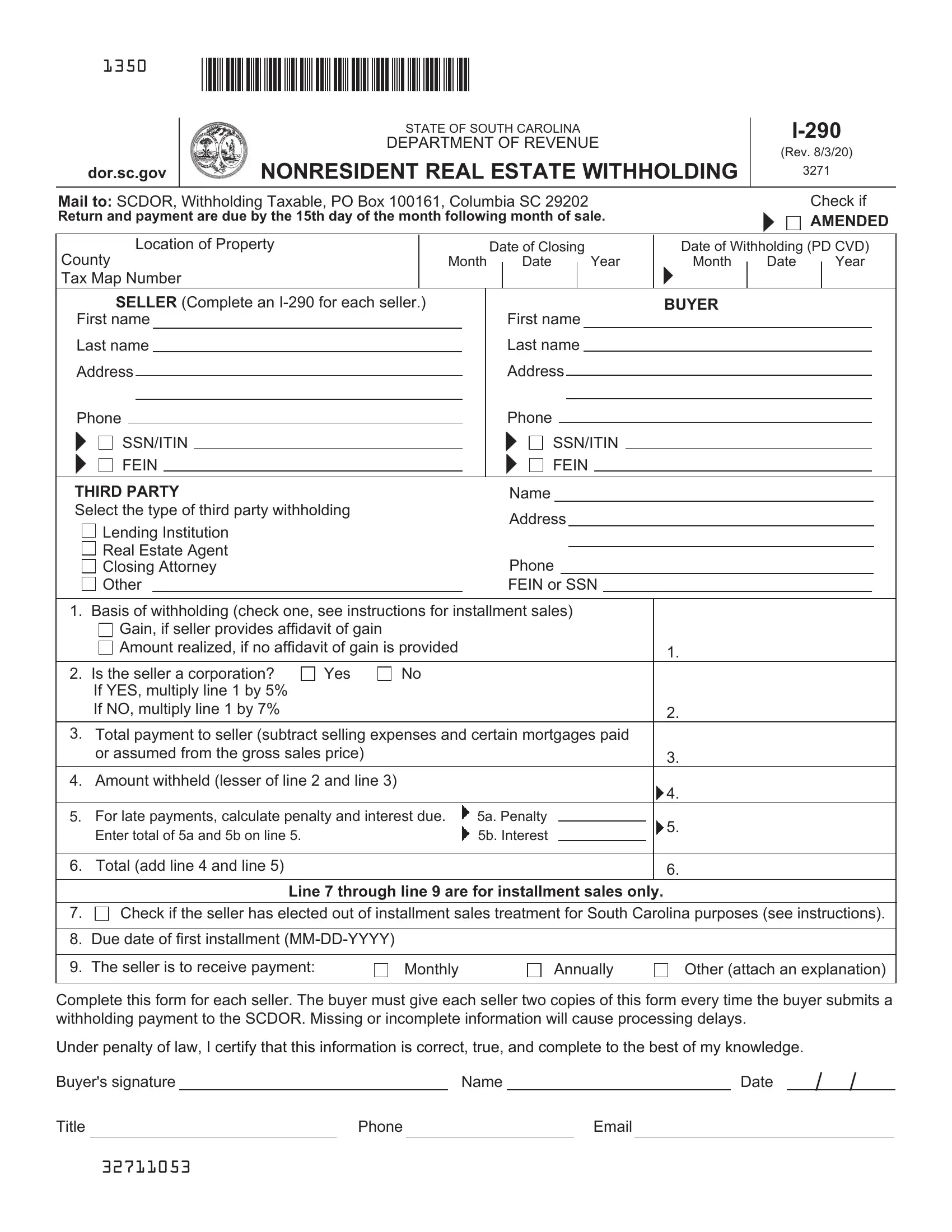

Understanding the nuances and requirements of the I-290 form is essential for anyone involved in the sale of real property to nonresidents in South Carolina. This form, issued by the State of South Carolina Department of Revenue, is pivotal for ensuring compliance with nonresident real estate withholding tax obligations. Whether you are a seller, buyer, or acting as a third party such as a real estate agent or attorney, familiarizing yourself with the form’s specific line items and deadlines can streamline the transaction process. It outlines the need for detailed information about both parties, the property, and the sale, including the calculation of withholding tax based on various conditions. Additionally, it sets forth requirements for installment sales and provides directives for cases where amendments are necessary. The significance of accurate, timely submission cannot be overstated, as this affects the handling of taxes related to the sale and can impact the financial responsibilities of both buyers and sellers. Notably, the I-290 form serves not only as a means of tax withholding but also as a document that facilitates the proper reporting and potential refunding of withheld amounts under specific conditions. Compliance with these regulations supports a transparent, accountable property transfer process, reinforcing the importance of this document in the realm of real estate transactions within the state.

| Question | Answer |

|---|---|

| Form Name | Form I 290 |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | how to sc i 290, sc i 290, sc revenue ruling 09 13, form i290 |

1350

|

|

|

|

|

|

|

|

|

|

|

|

STATE OF SOUTH CAROLINA |

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

DEPARTMENT OF REVENUE |

|

|

(Rev. 8/3/20) |

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

dor.sc.gov |

|

NONRESIDENT REAL ESTATE WITHHOLDING |

|

|

3271 |

|

|

||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

Mail to: SCDOR, Withholding Taxable, PO Box 100161, Columbia SC 29202 |

|

|

|

|

|

|

|

|

|

Check if |

||||||||||||||||||||||||||||||

Return and payment are due by the 15th day of the month following month of sale. |

|

|

|

AMENDED |

||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

Location of Property |

|

|

|

|

|

Date of Closing |

|

|

|

|

|

|

Date of Withholding (PD CVD) |

|||||||||||||||||||||||||

County |

|

|

|

Month |

|

|

Date |

|

|

|

Year |

|

Month |

|

Date |

|

Year |

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

Tax Map Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

SELLER (Complete an |

|

|

|

|

First name |

|

|

|

|

|

|

|

BUYER |

|

|

|

|

|

|

||||||||||||||||||||

First name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

Last name |

|

|

|

|

|

|

|

|

|

Last name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

Phone |

|

|

|

|

|

|

|

|

|

|

|

|

|

Phone |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

SSN/ITIN |

|

|

|

|

|

|

|

|

|

SSN/ITIN |

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

FEIN |

|

|

|

|

|

|

|

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

THIRD PARTY |

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

Select the type of third party withholding |

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

Lending Institution |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Real Estate Agent |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

Phone |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

Closing Attorney |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

Other |

|

|

|

|

|

|

|

|

FEIN or SSN |

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. Basis of withholding (check one, see instructions for installment sales) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

Gain, if seller provides affidavit of gain |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Amount realized, if no affidavit of gain is provided |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Is the seller a corporation? |

Yes |

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

If YES, multiply line 1 by 5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

If NO, multiply line 1 by 7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. Total payment to seller (subtract selling expenses and certain mortgages paid |

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||

|

or assumed from the gross sales price) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. Amount withheld (lesser of line 2 and line 3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

For late payments, calculate penalty and interest due. |

5a. Penalty |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

|

|

|

|

|

|

|||||||||||||||||

|

Enter total of 5a and 5b on line 5. |

|

|

|

5b. Interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

6. Total (add line 4 and line 5) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6. |

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

Line 7 through line 9 are for installment sales only. |

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||||||

7. |

Check if the seller has elected out of installment sales treatment for South Carolina purposes (see instructions). |

|||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

8. Due date of first installment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

9. |

The seller is to receive payment: |

|

Monthly |

|

|

|

|

Annually |

Other (attach an explanation) |

|||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Complete this form for each seller. The buyer must give each seller two copies of this form every time the buyer submits a withholding payment to the SCDOR. Missing or incomplete information will cause processing delays.

Under penalty of law, I certify that this information is correct, true, and complete to the best of my knowledge.

Buyer's signature |

|

|

|

Name |

|

|

|

Date |

/ |

/ |

|

Title |

|

|

Phone |

|

|

|

|

|

|||

32711053

INSTRUCTIONS

Anyone making payment to a nonresident seller for the purchase of real property or real and associated tangible personal property must deduct and withhold on the sale. For more information, see SC Revenue Ruling

Enter the:

•Location of property

•Date of withholding (date of payment)

•Seller's name and address

•Seller's SSN, ITIN, or FEIN

•Buyer's name

•Buyer's SSN, ITIN, or FEIN, and

•Date of closing (date of sale of property)

If the seller is a Partnership, S Corporation, Estate, or Trust, enter the entity name in the seller's first name field. If you don't provide complete information about the buyer, seller, and property, we will not be able to process the return.

Only in the case of installment sales will the date of withholding and the date of closing be a different date.

Complete four copies of this form for each sale. The buyer receives two copies, one to keep for their records and one to send to the SCDOR with the withholding payment. The seller receives two copies, one to include with their Income Tax return and one to keep for their records.

Send the withholding to the SCDOR by the 15th day of the month following the month of the sale. Withholding on an installment sale is not required if the total amount required to be withheld for the entire year would be less than $350.

If the amount to be withheld on installment sales is less than $500, the buyer may wait to submit withholding payments until the month when the amount equals $500 or more. If amounts withheld during a calendar year are more than $350 but less than $500, they must be sent to the SCDOR by January 15 of the following year.

Common questions:

•How do I request a refund for the amount withheld?

To request a refund for the withholding prior to the end of the tax year of the sale, file the

•How do I claim credit for the amount withheld?

When you file your Income Tax return, report the capital gain from the sale as income. Take credit for the Nonresident Real Estate Withholding on the appropriate line in the payments/withholding section of your Income Tax return.

•How do I complete the form for more than one seller?

If there is more than one seller (filing separate Individual Income Tax returns), then separate

•What if the buyer or seller has no SSN? They should apply for an ITIN at irs.gov.

Line instructions:

Line 1: Enter the amount of gain or amount realized from the sale. Subtract the selling expenses from the selling price to compute the amount realized. Use the definition of amount realized found in IRC Section 1001(b). Subtract the basis of the property from the amount realized to compute the gain or loss. If the seller provides the buyer with an

If the transaction reported is an installment sale, enter on line 1 only the portion of gain (if the seller provided an affidavit of gain) or the portion of the amount realized (if the seller does not provide an affidavit of gain) the withholding payment is based upon. If the seller makes the election on line 7 and provides an

Line 2: Check the appropriate box and multiply by the amount on line 1.

Line 3: Enter the total payment made to the seller. The total payment is the gross sales price reduced by any selling expenses and certain mortgages paid or assumed. Selling expenses include real estate commissions, advertising fees, legal fees, deed recording fees, and termite or heat/air letter fees. Reduce the sales price by mortgages or liens paid at closing on the property being sold. Do not deduct any mortgages, liens, advances on credit lines, or other debt secured by the properties and assumed by the buyer in contemplation of the sale. Loans or advances where the entire proceeds are used to purchase or improve the property being sold are not loans in contemplation of the sale.

Unless the buyer knows otherwise, the buyer can presume that any liens, mortgages, or advances on credit lines made more than one year before the closing are not in contemplation of the sale and may be deducted. If the lien, mortgage, or credit line advance is made less than one year prior to the closing, the buyer cannot deduct the mortgage, lien, or credit line advance unless the buyer obtains an affidavit from the seller, stating that the loan or advance was not made in contemplation of the sale.

Line 5: The return and payment are due by the 15th day of the month following the month of the sale. If the payment is late, enter penalty and interest. A Penalty and Interest Calculator is available at dor.sc.gov/calculator.

Line 7: The seller may give the buyer an affidavit

Amended returns:

Check the Amended box and follow instructions on the previous page, making whatever changes are necessary. Attach a copy of your original

An amended

original

Why file an amended

•No affidavit

•Overstatement of gain: A refund can be issued from an amended

•Calculation error: A refund can be issued from an amended

The net capital gain calculation is not taken into consideration when figuring the 7% Nonresident Seller Withholding. The capital gain is only reported with the filing of the Individual Income Tax return.

If filing an amended

SCDOR, PO Box 125, Columbia, SC,

If filing an amended

SCDOR, Withholding Taxable, PO Box 100161, Columbia, SC, 29202

Social Security Privacy Act Disclosure

It is mandatory that you provide your Social Security Number on this tax form if you are an individual taxpayer. 42 U.S.C. 405(c)(2)(C)(i) permits a state to use an individual's Social Security Number as means of identification in administration of any tax. SC Regulation

The Family Privacy Protection Act

Under the Family Privacy Protection Act, the collection of personal information from citizens by the SCDOR is limited to the information necessary for the SCDOR to fulfill its statutory duties. In most instances, once this information is collected by the SCDOR, it is protected by law from public disclosure. In those situations where public disclosure is not prohibited, the Family Privacy Protection Act prevents such information from being used by third parties for commercial solicitation purposes.