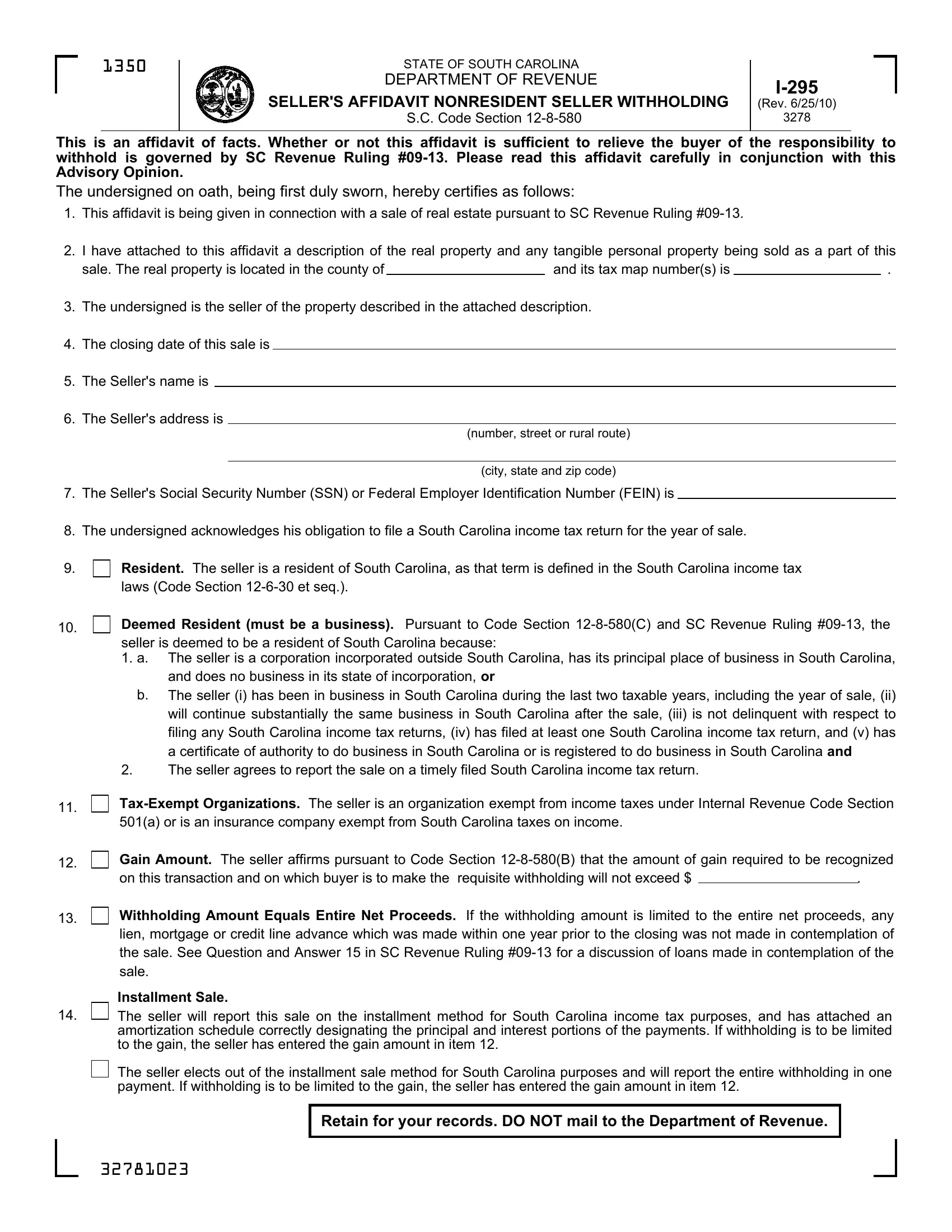

Navigating the tax implications and legal requirements involved in the sale of real estate by nonresidents in South Carolina involves understanding various statutory provisions, among which the form I-295 plays a crucial role. Specifically designed for nonresident sellers, this form is a seller’s affidavit under the South Carolina Code Section 12-8-580, created to ensure compliance with state tax withholding requirements on real estate transactions. It encompasses declarations by the seller regarding their residency status, a description of the property being sold, the seller's obligation to file a South Carolina income tax return, and other pertinent details reflecting the complexity of tax law and its implications on real estate transactions. Importantly, the form serves to potentially relieve the buyer from the responsibility of withholding part of the sale proceeds for tax purposes, contingent upon accurately meeting conditions as outlined in SC Revenue Ruling #09-13. This ruling, along with the advisories provided, forms the backbone of understanding how withholding requirements can be navigated or nullified under specific circumstances, such as sales involving tax-exempt organizations, installment sales, principal residence sales, involuntary conversions, like-kind exchanges, and employee relocation scenarios. Notably, this document must be read and understood in conjunction with the applicable Advisory Opinion, emphasizing its role as not just a form but as a critical affidavit bearing legal weight in real estate transactions within South Carolina.

| Question | Answer |

|---|---|

| Form Name | Form I 295 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | I295 form i 295 |