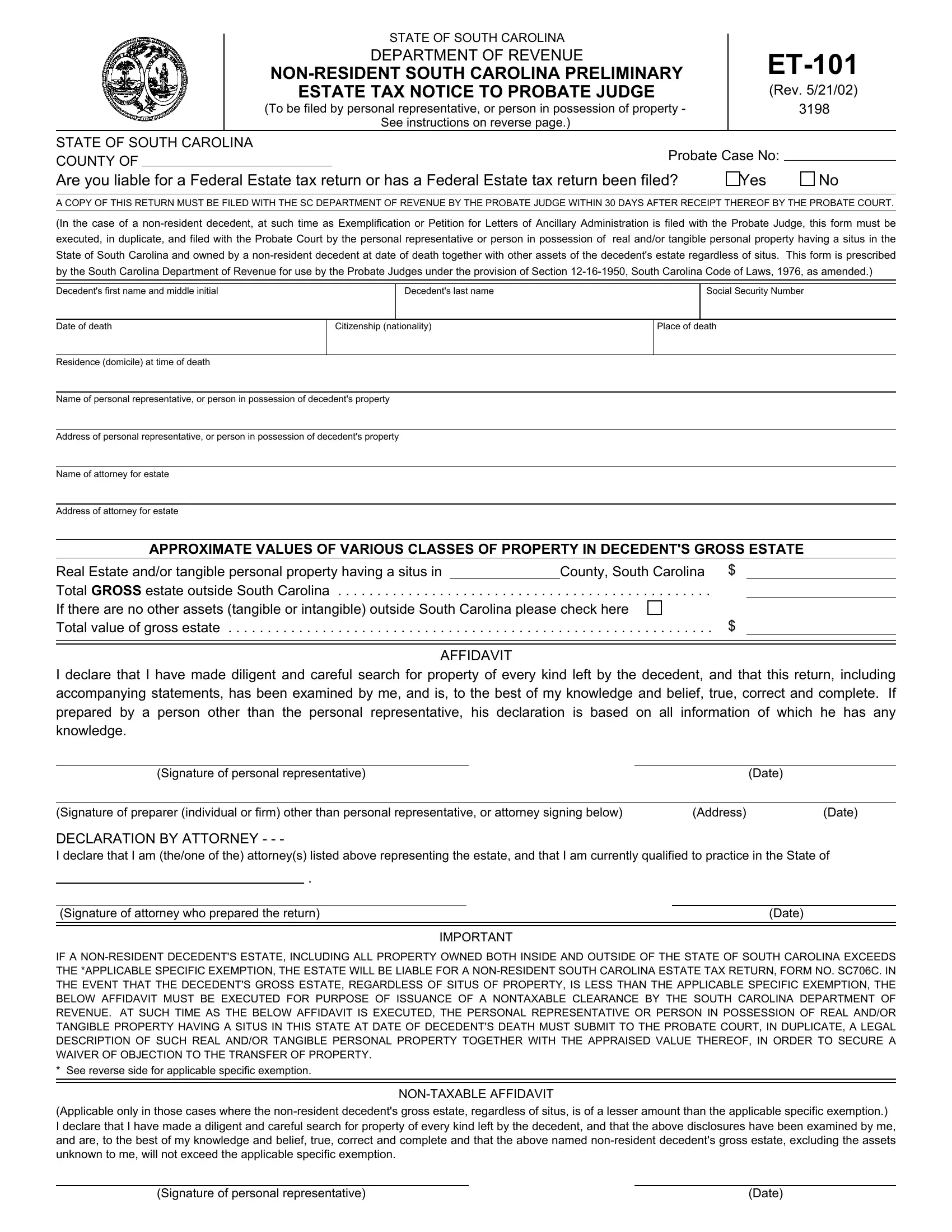

In the State of South Carolina, the handling of a non-resident decedent's estate involves specific procedures that are outlined in the ET-101 form, issued by the Department of Revenue. This Preliminary Estate Tax Notice must be filed with the local Probate Judge by the personal representative or the individual in possession of the decedent's property. Its primary purpose is to notify regarding the estate's tax liabilities in South Carolina, especially focusing on real and/or tangible personal property located within the state. Essential details required by the form include information about the decedent, such as name, social security number, date and place of death, citizenship, residency at the time of death, and approximate values of various classes of property within the gross estate. Furthermore, it mandates an affidavit by the personal representative affirming a diligent search for the decedent's property and attesting to the truthfulness and completeness of the return. For non-resident decedents, the form also stipulates the conditions under which the estate would be liable for a non-resident South Carolina Estate Tax Return (Form SC706C), depending on the specific exemption applicable at the date of death. This document is crucial for both compliance with state tax obligations and the smooth administration of the estate, emphasizing the importance of accurate and timely filing.

| Question | Answer |

|---|---|

| Form Name | Form Et 101 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | ET101 what is the address to file south carolina form et 101 |