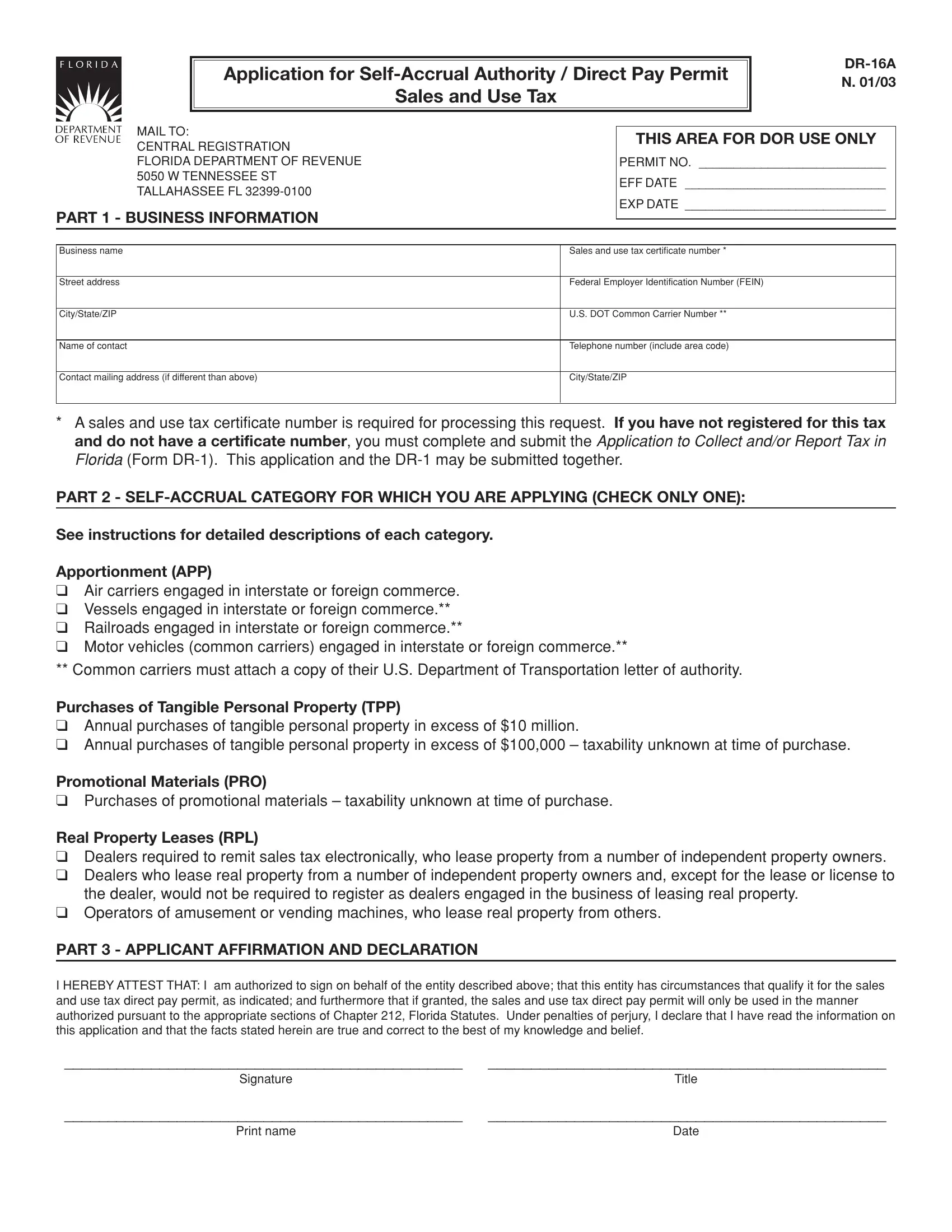

The Application for Self-Accrual Authority / Direct Pay Permit Sales and Use Tax, known as the DR-16A form, plays a critical role for businesses operating within Florida. This document is designed for entities seeking permission to self-accrue sales and use taxes, a process that allows them to directly remit tax payments to the state rather than through vendors at the point of sale. Required by the Florida Department of Revenue, the form requests detailed business information, including the business's name, Federal Employer Identification Number (FEIN), and sales and use tax certificate number, which is pivotal for the processing of this request. The form delineates multiple self-accrual categories, such as Apportionment for various carriers in interstate or foreign commerce, Purchases of Tangible Personal Property by entities with substantial annual purchases, and others, accommodating a range of business activities. Additionally, promotional materials and real property leases are specific categories that address the unique situations of dealers and operators. Applicants must affirm their eligibility and declare their knowledge of the facts under penalties of perjury, ensuring that only qualified entities receive this authority. Completing the DR-16A form accurately is essential for businesses aiming to leverage the direct pay permit, emphasizing the importance of understanding the form’s intricacies and the statutory requirements it entails.

| Question | Answer |

|---|---|

| Form Name | Form Dr 16A |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | tax5 texas direct pay permit form |

Application for

Sales and Use Tax

MAIL TO:

CENTRAL REGISTRATION

FLORIDA DEPARTMENT OF REVENUE 5050 W TENNESSEE ST TALLAHASSEE FL

PART 1 - BUSINESS INFORMATION

THIS AREA FOR DOR USE ONLY

PERMIT NO. ___________________________

EFF DATE _____________________________

EXP DATE _____________________________

Business name |

Sales and use tax certificate number * |

|

|

Street address |

Federal Employer Identification Number (FEIN) |

|

|

City/State/ZIP |

U.S. DOT Common Carrier Number ** |

|

|

Name of contact |

Telephone number (include area code) |

|

|

Contact mailing address (if different than above) |

City/State/ZIP |

|

|

*A sales and use tax certificate number is required for processing this request. If you have not registered for this tax and do not have a certificate number, you must complete and submit the Application to Collect and/or Report Tax in Florida (Form

PART 2 -

See instructions for detailed descriptions of each category.

Apportionment (APP)

❑Air carriers engaged in interstate or foreign commerce.

❑Vessels engaged in interstate or foreign commerce.**

❑Railroads engaged in interstate or foreign commerce.**

❑Motor vehicles (common carriers) engaged in interstate or foreign commerce.**

** Common carriers must attach a copy of their U.S. Department of Transportation letter of authority.

Purchases of Tangible Personal Property (TPP)

❑Annual purchases of tangible personal property in excess of $10 million.

❑Annual purchases of tangible personal property in excess of $100,000 – taxability unknown at time of purchase.

Promotional Materials (PRO)

❑Purchases of promotional materials – taxability unknown at time of purchase.

Real Property Leases (RPL)

❑Dealers required to remit sales tax electronically, who lease property from a number of independent property owners.

❑Dealers who lease real property from a number of independent property owners and, except for the lease or license to the dealer, would not be required to register as dealers engaged in the business of leasing real property.

❑Operators of amusement or vending machines, who lease real property from others.

PART 3 - APPLICANT AFFIRMATION AND DECLARATION

I HEREBY ATTEST THAT: I am authorized to sign on behalf of the entity described above; that this entity has circumstances that qualify it for the sales and use tax direct pay permit, as indicated; and furthermore that if granted, the sales and use tax direct pay permit will only be used in the manner authorized pursuant to the appropriate sections of Chapter 212, Florida Statutes. Under penalties of perjury, I declare that I have read the information on this application and that the facts stated herein are true and correct to the best of my knowledge and belief.

______________________________________________ |

______________________________________________ |

Signature |

Title |

______________________________________________ |

______________________________________________ |

Print name |

Date |

Information and Instructions for Completing Application

for

Sales and Use Tax

N.01/03 Page 2

Chapter 212, Florida Statutes, provides that

Instructions for Completing the Application

Review the

Note the specific uses of the direct pay permit, if granted.

Complete Parts 1 and 2.

Read and sign Part 3.

If you are a common carrier and are applying under the apportionment category, you must attach a copy of your U.S. Department of Transportation (DOT) letter of authority.

Note: Incomplete or unsigned applications will be returned, thus delaying the issuance of the direct pay permit.

Mail or deliver your completed application to:

CENTRAL REGISTRATION

FLORIDA DEPARTMENT OF REVENUE 5050 W TENNESSEE ST TALLAHASSEE FL

Apportionment (APP)

•The apportionment of tax by eligible air carriers for the purchase or use of tangible personal property, as provided in section 212.0598, F.S.

•The partial exemption applicable to vessels and parts thereof used in interstate or foreign commerce for the purchase of vessels and parts thereof, as provided in s. 212.08(8), F.S., and Rule

•The partial exemption applicable to railroads and parts thereof used in interstate or foreign commerce by licensed railroad carriers for purchases of tangible personal property, as provided in s. 212.08(9)(a), F.S., and Rule

•The partial exemption applicable to motor vehicles and parts thereof used in interstate or foreign commerce by licensed common carriers, as provided in s. 212.08(9)(b), F.S., and Rule

Purchases of Tangible Personal Property (TPP)

•The purchase of tangible personal property by dealers who annually purchase in excess of $10 million of taxable tangible personal property in any county for the dealer’s own use.

•The purchase of tangible personal property by dealers who annually purchase at least $100,000 of taxable tangible personal property, including maintenance and repairs for the dealer’s own use, when the taxable status of such property will be known only upon its use. The taxable status of the

property will be known upon its use when the dealer’s normal trade or business characteristics require the dealer to purchase tangible personal property that will either become a component part of a product manufactured for sale or will be used and consumed by the dealer.

Promotional Materials (PRO)

•The purchase of promotional materials, as defined in s. 212.06(11)(b), F.S., by dealers who are unable to determine at the time of purchase whether the promotional materials will be used in this state or exported from this state only when the seller of promoted subscriptions to publications sold in this state is a registered dealer and is remitting sales tax to the Department on publications sold in this state. The dealer purchasing and distributing promotional materials and the seller of the promoted subscriptions to publications are not required to be the same person.

Real Property Leases (RPL)

•The lease or license to use real property subject to tax under s. 212.031, F.S., by dealers who are required to remit sales tax electronically, as provided under s. 213.755, F.S., from a number of independent owners or lessors of real property.

•The lease of or license to use real property subject to the tax imposed by s. 212.031, F.S., by a dealer who leases or obtains licenses to use real property from a number of independent property owners who, except for the lease or license to the dealer, would not be required to register as dealers engaged in the business of leasing real property.

•The lease or license to use real property subject to the tax imposed by s. 212.031, F.S., by operators of amusement machines or vending machines who lease or obtain licenses to use real property from property owners or lessors for the purpose of placing and operating an amusement or vending machine.

For more information:

Information and forms are available on our Internet site at www.myflorida.com/dor

For general information about sales and use tax, call Taxpayer Services, Monday through Friday, 8 a.m. to 7 p.m., ET, at

For assistance with this application, call Central Registration, Monday through Friday, 8 a.m. to 5 p.m., ET, at