Understanding the NAC 372.730 form, as prescribed by the Nevada Department of Taxation, is crucial for businesses involved in the resale of tangible personal property within the state. This form serves as a vital tool in maintaining compliance with the resale certificate regulations outlined in the Nevada Revised Statutes, specifically chapters 372, 374, and 377. By completing this certificate, businesses affirm that they possess a valid seller's permit, engage in selling specific tangible personal properties, and intend to resell the purchased goods. The form allows for the declaration of the nature of the items being purchased, whether through an itemized list or a general description, aiming to streamline the resale process while ensuring adherence to tax laws. Additionally, it addresses various scenarios, such as exemptions for sellers not required to hold a permit and the acceptance of blanket certificates for recurring transactions, simplifying the administrative burden on businesses. Critical to this process is the requirement for businesses to retain these certificates on file and the emphasis on the seller's responsibility to assess the purchaser's intent to resell, underscoring the importance of due diligence in commercial operations. The NAC 372.730 form embodies a comprehensive approach to facilitating lawful business practices and tax compliance in Nevada's market.

| Question | Answer |

|---|---|

| Form Name | Form Nac 372 730 |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | nv form resale, nevada fstf search, resale certificate nevada form, nevada resale certificate blank form |

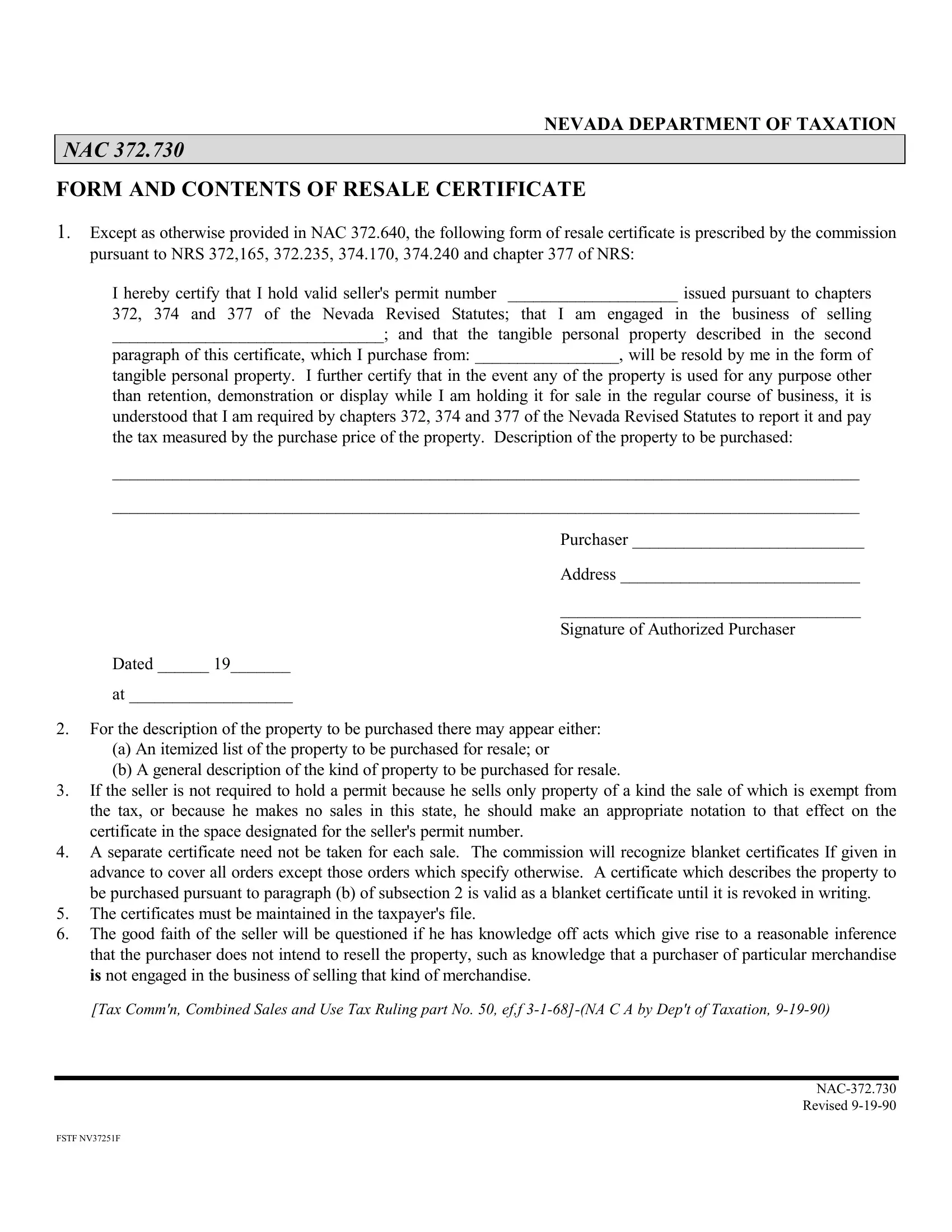

NEVADA DEPARTMENT OF TAXATION

NAC 372.730

FORM AND CONTENTS OF RESALE CERTIFICATE

1. Except as otherwise provided in NAC 372.640, the following form of resale certificate is prescribed by the commission pursuant to NRS 372,165, 372.235, 374.170, 374.240 and chapter 377 of NRS:

I hereby certify that I hold valid seller's permit number ____________________ issued pursuant to chapters

372, 374 and 377 of the Nevada Revised Statutes; that I am engaged in the business of selling

________________________________; and that the tangible personal property described in the second

paragraph of this certificate, which I purchase from: _________________, will be resold by me in the form of

tangible personal property. I further certify that in the event any of the property is used for any purpose other than retention, demonstration or display while I am holding it for sale in the regular course of business, it is understood that I am required by chapters 372, 374 and 377 of the Nevada Revised Statutes to report it and pay the tax measured by the purchase price of the property. Description of the property to be purchased:

_______________________________________________________________________________________

_______________________________________________________________________________________

Purchaser ___________________________

Address ____________________________

___________________________________

Signature of Authorized Purchaser

Dated ______ 19_______

at ___________________

2.For the description of the property to be purchased there may appear either:

(a)An itemized list of the property to be purchased for resale; or

(b)A general description of the kind of property to be purchased for resale.

3.If the seller is not required to hold a permit because he sells only property of a kind the sale of which is exempt from the tax, or because he makes no sales in this state, he should make an appropriate notation to that effect on the certificate in the space designated for the seller's permit number.

4.A separate certificate need not be taken for each sale. The commission will recognize blanket certificates If given in advance to cover all orders except those orders which specify otherwise. A certificate which describes the property to be purchased pursuant to paragraph (b) of subsection 2 is valid as a blanket certificate until it is revoked in writing.

5.The certificates must be maintained in the taxpayer's file.

6.The good faith of the seller will be questioned if he has knowledge off acts which give rise to a reasonable inference that the purchaser does not intend to resell the property, such as knowledge that a purchaser of particular merchandise IS not engaged in the business of selling that kind of merchandise.

[Tax Comm'n, Combined Sales and Use Tax Ruling part No. 50, ef,f

Revised

FSTF NV37251F