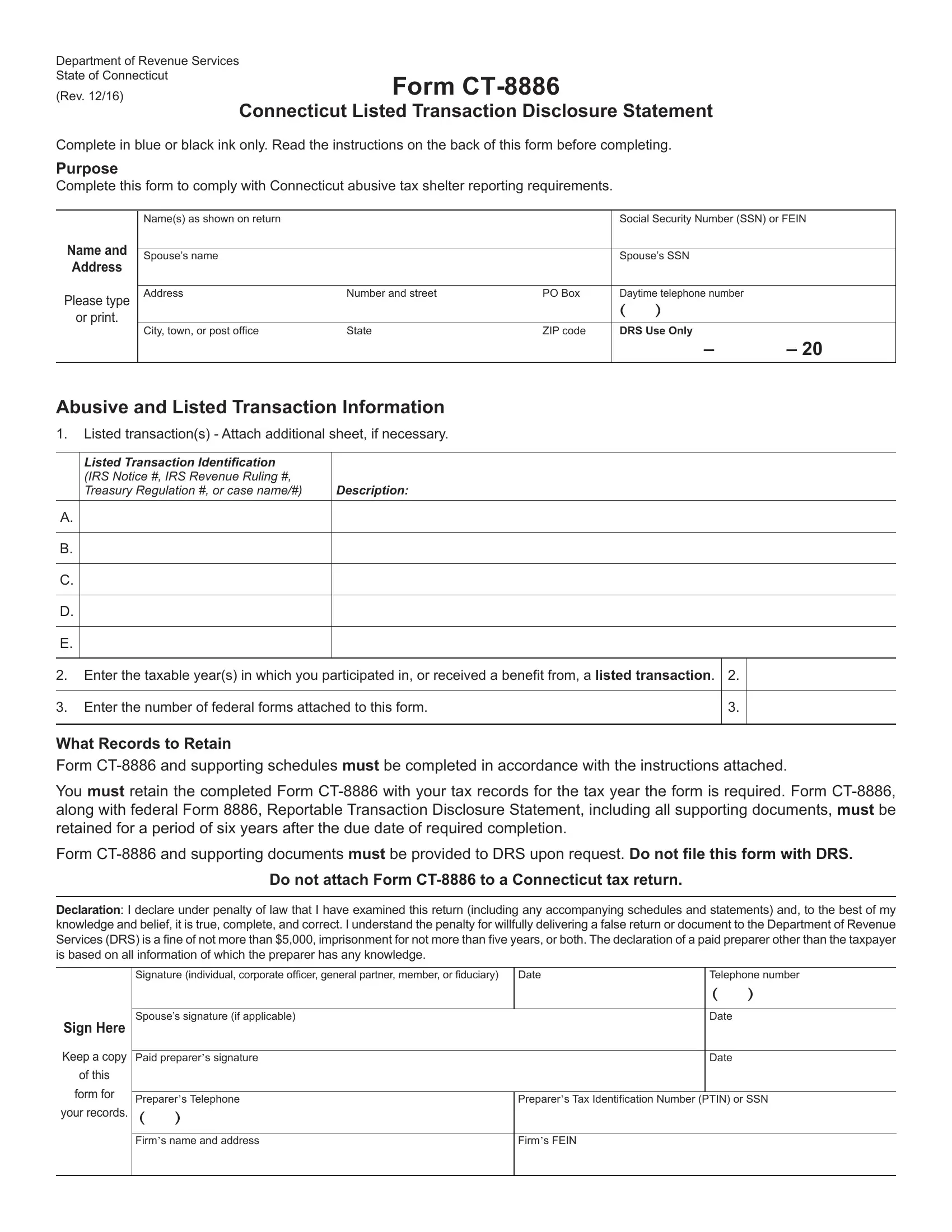

In the landscape of tax regulation, particularly concerning the oversight of abusive tax shelters, the Form CT-8886 emerges as a critical tool within the State of Connecticut. Issued by the Department of Revenue Services, this document, officially titled the Connecticut Listed Transaction Disclosure Statement, mandates comprehensive disclosure from taxpayers involved in "listed transactions." These transactions, earmarked by the Internal Revenue Service (IRS) as potential vehicles for tax avoidance, trigger specific reporting obligations. The form's revision in December 2016 underscores its relevance in the continuous effort to maintain transparency and fairness in tax practices. By mandating detailed information, including the identification of the transaction and the taxable years it impacts, Form CT-8886 plays a pivotal role in the enforcement of tax compliance. Alongside providing details about the transaction, taxpayers are guided to retain this form and all affiliated documentation for a duration extending to six years post the due submission date, reinforcing the long-term accountability in tax reporting. Importantly, this form stretches its applicability across a broad spectrum of taxpayers, including corporations, individuals, partnerships, and other entities, thus casting a wide net in the pursuit of abusive tax shelter deterrence. The declaration and preparer sections further imbue the process with a layer of formal verification, highlighting the seriousness with which the state views accurate disclosure. As a legislative tool, Form CT-8886 illustrates the intricate balance between taxpayer responsibilities and regulatory oversight, aiming to diminish the shadow of tax evasion tactics while ensuring a fair tax operation field for all parties involved.

| Question | Answer |

|---|---|

| Form Name | Form Ct 8886 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | form ct 8886, preparer, llcs, ct 8886 |

Department of Revenue Services State of Connecticut

(Rev. 12/16)

Form

Connecticut Listed Transaction Disclosure Statement

Complete in blue or black ink only. Read the instructions on the back of this form before completing.

Purpose

Complete this form to comply with Connecticut abusive tax shelter reporting requirements.

|

Name(s) as shown on return |

|

|

Social Security Number (SSN) or FEIN |

||

Name and |

|

|

|

|

|

|

Spouse’s name |

|

|

Spouse’s SSN |

|

||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

Please type |

Address |

Number and street |

PO Box |

Daytime telephone number |

|

|

or print. |

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

City, town, or post offi ce |

State |

ZIP code |

DRS Use Only |

|

|

|

|

|

|

|

– |

– 20 |

|

|

|

|

|

|

|

Abusive and Listed Transaction Information

1.Listed transaction(s) - Attach additional sheet, if necessary.

|

Listed Transaction Identification |

|

|

|

|

(IRS Notice #, IRS Revenue Ruling #, |

|

|

|

|

Treasury Regulation #, or case name/#) |

Description: |

|

|

|

|

|

|

|

A. |

|

|

|

|

|

|

|

|

|

B. |

|

|

|

|

|

|

|

|

|

C. |

|

|

|

|

|

|

|

|

|

D. |

|

|

|

|

|

|

|

|

|

E. |

|

|

|

|

|

|

|

|

|

2. Enter the taxable year(s) in which you participated in, or received a benefi t from, a listed transaction. |

2. |

|

||

|

|

|

|

|

3. Enter the number of federal forms attached to this form. |

3. |

|

||

|

|

|

|

|

What Records to Retain

Form

You must retain the completed Form

Form

Do not attach Form

Declaration: I declare under penalty of law that I have examined this return (including any accompanying schedules and statements) and, to the best of my knowledge and belief, it is true, complete, and correct. I understand the penalty for willfully delivering a false return or document to the Department of Revenue Services (DRS) is a fine of not more than $5,000, imprisonment for not more than five years, or both. The declaration of a paid preparer other than the taxpayer is based on all information of which the preparer has any knowledge.

Sign Here

Keep a copy

of this

form for

your records.

Signature (individual, corporate officer, general partner, member, or fiduciary) |

Date |

Telephone number |

||

|

|

|

( |

) |

|

|

|

|

|

Spouse’s signature (if applicable) |

|

Date |

|

|

|

|

|

|

|

Paid preparer’s signature |

|

Date |

|

|

|

|

|

||

Preparer’s Telephone |

Preparer’s Tax Identifi cation Number (PTIN) or SSN |

|||

( |

) |

|

|

|

|

|

|

|

|

Firm’s name and address |

Firm’s FEIN |

|

|

|

|

|

|

|

|

Form

General Information

Taxpayers participating in any tax shelter designated by the Internal Revenue Service (IRS) as an abusive or listed transaction are required to provide DRS with specific information about each listed transaction.

For tax returns (individual or corporation) beginning on or after January 1, 2006, a penalty of 75% of the amount of the deficiency may be imposed when it appears that any part of the deficiency is due to a failure to disclose a listed transaction. DRS may conduct audits of abusive transactions six years after the return was filed.

Also, promoters of abusive tax shelters may be subject to a penalty of 50% of the gross income received from the marketing, soliciting, sale, or promotion of abusive tax shelters.

What is a listed transaction?

A listed transaction is a reportable transaction that is the same as or substantially similar to a transaction the IRS determines to be a tax avoidance transaction and identified by notice, ruling, regulation, or other form of published guidance as a listed transaction. This is true whether or not the IRS has identified the transaction as a listed transaction at the time the taxpayer entered into the transaction.

Who Must Complete Form

Every taxpayer, who is required to file a disclosure statement of listed transactions with the IRS (according to Internal Revenue Code (IRC) §6011 and Treasury Regulation

This form, along with supporting documentation, must be retained for a period of six years after the due date of required completion.

Form

Each taxpayer must make its own disclosure using Form

Taxpayers who may be required to complete this form include:

•Corporations, including limited liability companies (LLCs) treated as a corporation;

•Individuals, including sole proprietors and single member LLCs;

•Partnerships, including LLCs that are treated as a partnership for federal income tax purposes;

•Estates and trusts;

•Partners in a partnership;

•S corporations;

•Shareholders of an S corporation; and

•Benefi ciaries of an estate or trust.

When to Complete Form

Form

For returns filed under Chapter 229 of the Connecticut General Statutes (individuals, partnerships, LLCs, S corporations, trusts and estates), the form must be completed on or before the fifteenth day of the fourth month following the close of the taxpayer’s taxable year.

For returns filed under Chapter 208 of the Connecticut General Statutes (C corporations), the form must be completed on or before the first day of the month next succeeding the due date of the company’s corresponding federal income tax return for the income year or, in the case of any company that is not required to file a federal income tax return for the income year, on or before the first day of the fourth month next succeeding the end of the income year.

What Records to Retain

You must retain the completed Form

Form

Do not attach Form

Specifi c Line Instructions

Line 1

Enter the IRS Notice, IRS Revenue Ruling, Treasury Regulation, case name (and number), or other form of published guidance that identified the listed transaction and provide a description of the listed transaction.

This includes transactions that are the same as or substantially similar to one of the types of transactions that the IRS has determined to be a tax avoidance transaction.

The IRS list of abusive or listed transactions is available by visiting the IRS website at www.irs.gov/businesses/corporations and selecting Abusive Tax Shelters and Transactions. The listed transactions is also periodically updated in issues of the IRS Internal Revenue Bulletin.

Line 2

Enter the taxable year(s) in which you participated in, or received a benefit from a listed transaction. This disclosure must be made for each taxable year for which a taxpayer participates in a listed transaction.

Line 3

Enter the number of IRS Form(s) 8886 and Schedule(s)

Signature

You must sign this form. If you are completing Form

Paid Preparer’s Signature

Anyone you pay to prepare your return must sign and date it. Paid preparers must also enter their Social Security Number (SSN) or Personal Tax Identification Number (PTIN), their firm’s Federal Employer Identification Number (FEIN), and the firm’s address and telephone number.

For Further Information

Visit the DRS Web site at www.ct.gov/DRS or for personal telephone assistance call the Corporation and

Form