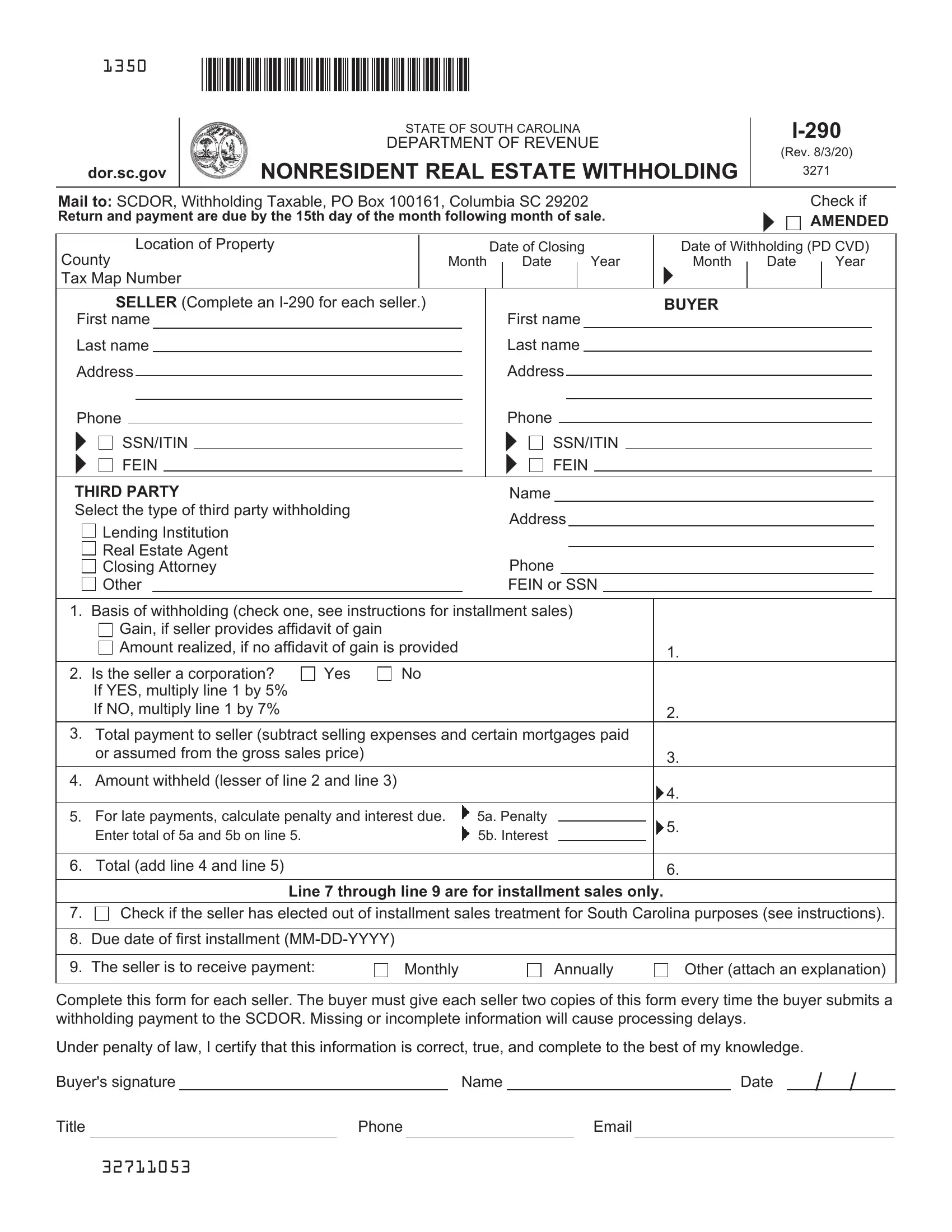

Understanding the nuances and requirements of the I-290 form is essential for anyone involved in the sale of real property to nonresidents in South Carolina. This form, issued by the State of South Carolina Department of Revenue, is pivotal for ensuring compliance with nonresident real estate withholding tax obligations. Whether you are a seller, buyer, or acting as a third party such as a real estate agent or attorney, familiarizing yourself with the form’s specific line items and deadlines can streamline the transaction process. It outlines the need for detailed information about both parties, the property, and the sale, including the calculation of withholding tax based on various conditions. Additionally, it sets forth requirements for installment sales and provides directives for cases where amendments are necessary. The significance of accurate, timely submission cannot be overstated, as this affects the handling of taxes related to the sale and can impact the financial responsibilities of both buyers and sellers. Notably, the I-290 form serves not only as a means of tax withholding but also as a document that facilitates the proper reporting and potential refunding of withheld amounts under specific conditions. Compliance with these regulations supports a transparent, accountable property transfer process, reinforcing the importance of this document in the realm of real estate transactions within the state.

| Question | Answer |

|---|---|

| Form Name | Form I 290 |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | how to sc i 290, sc i 290, sc revenue ruling 09 13, form i290 |