The IDR 54-269 form, an essential document for nonprofit and charitable organizations seeking property tax exemptions in Iowa, encapsulates the legal framework laid out in Iowa Code Section 427.1(14). Required to be filed or mailed to the city or county assessor by February 1, with a postmark no later than this date, it facilitates the exemption process, ensuring organizations that qualify can benefit from tax relief. This form gathers comprehensive details about the applicant, including contact information, property title and use, as well as any income-generating activities on the property that could impact its eligibility for exemption. It meticulously assesses if the property is being used in alignment with the organization's non-profit goals and if any part of it serves commercial purposes. Additionally, it clarifies the legal stance on properties with federally-licensed devices not permitted under Iowa law, establishing clear grounds for exemption denial. This form also forms a basis for possible revocation of exemptions if violations occur, underlining the importance of adherence to state laws and regulations for maintaining tax-exempt status. By providing a structured format for application, the IDR 54-269 form plays a pivotal role in ensuring that exemptions are granted to eligible entities in a fair and transparent manner, emphasizing the state's support for non-profit and charitable endeavors.

| Question | Answer |

|---|---|

| Form Name | Form Idr 54 269 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | Dist, taxable, valuation, 54-269b |

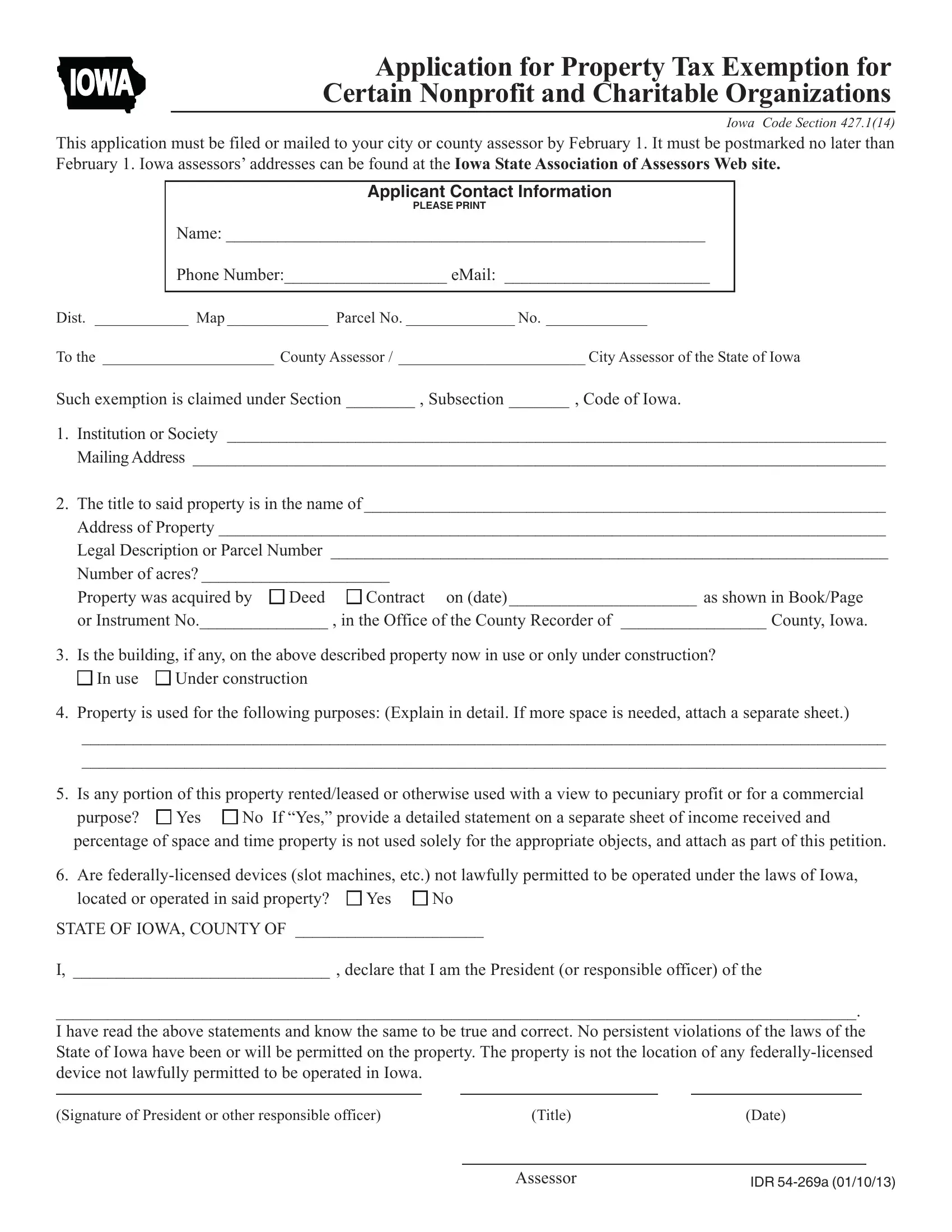

IOWA

Application for Property Tax Exemption for Certain Nonprofit and Charitable Organizations

IOWA CODE SECTION 427.1(14)

This application must be filed or mailed to your city or county assessor by February 1. It must be postmarked no later than February 1. Iowa assessors’ addresses can be found at the Iowa State Association of Assessors Web site.

Applicant Contact Information

PLEASE PRINT

Name: ________________________________________________________

Phone Number:___________________ eMail: ________________________

Dist. ____________ Map _____________ Parcel No. ______________ No. _____________

To the ______________________ County Assessor / ________________________ City Assessor of the State of Iowa

Such exemption is claimed under Section ________ , Subsection _______ , Code of Iowa.

1.Institution or Society _____________________________________________________________________________

Mailing Address _________________________________________________________________________________

2.The title to said property is in the name of_____________________________________________________________

Address of Property ______________________________________________________________________________

Legal Description or Parcel Number __________________________________________________________________

Number of acres? ______________________

Property was acquired by |

Deed |

Contract on (date)______________________ as shown in Book/Page |

or Instrument No._______________ , in the Office of the County Recorder of _________________ County, Iowa.

3. Is the building, if any, on the above described property now in use or only under construction?

In use |

Under construction |

4.Property is used for the following purposes: (Explain in detail. If more space is needed, attach a separate sheet.)

______________________________________________________________________________________________

______________________________________________________________________________________________

5.Is any portion of this property rented/leased or otherwise used with a view to pecuniary profit or for a commercial

purpose? |

Yes |

No If “Yes,” provide a detailed statement on a separate sheet of income received and |

percentage of space and time property is not used solely for the appropriate objects, and attach as part of this petition.

6. Are

located or operated in said property? |

Yes |

No |

STATE OF IOWA, COUNTY OF ______________________ |

||

I, ______________________________ , declare that I am the President (or responsible officer) of the

_____________________________________________________________________________________________.

I have read the above statements and know the same to be true and correct. No persistent violations of the laws of the State of Iowa have been or will be permitted on the property. The property is not the location of any

(Signature of President or other responsible officer) |

(Title) |

(Date) |

Assessor |

IDR |

LAW AND INSTRUCTIONS

427.1. EXEMPTIONS. The following classes of property shall not be taxed.

5.Property of associations of war veterans. The property of any organization composed wholly of veterans of any war, when such property is devoted entirely to its own use and not held for pecuniary profit.

8.Property of religious, literary, and charitable societies. All grounds and buildings used or under construction by literary, scientific, charitable, benevolent, agricultural, and religious institutions and societies solely for their appropriate objects, not exceeding three hundred twenty acres in extent and not leased or otherwise used or under construction with a view to pecuniary profit. An organization whose primary objective is to preserve land in its natural state may own or lease land not exceeding three hundred twenty acres in each county for its appropriate objects. All deeds or leases by which such property is held shall be filed for record before the property herein described shall be omitted from the assessment. All such property shall be listed upon the tax rolls of the district or districts in which it is located and shall have ascribed to it an actual fair market value and an assessed or taxable value, as contemplated by section 441.21 of the Code, whether such property be subject to a levy or be exempted as herein provided and such information shall be open to public inspection.

14.Statement of Objects and Uses Filed. A society and organization claiming an exemption under the provisions of either subsection five (5) subsection eight (8) or subsection thirty three (33) of this section shall file with the assessor not later than February 1 of the year for which such exemption is requested, a statement upon forms to be prescribed by director of revenue, describing the nature of the property upon which such exemption is claimed and setting out in detail any uses and income from the property derived from the rentals, leases or other uses of the property not solely for the appropriate objects of the society or organization. The assessor, in arriving at the valuation of any property of the society or organization shall take into consideration any uses of the property not for the appropriate objects of the organization and shall assess in the same manner as other property, all or any portion of the property involved which is leased or rented and is used regularly for commercial purposes for a profit to a party or individual. If a portion of the property is used regularly for commercial purposes, an exemption shall not be allowed upon property so used and the exemption granted shall be in the proportion of the value of the property used solely for the appropriate objects of the organization, to the entire value of the property. An exemption shall not be granted upon property upon or in which persistent violations of law be knowingly permitted or have been permitted on or after January 1st of the year for which a tax exemption is requested. Claims for such exemption shall be verified under oath by the president or other responsible head of the organization.

15.Mandatory Denial. No exemption shall be granted upon any property which is the location of federally licensed devices not lawfully permitted to operate under the laws of the state of Iowa.

16.Revoking Exemption. Any taxpayer or any taxing district may make application to the director of revenue for revocation or modification for any exemption, based upon alleged violations of this chapter. The director of revenue may also on the director’s own motion, set aside or modify any exemption which has been granted upon property for which exemption is claimed under this chapter. The director of revenue shall give notice by mail to the taxpayer or taxing district applicant and to the societies or organizations claiming an exemption upon property, exemption of which is questioned before or by the director of revenue and shall hold a hearing prior to issuing any order for revocation or modification. An order made by the director of revenue revoking or modifying an exemption shall be applicable to the tax year commencing with the tax year in which the application is made to the director or the tax year commencing with the tax year in which the director’s own motion is filed. An order made by the director of revenue revoking or modifying an exemption is subject to judicial review in accordance with Chapter 17A, the Iowa administrative procedure act. Notwithstanding the terms of that Act, petitions for judicial review may be filed in the district court having jurisdiction in the county in which the property is located, and must be filed within thirty days after any order revoking or modifying an exemption is made by the director of revenue.

21.

33.Property owned and operated by an Indian housing authority, as defined in 24 C.F.R. 950.102, created under Indian law, if a cooperative agreement has been made with the local governing body agreeing to the exemption.

INSTRUCTIONS:

1.List description of one location only (with any adjoining properties). If exemption is to be claimed on properties in more than one location, use a separate application form for each such description.

2.Complete this form and return to the assessor on or before February 1. The assessor may request additional information to determine the taxable status of the property.

3.IMPORTANT: THIS CLAIM MUST BE FILED ON OR BEFORE THE DATE SPECIFIED BY LAW, OR EXEMPTION CANNOT BE GRANTED.

IDR