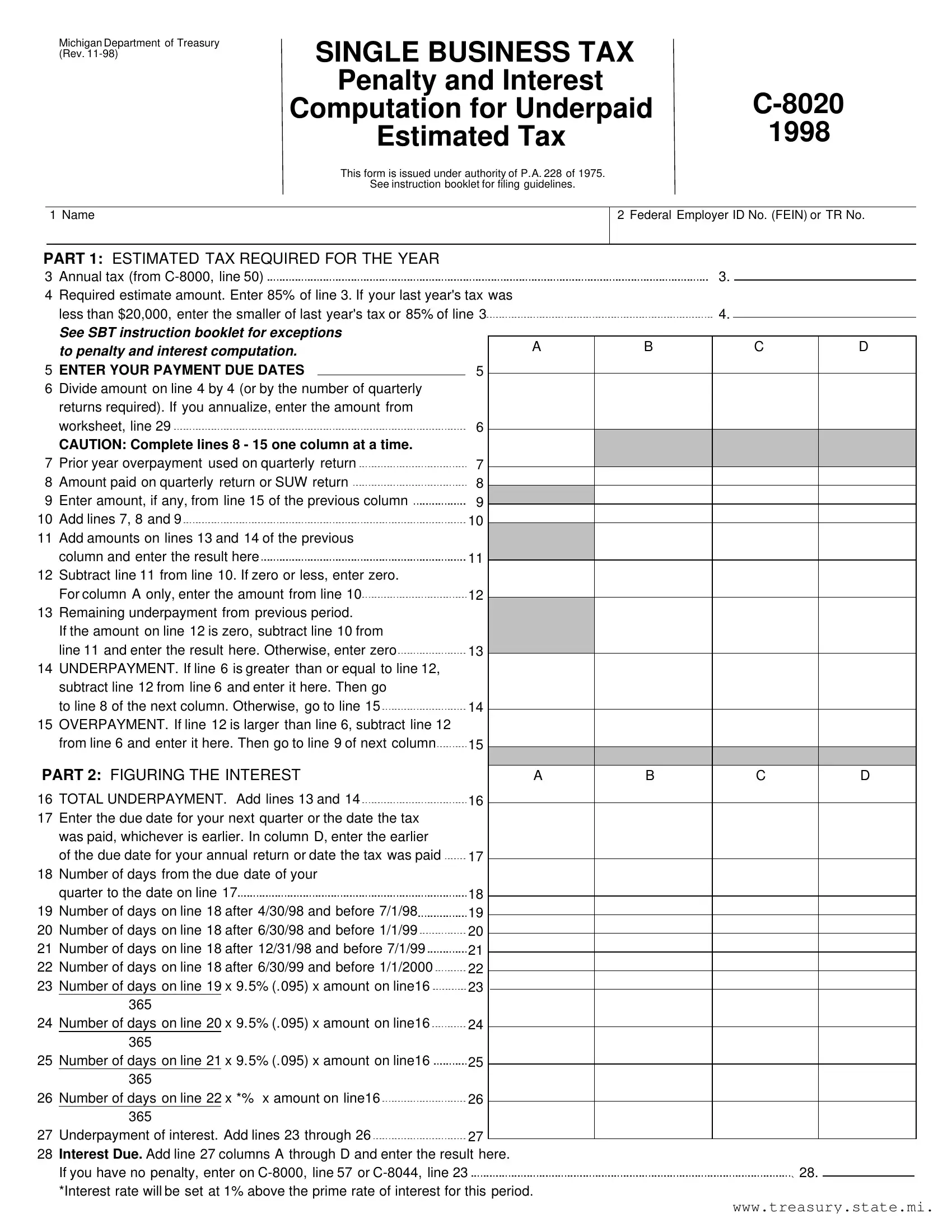

In an effort to streamline the understanding and handling of business taxation, the Michigan Department of Treasury provides a variety of forms, among which is the C-8020 form, specifically designed for the computation of penalties and interest due to underpaid estimated taxes by businesses. Issued under the authority of P.A. 228 of 1975, this form is central to ensuring that businesses meet their tax obligations in a timely and accurate manner. Essentially, it serves as a detailed guide for calculating what a business owes when it falls short of its estimated tax payments throughout the year. The C-8020 form highlights the necessity of not only making these payments but also doing so in a manner that aligns with the state’s fiscal regulations. The form itself is broken down into various parts, including the annual tax estimate required for the year, detailed computation sections for both the penalties and interest that may accrue due to untimely or insufficient quarterly tax payments, and specific schedules to assist businesses in accurately adjusting their payments should their liabilities fluctuate throughout the year. By dividing the estimated tax amount by the required quarterly returns or employing an annualization worksheet for businesses with uneven income distribution across the year, the C-8020 form encapsulates a comprehensive approach to managing and rectifying underpayments, thereby maintaining fiscal responsibility and legal compliance. Additionally, it includes provisions for adjustments and corrections to penalty assessments, offering a structured yet adaptable framework for businesses to navigate their tax responsibilities effectively.

| Question | Answer |

|---|---|

| Form Name | Form C 8020 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | Michigan, 29A, Annualized, FEIN |