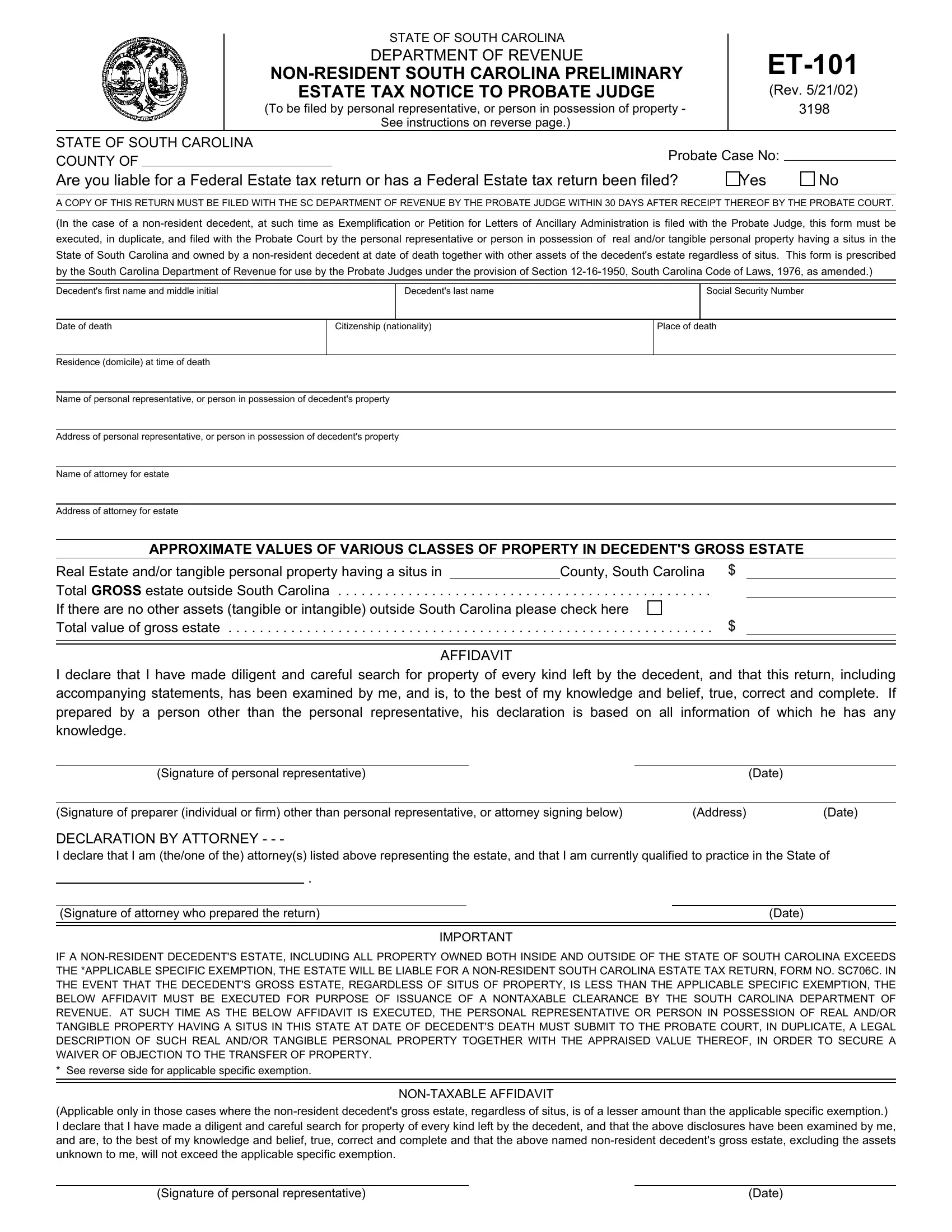

In the State of South Carolina, the handling of a non-resident decedent's estate involves specific procedures that are outlined in the ET-101 form, issued by the Department of Revenue. This Preliminary Estate Tax Notice must be filed with the local Probate Judge by the personal representative or the individual in possession of the decedent's property. Its primary purpose is to notify regarding the estate's tax liabilities in South Carolina, especially focusing on real and/or tangible personal property located within the state. Essential details required by the form include information about the decedent, such as name, social security number, date and place of death, citizenship, residency at the time of death, and approximate values of various classes of property within the gross estate. Furthermore, it mandates an affidavit by the personal representative affirming a diligent search for the decedent's property and attesting to the truthfulness and completeness of the return. For non-resident decedents, the form also stipulates the conditions under which the estate would be liable for a non-resident South Carolina Estate Tax Return (Form SC706C), depending on the specific exemption applicable at the date of death. This document is crucial for both compliance with state tax obligations and the smooth administration of the estate, emphasizing the importance of accurate and timely filing.

| Question | Answer |

|---|---|

| Form Name | Form Et 101 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | ET101 what is the address to file south carolina form et 101 |

STATE OF SOUTH CAROLINA

DEPARTMENT OF REVENUE

ESTATE TAX NOTICE TO PROBATE JUDGE

(To be filed by personal representative, or person in possession of property -

See instructions on reverse page.)

(Rev. 5/21/02) 3198

STATE OF SOUTH CAROLINA

COUNTY OF |

|

Probate Case No: |

|

|

|

|

|

|

|

Are you liable for a Federal Estate tax return or has a Federal Estate tax return been filed? |

Yes |

No |

||

A COPY OF THIS RETURN MUST BE FILED WITH THE SC DEPARTMENT OF REVENUE BY THE PROBATE JUDGE WITHIN 30 DAYS AFTER RECEIPT THEREOF BY THE PROBATE COURT.

(In the case of a

Decedent's first name and middle initial |

|

Decedent's last name |

|

|

Social Security Number |

|||

|

|

|

|

|

|

|

|

|

Date of death |

|

Citizenship (nationality) |

|

Place of death |

||||

|

|

|

|

|

|

|

|

|

Residence (domicile) at time of death |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of personal representative, or person in possession of decedent's property |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

Address of personal representative, or person in possession of decedent's property |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

Name of attorney for estate |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of attorney for estate |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

APPROXIMATE VALUES OF VARIOUS CLASSES OF PROPERTY IN DECEDENT'S GROSS ESTATE |

||||||||

Real Estate and/or tangible personal property having a situs in |

|

County, South Carolina $ |

|

|||||

Total GROSS estate outside South Carolina |

. . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . |

. |

|

|||

If there are no other assets (tangible or intangible) outside South Carolina please check here |

||||||||

Total value of gross estate |

. . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . $ |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

AFFIDAVIT

I declare that I have made diligent and careful search for property of every kind left by the decedent, and that this return, including accompanying statements, has been examined by me, and is, to the best of my knowledge and belief, true, correct and complete. If prepared by a person other than the personal representative, his declaration is based on all information of which he has any knowledge.

(Signature of personal representative) |

|

(Date) |

|

|

|

(Signature of preparer (individual or firm) other than personal representative, or attorney signing below) |

(Address) |

(Date) |

DECLARATION BY ATTORNEY - - -

I declare that I am (the/one of the) attorney(s) listed above representing the estate, and that I am currently qualified to practice in the State of

.

(Signature of attorney who prepared the return) |

(Date) |

|

|

IMPORTANT

IF A

* See reverse side for applicable specific exemption.

(Applicable only in those cases where the

(Signature of personal representative) |

(Date) |

Date of Death |

Applicable Specific Exemption |

||

January 1, 1962 |

- December 31, 1978 |

$60,000 |

|

January 1, 1979 |

- June 30, 1988 |

120,000 |

|

July 1, 1988 |

- June 30, 1989 |

140,000 |

|

July 1, 1989 |

- June 30, 1990 |

170,000 |

|

July 1, 1990 |

- June 30, 1991 |

320,000 |

|

July 1, 1991 |

- thereafter |

same as Federal |

|

Requirement of notice - This notice must be filed with the Probate Judge for the estate of every

Time for filing notice - In the absence of an ancillary administration in this state, the notice must be filed together with exemplifications with the Probate Judge of the county in which the property is located, within 90 days from date of death. If the property is in several counties, file in the county in which the greater part of the property is located, within 90 days after date of death. When an ancillary administration is commenced, the notice must accompany the Petition for Letters of Ancillary Administration.

Persons required to file notice - The duly qualified personal representative, or any person in actual or constructive possession of property included in the statutory gross estate, must file this notice as follows: (1) The personal representative, qualified under an appointment by a court, must file the notice unless at the time of his qualification the notice has already been filed; (2) Any person in actual or constructive possession of property included in the statutory gross estate, must file the notice unless a personal representative qualifies within 3 months after the decedent's death. Persons in actual or constructive possession of such property include custodians, fiduciaries, transferees, joint owners, partners, distributees, debtors, agents, factors, brokers, bankers, safe deposit companies, and warehouse companies.

Signature - The signature of one personal representative is sufficient. If this form is filed by a person other than the personal representative, such person must sign this form and should use a descriptive title such as stated in the last sentence of the above paragraph.

Gross estate - The gross estate, as defined in Section 2031

(a)of the Internal Revenue Code adopted by reference for South Carolina estate tax purposes comprises property of the decedent wherever situated and includes:

1.Property in which the decedent, at the time of his death, has any beneficial interest.

2.Interest of surviving spouse, as dower, curtesy, or estate in lieu thereof.

3.Property transferred by the decedent during his life, by trust or otherwise (other than by bona fide sale for an adequate and full consideration in money or money's worth) as follows: (1) Transfers intended to take effect in possession or enjoyment at or after the decedent's death; (2) Transfers under which the decedent reserved or retained (in whole or in part) the use, possession, rents, or other income or enjoyment of the transferred property, for his life, or for a period not ascertainable without reference to his death, or for a period of such duration as to evidence an intention that it should extend to his death; (3) Transfers under which the decedent retained the right, either alone or in conjunction with another person or persons, to designate who should possess or enjoy the property or the income therefrom; and (4) Transfers under which the enjoyment of the transferred property was subject at decedent's death to a change through the exercise, either by the decedent alone or in conjunction with another person or persons, of a power to alter, amend, revoke or terminate.

4.Annuities received by any beneficiary by reason of surviving the decedent.

5.Property owned jointly or in tenancy with right of survivorship.

6.Property subject to a general power of appointment, including property with respect to which the decedent exercised or released the power during his lifetime.

7.Insurance upon the life of the decedent, including insurance receivable by beneficiaries other than the estate.

For decedents dying on or after July 1, 1991: South Carolina has adopted the Internal Revenue Code Section 2011. The term "Federal Credit" means the maximum amount of the credit for state death taxes allowable by the Internal Revenue Code Section 2011. The term "maximum amount" must be construed so as to take full advantage of the credit as allowed by the Internal Revenue Code.

Lien - A lien upon the property of a

Penalties - Penalties are provided for under Chapter 54 of Title 12.