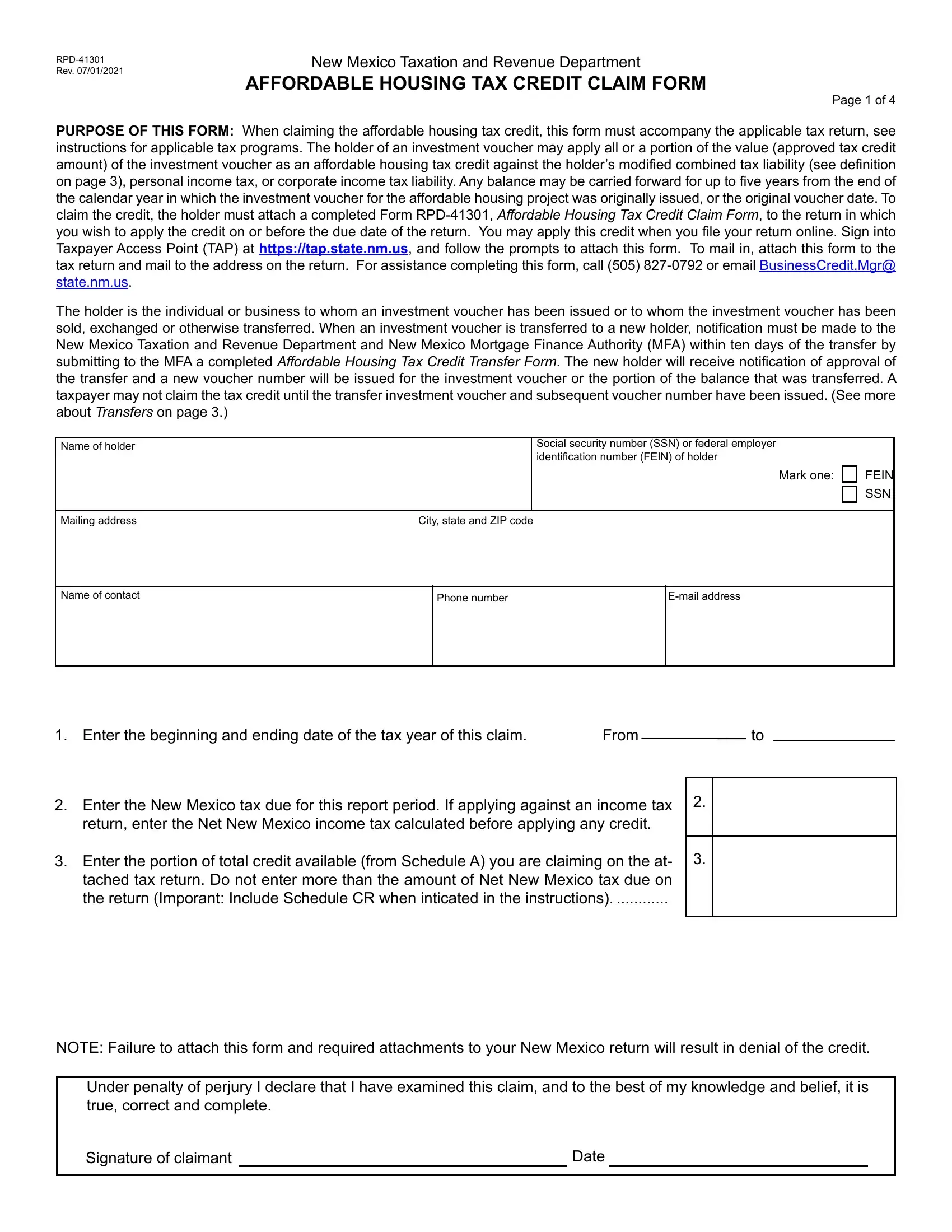

In the landscape of tax incentives designed to bolster affordable housing development, the RPD-41301 form emerges as a pivotal document for entities navigating the financial nuances of these projects in New Mexico. Issued by the New Mexico Taxation and Revenue Department, the Affordable Housing Tax Credit Claim Form serves as the bridge between investment in affordable housing and the realization of a tax credit benefit against a modified combined tax liability, personal income tax, or corporate income tax liabilities. Notably, this form accommodates the claiming of credits derived from investments in land, buildings, construction, and other components integral to affordable housing projects that have received the green light from the New Mexico Mortgage Finance Authority. What sets this form apart is its capacity to embody transfers, allowing credits to be assigned, thus introducing flexibility and liquidity into the realm of affordable housing finance. The stipulation of a five-year carryforward period for unused credits post the original issuance date underscores a commitment to long-term investment in the housing sector. Furthermore, the form's meticulous design, evident in the required attachment of supporting schedules and adherence to specific deadlines, ensures that claimants are both informed and compliant in their quest to contribute to affordable housing while navigating their tax obligations responsibly.

| Question | Answer |

|---|---|

| Form Name | Form Rpd 41301 |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | this form must accompany the applicable tax return, PURPOSE OF THIS FORM: When claiming the affordable housing tax credit, see |