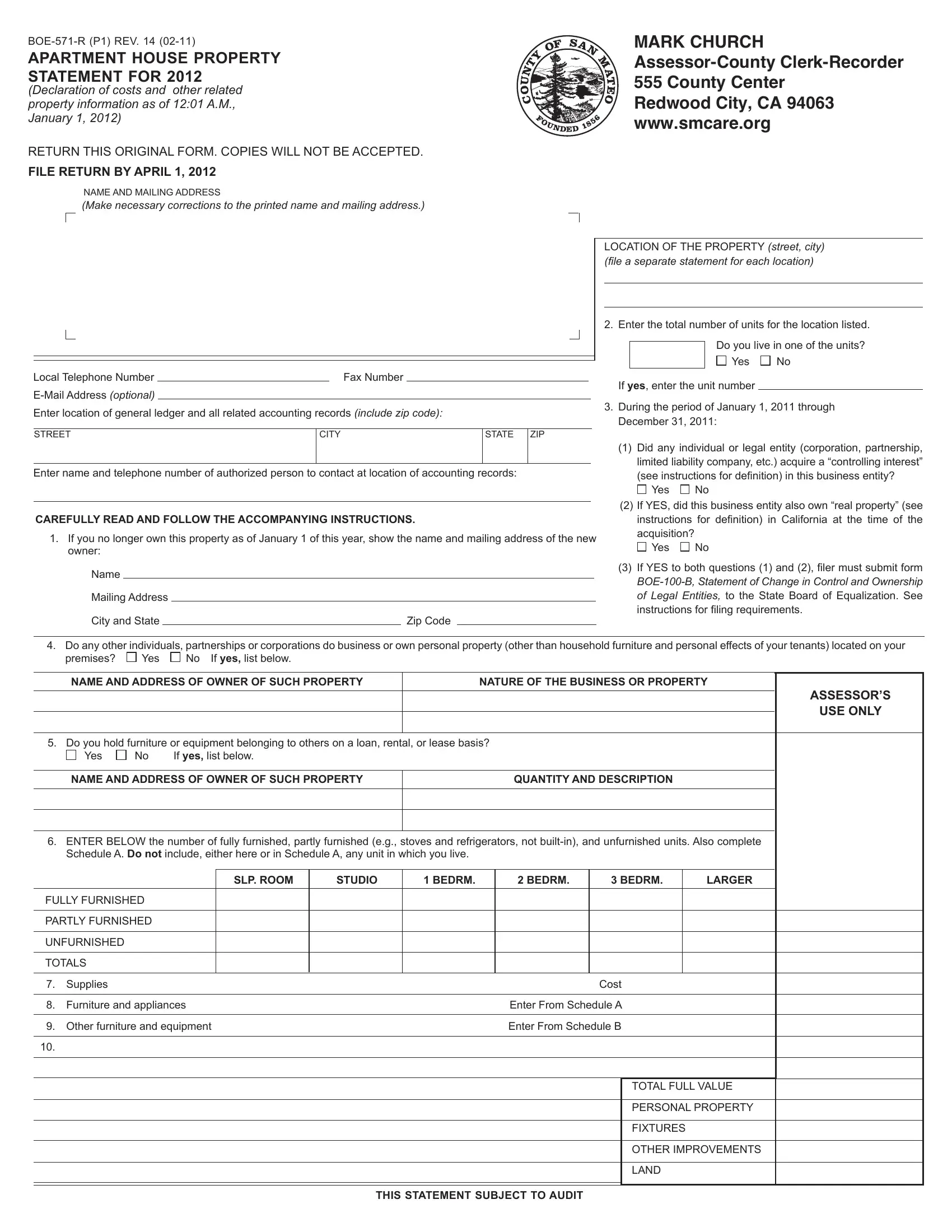

APARTMENT HOUSE PROPERTY

STATEMENT FOR 2012

(Declaration of costs and other related property information as of 12:01 A.M., January 1, 2012)

RETURN THIS ORIGINAL FORM. COPIES WILL NOT BE ACCEPTED.

FILE RETURN BY APRIL 1, 2012

NAME AND MAILING ADDRESS

(Make necessary corrections to the printed name and mailing address.)

MARK CHURCH

Redwood City, CA 94063 www.smcare.org

LOCATION OF THE PROPERTY (street, city) (file a separate statement for each location)

Local Telephone Number |

|

Fax Number |

|

|

|

|

|

|

Enter location of general ledger and all related accounting records (include zip code):

2. Enter the total number of units for the location listed.

Do you live in one of the units?

Yes No

If yes, enter the unit number

3.During the period of January 1, 2011 through December 31, 2011:

STREET |

|

CITY |

|

STATE |

ZIP |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

(1) Did any individual or legal entity (corporation, partnership, |

||

|

|

|

|

|

|

|

|

|

|

|

|

limited liability company, etc.) acquire a “controlling interest” |

||

Enter name and telephone number of authorized person to contact at location of accounting records: |

|

|

|

|

||||||||||

|

|

|

|

(see instructions for definition) in this business entity? |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

Yes |

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

(2) If YES, did this business entity also own “real property” (see |

||

|

|

|

|

|

|

|

|

|

|

|

|

|||

CAREFULLY READ AND FOLLOW THE ACCOMPANYING INSTRUCTIONS. |

|

|

|

|

|

|

instructions for definition) in California at the time of the |

|||||||

1. If you no longer own this property as of January 1 of this year, show the name and mailing address of the new |

acquisition? |

|

||||||||||||

Yes |

No |

|||||||||||||

owner: |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

(3) If YES to both questions (1) and (2), filer must submit form |

||

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|||

Mailing Address |

|

|

|

|

|

|

|

|

|

of Legal Entities, to the State Board of Equalization. See |

||||

|

|

|

|

|

|

|

|

|

|

|

|

instructions for filing requirements. |

||

City and State |

|

|

|

Zip Code |

|

|

|

|

|

|

|

|

||

4. Do any other individuals, partnerships or corporations do business or own personal property (other than household furniture and personal effects of your tenants) located on your

|

premises? |

Yes |

No If yes, list below. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

NAME AND ADDRESS OF OWNER OF SUCH PROPERTY |

|

NATURE OF THE BUSINESS OR PROPERTY |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ASSESSOR’S |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

USE ONLY |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||

5. Do you hold furniture or equipment belonging to others on a loan, rental, or lease basis? |

|

|

|

|

|

|

||||||||

|

Yes |

No |

If yes, list below. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

NAME AND ADDRESS OF OWNER OF SUCH PROPERTY |

|

|

QUANTITY AND DESCRIPTION |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|||||

6. ENTER BELOW the number of fully furnished, partly furnished (e.g., stoves and refrigerators, not |

|

|||||||||||||

|

Schedule A. Do not include, either here or in Schedule A, any unit in which you live. |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SLP. ROOM |

STUDIO |

1 BEDRM. |

|

2 BEDRM. |

3 BEDRM. |

|

LARGER |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

FULLY FURNISHED |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

PARTLY FURNISHED |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNFURNISHED |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTALS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7. |

Supplies |

|

|

|

|

|

|

|

Cost |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

8. |

Furniture and appliances |

|

|

|

Enter From Schedule A |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||

9. Other furniture and equipment |

|

|

|

Enter From Schedule B |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL FULL VALUE |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

PERSONAL PROPERTY |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FIXTURES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

OTHER IMPROVEMENTS |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LAND |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

THIS STATEMENT SUBJECT TO AUDIT |

|

|

|

|

|

|

|||

SCHEDULES OF DEPRECIABLE PROPERTY — SCHEDULES A and B. Items may be listed separately within the year of acquisition on a separate schedule, or items may be grouped by year of acquisition and listed on the schedules below. If you purchased the property as a unit, report on Schedules A & B the previous owner’s original cost by the original year of acquisition of the furniture and equipment that was included in your purchase.

Enter the total installed cost including freight, excise taxes, and sales and use taxes of all furniture, and other equipment located on the premises. Include fully depreciated items. Do not include licensed vehicles. Depreciation schedules may be attached if they provide the desired information.

SCHEDULE A |

FURNITURE AND APPLIANCES (include items in storage; |

SCHEDULE B |

OTHER FURNITURE AND EQUIPMENT (office, lobby, laundry, |

||||||||

do not include |

|

|

pool, vending, signs, fire extinguishers) |

|

|||||||

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Year of |

|

Original Installed Cost |

FOR ASSESSOR’S USE ONLY |

Year of |

|

Original Installed Cost |

FOR ASSESSOR’S USE ONLY |

||||

Acquisition |

|

|

|

Acquisition |

|

|

|

||||

|

(NOT depreciated book value) |

Factor |

Value |

(NOT depreciated book value) |

Factor |

Value |

|||||

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

2011 |

|

|

|

|

|

2011 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2010 |

|

|

|

|

|

2010 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2009 |

|

|

|

|

|

2009 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2008 |

|

|

|

|

|

2008 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2007 |

|

|

|

|

|

2007 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2006 |

|

|

|

|

|

2006 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2005 |

|

|

|

|

|

2005 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2004 |

|

|

|

|

|

2004 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2003 |

|

|

|

|

|

2003 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2002 |

|

|

|

|

|

2002 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2001 |

|

|

|

|

|

2001 |

|

|

|

|

|

& prior |

|

|

|

|

|

& prior |

|

|

|

|

|

TOTAL COST $ |

|

|

|

|

TOTAL COST $ |

|

|

|

|

||

Enter on line 8, page 1. |

|

|

Enter on line 9, page 1. |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

REMARKS:

DECLARATION BY ASSESSEE

Note: The following declaration must be completed and signed. If you do not do so, it may result in penalties.

I declare under penalty of perjury under the laws of the State of California that I have examined this property statement, including accompanying schedules, statements or other attachments, and to the best of my knowledge and belief it is true, correct, and complete and includes all property required to be reported which is owned, claimed, possessed, controlled, or managed by the person named as the assessee in this statement at 12:01 a.m. on January 1, 2012.

OWNERSHIP

TYPE ( )

Proprietorship

Partnership

Corporation

Other

SIGNATURE OF ASSESSEE OR AUTHORIZED AGENT* |

|

|

DATE |

|

|

|

|

NAME OF ASSESSEE OR AUTHORIZED AGENT* (typed or printed) |

|

|

TITLE |

|

|

|

|

NAME OF LEGAL ENTITY (other than DBA) (typed or printed) |

|

|

FEDERAL EMPLOYER ID NUMBER |

|

|

|

|

PREPARER’S NAME AND ADDRESS (typed or printed) |

TELEPHONE NUMBER |

TITLE |

|

|

( |

) |

|

|

|

|

|

*Agent: See page 3 for Declaration by Assessee instructions.

INSTRUCTIONS

The Revenue and Taxation Code of the State of California requires that every person, upon request of the Assessor, shall file a written property statement under penalty of perjury with the Assessor within such time as the Assessor may appoint. Please complete this form according to the numbered instructions provided below as your statement of furnishings and related equipment owned, possessed or controlled by you as of 12:01 a.m., January 1, this year at the location listed. Property which you are purchasing under a conditional sales contract must be included. Return the completed statement form to the Assessor on or before the date stated in the official requirement section. In all instances, you must return the original

LINE 3. PROPERTY TRANSFER

Real Property – For purposes of reporting a change in control, real property includes land, structures, or fixtures owned or held under lease from (1) a private owner if the remaining term of the lease exceeds 35 years, including written renewal options, (2) a public owner (any arm or agency of local, state, or federal government) for any term or (3) mineral rights owned or held on lease for any term, whether in production or not.

Controlling Interest – When any person or legal entity obtains more than 50 percent of the voting stock of a corporation, or more than a 50 percent ownership interest in any other type of legal entity. The interest obtained includes what is acquired directly or indirectly by a parent or affiliated entity.

Forms, Filing Requirements & Penalty Information – Contact the Legal Entity Ownership Program Section at

LINE 4. Check the appropriate box. If yes is checked, enter the name and address of the owner of the furniture or equipment. Briefly describe the nature of the business or property. Do not report household furnishings owned by tenants and used in their living quarters, or other personal property owned or controlled by tenants.

LINE 5. Check the appropriate box. If yes is checked, enter the name and address of the owner or lessor and the quantity and description of the furniture or equipment. The lessor of the items will be asked to declare them.

LINE 6. Enter the number of fully furnished, partly furnished, and unfurnished units in the appropriate column or columns. If the owner of the building (other than a corporation) occupies a unit as his living quarters, do not include it. Please indicate in the REMARKS area the items contained in a typical PARTLY FURNISHED apartment of each size. A sleeping room is a room with no kitchen facilities; a studio contains a kitchen and a convertible living room; a 1 bedrm. contains a bedroom, living room, kitchen, etc. Attach additional sheets if necessary.

LINE 7. Enter the cost of supplies that are on hand at 12:01 a.m. on January 1 of this year. Include janitorial and pool supplies, whether carried in your asset accounts or expensed.

LINES 8 and 9. Enter the total cost from Schedules A and B.

SCHEDULE A.

SCHEDULE B.

DECLARATION BY ASSESSEE

The law requires that this property statement, regardless of where it is executed, shall be declared to be true under penalty of perjury under the laws of the State of California. The declaration must be signed by the assessee, a duly appointed fiduciary, or a person authorized to sign on behalf of the assessee. In the case of a corporation, the declaration must be signed by an officer or by an employee or agent who has been designated in writing by the board of directors, by name or by title, to sign the declaration on behalf of the corporation. In the case of a partnership, the declaration must be signed by a partner or an authorized employee or agent. In the case of a Limited Liability Company (LLC), the declaration must be signed by an LLC manager, or by a member where there is no manager, or by an employee or agent designated by the LLC manager or by the members to sign on behalf of the LLC.

When signed by an employee or agent, other than a member of the bar, a certified public accountant, a public accountant, an enrolled agent or a duly appointed fiduciary, the assessee’s written authorization of the employee or agent to sign the declaration on behalf of the assessee must be filed with the Assessor. The Assessor may at any time require a person who signs a property statement and who is required to have written authorization to provide proof of authorization.

A property statement that is not signed and executed in accordance with the foregoing instructions is not validly filed. The penalty imposed by section 463 of the Revenue and Taxation Code for failure to file is applicable to unsigned property statements.

THIS STATEMENT IS NOT A PUBLIC DOCUMENT. THE INFORMATION DECLARED

WILL BE HELD SECRET BY THE ASSESSOR.