Managing changes to employment status and planning for financial futures are critical concerns for individuals participating in deferred compensation plans. The NC 457b form plays a pivotal role in this process, offering a structured approach for reporting terminations and requesting disbursements from the NC 457b Deferred Compensation Plan. This form, which must be completed with utmost attention to detail using blue or black ink, requires authorization by the employer, underscoring the importance of a coordinated effort between the employee and their benefits or human resources office. Upon thoroughly reviewing the employee's submitted information, the authorized employer representative's signature ensures the request's validity, preventing processing without this crucial approval. The form outlines various disbursement options, including direct rollovers to other qualified plans and partial or total lump sum withdrawals, each with specific tax implications and considerations for the requesting individual. Additionally, it highlights the mandatory and optional aspects of federal and state income tax withholding, making it essential for individuals to understand their responsibilities and options regarding tax liabilities. With options for electronic fund transfers and detailed instructions for addressing overpayments, the form emphasizes accuracy and clarity in managing one’s deferred compensation benefits. This comprehensive approach facilitates a smoother transition for employees experiencing changes in their employment status, while also safeguarding their financial interests and compliance with regulatory requirements.

| Question | Answer |

|---|---|

| Form Name | Form Nc 457B |

| Form Length | 7 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 45 sec |

| Other names | North_Carolina, prudential forms request for termination request for disbursement, rollovers, prudential |

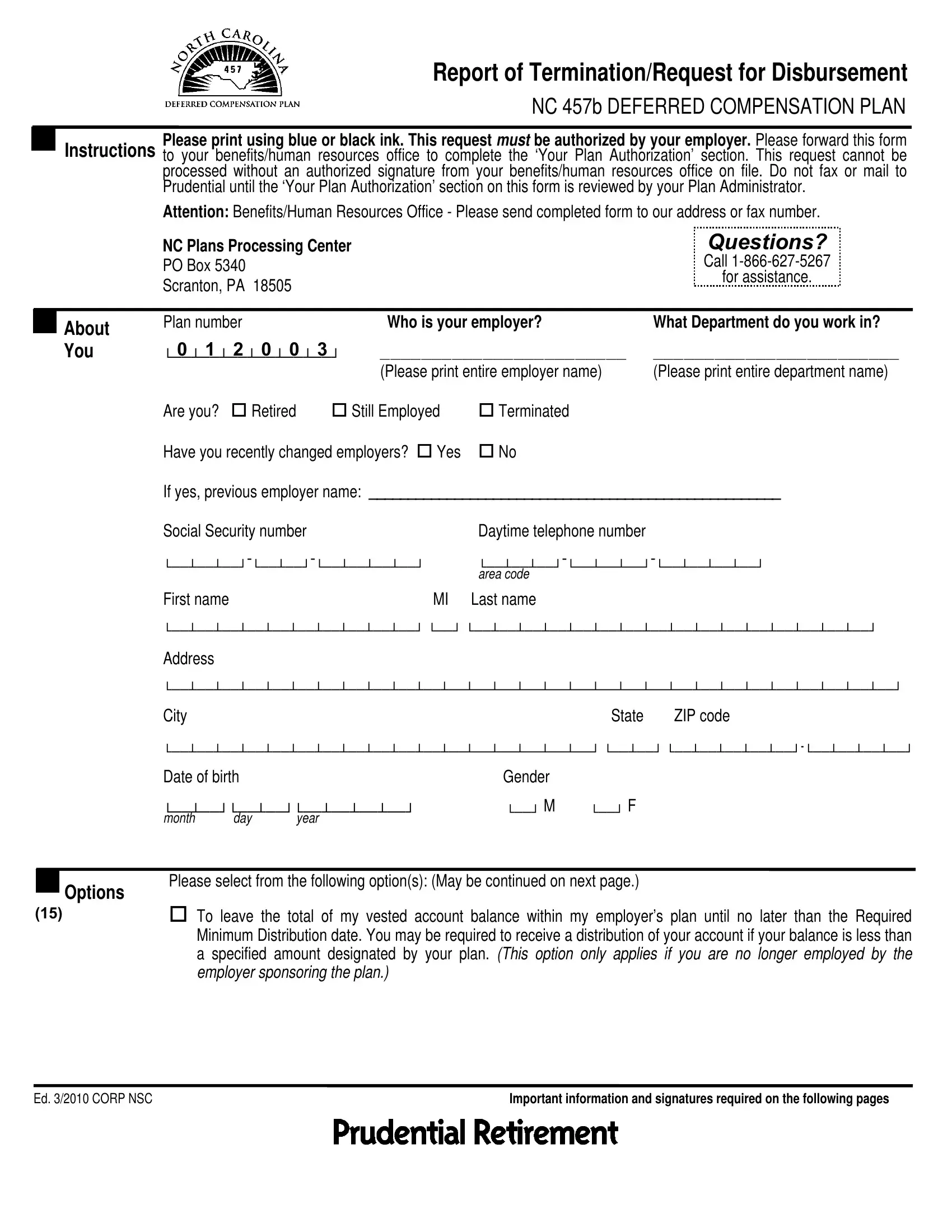

Report of Termination/Request for Disbursement

NC 457b DEFERRED COMPENSATION PLAN

Please print using blue or black ink. This request must be authorized by your employer. Please forward this form Instructions to your benefits/human resources office to complete the ‘Your Plan Authorization’ section. This request cannot be processed without an authorized signature from your benefits/human resources office on file. Do not fax or mail to

Prudential until the ‘Your Plan Authorization’ section on this form is reviewed by your Plan Administrator. Attention: Benefits/Human Resources Office - Please send completed form to our address or fax number.

|

NC Plans Processing Center |

|

|

|

QUESTIONS? |

|

|

PO Box 5340 |

|

|

|

|

Call |

|

|

|

|

|

for assistance. |

|

|

Scranton, PA 18505 |

|

|

|

||

|

|

|

|

|

||

About |

Plan number |

|

Who is your employer? |

|

What Department do you work in? |

|

|

|

|

|

|

|

|

You |

0 1 2 |

0 0 3 |

________________________ |

________________________ |

||

|

└──┴──┴──┴──┴──┴──┘ |

(Please print entire employer name) |

(Please print entire department name) |

|||

|

|

|

||||

|

Are you? |

Retired |

Still Employed |

Terminated |

|

|

|

Have you recently changed employers? Yes |

No |

|

|

||

|

If yes, previous employer name: _____________________________________________________ |

|||||

|

Social Security number |

|

Daytime telephone number |

|

||

|

area└──┴──┴──┘code |

|||||

|

First name |

|

MI |

Last name |

|

|

└──┴──┴──┴──┴──┴──┴──┴──┴──┴──┘ └──┘ └──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┘

Address

└──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┘

City |

State |

ZIP code |

└──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┘ └──┴──┘

Date of birth |

|

Gender |

|

|

||

└──┴──┘└──┴──┘└──┴──┴──┴──┘ |

└──┘ |

M |

└──┘ |

F |

||

month |

day |

year |

|

|

|

|

Options

(15)

Please select from the following option(s): (May be continued on next page.)

To leave the total of my vested account balance within my employer’s plan until no later than the Required Minimum Distribution date. You may be required to receive a distribution of your account if your balance is less than a specified amount designated by your plan. (This option only applies if you are no longer employed by the employer sponsoring the plan.)

Ed. 3/2010 CORP NSC |

Important information and signatures required on the following pages |

Options

(73)(continued)

(20)

Direct

1. Types of |

2. What do you want to roll |

3. What type of |

4. Please choose a specific |

|

money in your |

over? |

account are you |

product/plan below. |

|

account. |

|

rolling to? |

|

|

The entire Account. |

Another |

Direct Rollover to your NC 401(k) |

||

and |

|

qualified |

Account |

|

|

employer- |

|||

Account. |

A portion of the Account: |

|

||

based plan. |

Prudential SmartSolution IRA2 |

|||

(Excludes Roth |

||||

|

|

Brokerage IRA with Prudential |

||

Accounts. May |

$_____________ |

A Traditional |

||

include one or |

Investment Management |

|||

|

IRA. |

|||

|

Bank IRA with Prudential Bank and |

|||

more of the |

OR |

|||

|

||||

following: Your |

|

1 |

Trust2 |

|

_____________% |

A Roth IRA. |

|

||

own |

|

Other3 |

||

|

|

|||

contributions |

Percentage of |

|

Name____________________________ |

|

|

||||

contributions (if any) to be |

|

|||

tax, or both), |

|

|

||

rolled |

|

Payee name______________________ |

||

made by your |

|

|

||

|

|

|

||

employer, |

_____________% |

|

Address__________________________ |

|

money you’ve |

|

|||

(If no percentage is |

|

|

||

rolled over from |

|

_________________________________ |

||

indicated, |

|

|||

another |

|

|||

contributions will be |

|

Account number: |

||

|

||||

included in the direct |

|

|||

|

____________________ |

|||

plan.) |

|

|||

rollover. It is your |

|

|||

|

responsibility to confirm that |

|

|

|

|

the receiving plan accepts |

|

|

|

|

rollovers, including |

|

|

|

|

if applicable.) |

|

|

1This type of rollover is subject to current taxes. Please complete the section called “Election for Withholding Federal Income Taxes When Rolling

2Your SmartSolution IRA or Prudential Bank and Trust IRA must be opened before the distribution can be processed. If you have not already opened an account please call our

3If the address of the institution is not given, your direct rollover check will be sent to you. You are responsible for completing the direct rollover to your financial institution in a timely manner in accordance with applicable law. If rolling over to multiple institutions, please list additional institutions or IRA (note if Traditional or Roth) on a separate page.

Partial Single

Depending on the terms of your plan, the funds will either be prorated across all available contribution types and

investments or taken in a specific sequence. If you select this option and no amount is specified here or if you would like to choose the contribution type for your disbursement, you must check the appropriate box(es) below:

Please note: The minimum allowable disbursement is $500 unless a total disbursement is taken.

1.Amount indicated or maximum amount of my

2.Amount indicated or maximum amount of my

Important information and signatures required on the following pages

Options

(20)(continued)

Total Single

•To request distributions in installment payments, a Request for Systematic Disbursement form should be completed in place of this form. You can request the form by calling our

If no distribution election is made and your account balance is less than $500, we will automatically process a lump sum distribution.

• Annuity Please call our service center toll free at

Express Mail

(check box if applicable)

Electronic

Fund

Transfer

(not applicable for direct rollover)

•Income for a Period Certain

•Fixed Life Annuity with Guaranteed Period of 5, 10, 15, 20 years

•Fixed Life Annuity Life only (no death benefits)

•Joint Life 50% Survivor Benefit or 100% Survivor Benefit option for guaranteed period of 5, 10, 15, 20 years

Send my disbursement check by express mail and deduct $10.50 per check from my account prior to the distribution. Please Note: Express mail is not available for annuities or systematic disbursements, or delivery to post office boxes.

If you would like your disbursement sent to you via Electronic Funds Transfer (EFT), please check the following box and complete the information below. If all of the necessary information is not provided or if this section does not apply to your disbursement request, a check will be made payable to you.

I would like my payment sent by EFT.

Financial Institution name

└──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┘

Account number

└──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┴──┘

Please verify the entire account number with your financial institution to ensure acceptance of payments.

Type of Account: |

Checking |

Savings |

Financial Institution Routing/Transit/ABA Number

└──┴──┴──┴──┴──┴──┴──┴──┴──┘

Attach a voided check or obtain this number from your financial institution.

I have carefully read this form and I hereby authorize Prudential to make this Plan payment to the financial institution listed above in the form of direct deposit.

I understand payment will be made to the financial institution account listed above by Electronic Fund Transfer (EFT).

In the event that an overpayment is credited to the financial institution account listed above, I hereby authorize and direct the financial institution designated above to debit my account and refund any overpayment to Prudential. This authorization will remain in effect until Prudential receives a written notice from me stating otherwise and until Prudential has had a reasonable chance to act upon it.

Important information and signatures required on the following pages

Election for Withholding Federal Income Taxes When Rolling Non- Roth Money to a Roth IRA

Only complete this section if you elected to roll

A rollover of

Please withhold |

|

% (percent) or $ |

(amount) |

|

|

|

|

|

|

Please do not withhold federal income taxes

(Note: If you elect federal income tax withholding for this type of rollover, you will receive a second

Election for Withholding of Federal Income Taxes

(For Single Sum Payments)

Election For

Withholding

of State

Income Taxes

(For Single Sum Payments and Rollovers of non- Roth money to a Roth IRA)

NC State Income Tax withholding generally does not apply to payees of a Bailey vested account.

We will automatically withhold 20% federal income tax from the taxable portion of your distribution. Only complete this section if you elected a total or partial single sum distribution made payable to you and you wish to have an additional amount withheld from your distribution.

In addition to the 20%, I want └──┴──┴──┘% or $└──┴──┴──┘,└──┴──┴──┘. federal income tax withheld from my distribution.

A.Mandatory State Withholding: If you reside in a state where state income tax withholding is mandatory AR,

CA*, DE, IA, KS, MA, MD (mandatory for eligible rollover distributions only, subject to 20% mandatory federal withholding), ME, NC, NE, OK*, OR*, VA or VT* applicable withholding will be deducted automatically, unless an election out is applicable (see below). Note: Some states require withholding if federal income tax is withheld from the distribution.

My resident state is AR, DE, KS, ME, NC, NE, or VA (for NE and VA, election out is allowed for payments from IRA’s only) and I do not want state income tax withholding deducted from my distribution. (An election out of AR, DE, KS, ME, NC, or VA state tax is not allowed for eligible rollover distributions, subject to 20% mandatory federal withholding.) Important note to Maine (ME) residents. If you elect out of ME withholding, you must either have elected out of federal withholding, or have no Maine State tax liability in the prior or current years.

*My resident state is one of the following: CA, OK, OR, **VT and withholding is required if federal income tax is withheld, unless I elect out of state withholding. By checking this box I am electing out of state withholding. **An election out is not allowed for eligible rollover distributions, subject to 20% mandatory federal withholding.

B.Voluntary State Withholding: Please check the appropriate box below. If state income tax withholding is not mandatory in your state, you may be allowed to request state tax withholding. If your state of residence is not listed, or if you choose a method of withholding that is not offered for your state, we cannot withhold state income tax.

I reside in one of the following voluntary withholding states: AL, CO, CT, DC, GA, ID, IL, IN, KY, LA, MD

______________% or $___________________

I reside in one of the voluntary withholding states listed above and I do not want state income tax withholding deducted from my distribution.

C.No State Withholding: Some states do not have state income tax withholding.

My resident state is one of the following: AK, FL, HI, NV, NH, SD, TN, TX, WA, WY and there is no state income tax withholding.

My resident state is AZ and there is no state income tax withholding on

Important information and signatures required on the following page

YourI understand that Prudential will rely on the information I have provided in processing my request. I further understand Authorization that I am responsible for its accuracy in the event any dispute arises with respect to the transaction. I acknowledge that I have read the attached Special Tax Notice Regarding Plan Payments. I understand the tax implications regarding

this disbursement, including that if I am entitled to an eligible rollover distribution, I have the right to consider whether or not to elect a direct rollover for at least 30 days after this special tax notice is provided. By signing this form, I am waiving this notice period. The taxable portion of any distribution that is eligible for "rollover" is subject to a mandatory 20% federal income tax withholding, unless that amount is directly rolled to an Individual Retirement Account (IRA) or to another plan in which I am a participant.

If there are investment options available through your retirement account that are subject to the fund’s market timing policies, you may be subject to restrictions or incur fees if you engage in excessive trading activity in those investments. You may wish to review the fund information or your retirement account’s market timing policy prior to submitting this transaction request. If a fee applies to the transaction, you will be able to view the details after the transaction is processed by logging on to the retirement internet site at www.prudential.com/online/retirement.

|

X |

Date |

|

|

|

|

|

Participant’s signature |

|

|

|

|

|

Your |

This section must be completed by an authorized employer representative. If an authorized plan representative |

|||||

Plan |

previously submitted termination information to Prudential and a change in employee status did not take place |

|||||

Authorization since then, this section does not need to be completed.

I certify, as plan sponsor and authorized representative of the plan, I understand that it is my responsibility to confirm employee status (i.e., terminated, rehired) and date of termination for terminated participants, and submit such information to Prudential. If the participant is terminated, I authorized Prudential to process any current or future disbursements to the participant named on the attached using the date of termination provided. I understand that it is my responsibility to notify Prudential of any change in employee status (i.e., if a participant is rehired). After signature is received by Prudential, any future disbursements of terminated participants will not require approval unless a change in employee status applies.

Date of Separation from Service: └──┴──┘└──┴──┘└──┴──┴──┴──┘

month |

day |

year |

Please indicate type of separation: |

Termination |

Retirement |

X |

|

Date |

Authorized employer representative’s signature

Print name and title

Prudential fax number:

Applies to Section 457(b) Governmental Plans Only

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

Retain For Your Records

This notice is provided to you by Prudential Financial, Inc., on behalf of the North Carolina Public Employee Deferred Compensation (“The Plan”).

Right to Defer Distributions from Defined Contribution Plans

You may be eligible to receive a distribution from your employer's retirement plan now. Instead of taking a distribution now, you may elect to defer receiving a distribution until a later date

YOUR ROLLOVER OPTIONS

This notice is provided to you because all or part of the payments you may receive from the employer’s plan (the “Plan”) may be eligible for rollover to an IRA or an eligible employer plan. This notice is intended to help you decide whether to do such a rollover. If you have additional questions after reading this notice, you can contact your Plan Administrator.

Rules that apply to most payments from a plan are described in the “General Information About Rollovers” section. Special rules that only apply in certain circumstances are described in the “Special Rules and Options” section.

GENERAL INFORMATION ABOUT ROLLOVERS

How can a rollover affect my taxes?

You will be taxed on a payment from the Plan if you do not roll it over. In addition, distributions from this Plan are generally not subject to the 10% additional income tax that applies to

Where may I roll over the payment?

You may roll over the payment to either an IRA (an individual retirement account or individual retirement annuity) or an employer plan (a

How do I do a rollover?

There are two ways to do a rollover. You can do either a direct rollover or a

If you do a direct rollover, the Plan will make the payment directly to your IRA or an employer plan. You should contact the IRA sponsor or the administrator of the employer plan for information on how to do a direct rollover.

If you do not do a direct rollover, you may still do a rollover by making a deposit into an IRA or eligible employer plan that will accept it. You will have 60 days after you receive the payment to make the deposit. If you do not do a direct rollover, the Plan is required to withhold 20% of the payment for federal income taxes. This means that, in order to roll over the entire payment in a

How much may I roll over?

If you wish to do a rollover, you may roll over all or part of the amount eligible for rollover. Any payment from the Plan is eligible for rollover, except:

•Certain payments spread over a period of at least 10 years or over your life or life expectancy (or the lives or joint life expectancy of you and your beneficiary)

Ed. 12/2009

•Required minimum distributions after age 70½ (or after death)

•Unforeseeable emergency distributions

•Corrective distributions of contributions that exceed tax law limitations

•Loans treated as deemed distributions (for example, loans in default due to missed payments before your employment ends)

•Contributions made under special automatic enrollment rules that are withdrawn pursuant to your request within 90 days of enrollment

The Plan or the payor can tell you what portion of a payment is eligible for rollover.

If I do a rollover to an IRA, will the 10% additional income tax apply to early distributions from the IRA?

If you receive a payment from an IRA when you are under age 59½, you will have to pay the 10% additional income tax on early distributions from the IRA, unless an exception applies.

What are the exceptions to the 10% additional income tax that applies to early distributions?

In general, the exceptions to the 10% additional income tax for early distributions from an IRA are the same as the exceptions applicable to Section 401 and 403 employer plans for early distributions from a plan, which are as follows:

•Payments made after you separate from service if you will be at least age 55 in the year of the separation

•Payments that start after you separate from service if paid at least annually in equal or close to equal amounts over your life or life expectancy (or the lives or joint life expectancy of you and your beneficiary)

•Payments made due to disability

•Payments after your death

•Payments of ESOP dividends

•Corrective distributions of contributions that exceed tax law limitations

•Cost of life insurance paid by the Plan

•Contributions made under special automatic enrollment rules that are withdrawn pursuant to your request within 90 days of enrollment

•Payments made directly to the government to satisfy a federal tax levy

•Payments made under a qualified domestic relations order (QDRO)

•Payments up to the amount of your deductible medical expenses

•Certain payments made while you are on active duty if you were a member of a reserve component called to duty after September 11, 2001 for more than 179 days

However, there are a few differences for payments from an IRA, including:

•There is no exception for payments after separation from service that are made after age 55.

•The exception for qualified domestic relations orders (QDROs) does not apply (although a special rule applies under which, as part of a divorce or separation agreement, a

•The exception for payments made at least annually in equal or close to equal amounts over a specified period applies without regard to whether you have had a separation from service.

•There are additional exceptions for (1) payments for qualified higher education expenses, (2) payments up to $10,000 used in a qualified

Will I owe State income taxes?

This notice does not describe any State or local income tax rules (including withholding rules).

SPECIAL RULES AND OPTIONS

If you miss the

Generally, the

If you have an outstanding loan that is being offset

If you have an outstanding loan from the Plan, your Plan benefit may be offset by the amount of the loan, typically when your employment ends. The loan offset amount is treated as a distribution to you at the time of the offset and will be taxed unless you do a

If you are an eligible retired public safety officer and your pension payment is used to pay for health coverage or qualified

If you retired as a public safety officer, and your retirement was by reason of disability or was after normal retirement age, you can exclude from your taxable income plan payments paid directly as premiums to an accident or health plan (or a qualified

If you roll over your payment to a Roth IRA

You can roll over a payment from the Plan made before January 1, 2010 to a Roth IRA only if your modified adjusted gross income is not more than $100,000 for