Through the online tool for PDF editing by FormsPal, you are able to fill out or edit Form Rtf 1Ee right here. FormsPal expert team is ceaselessly working to enhance the tool and help it become even faster for people with its many features. Unlock an constantly progressive experience now - take a look at and find out new opportunities along the way! All it requires is just a few simple steps:

Step 1: First, access the tool by pressing the "Get Form Button" in the top section of this site.

Step 2: The editor gives you the opportunity to change nearly all PDF documents in a variety of ways. Enhance it by including personalized text, correct existing content, and include a signature - all readily available!

This PDF doc will require some specific information; to ensure correctness, take the time to consider the tips below:

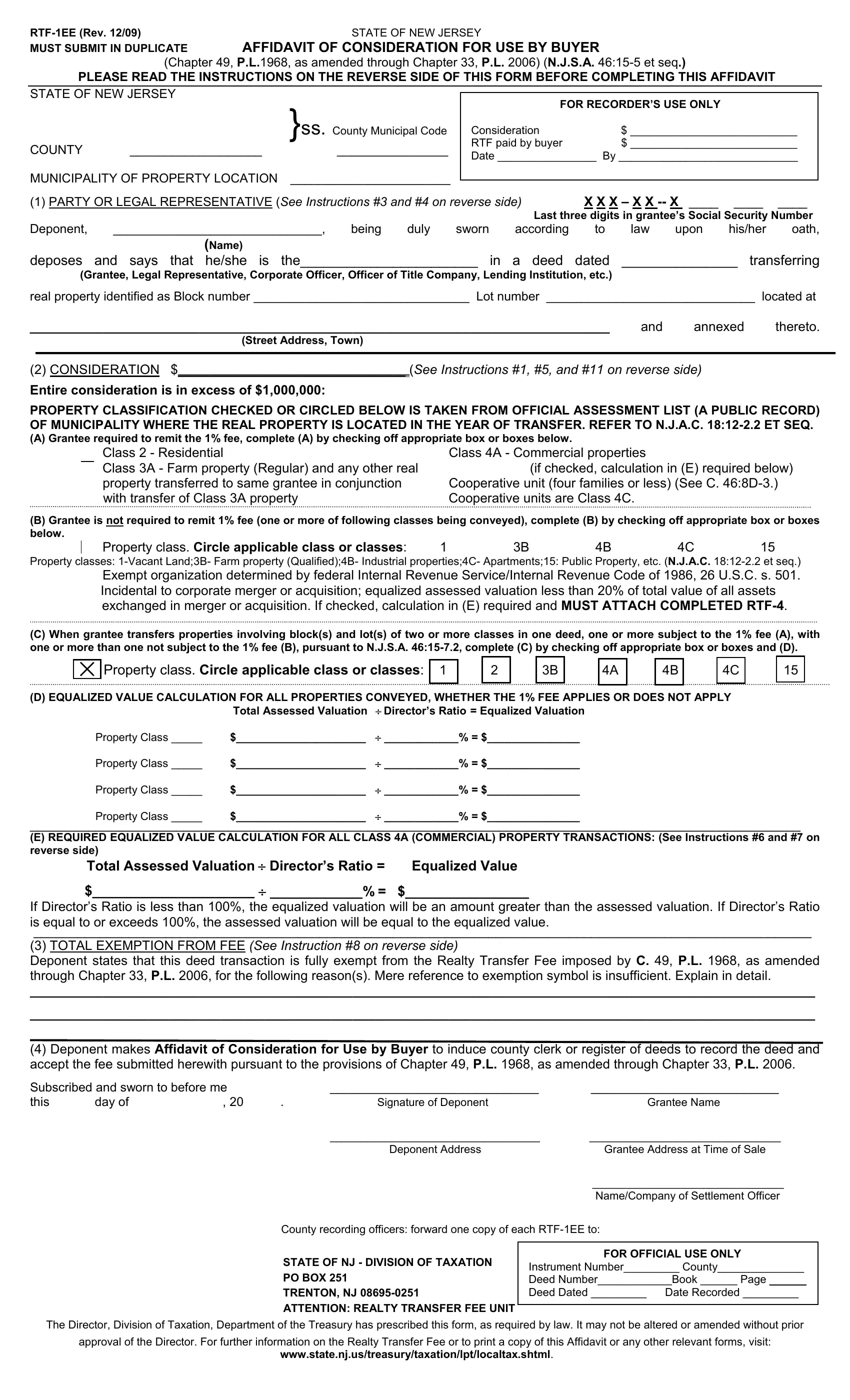

1. Complete the Form Rtf 1Ee with a selection of necessary fields. Get all the required information and make certain nothing is left out!

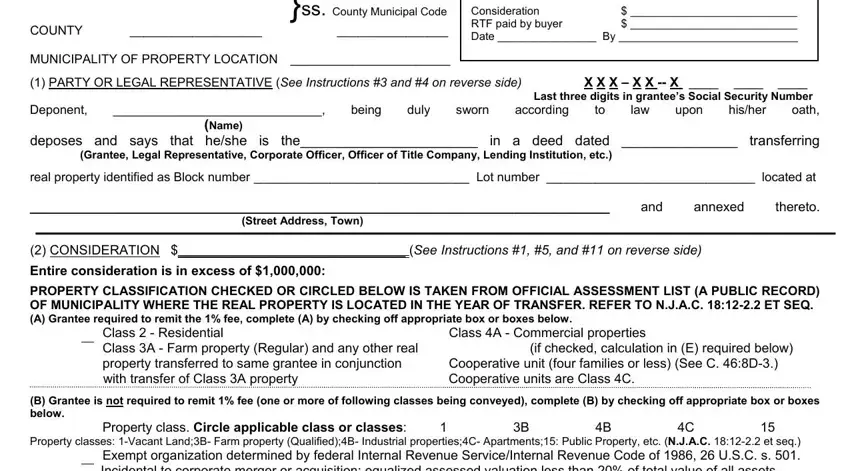

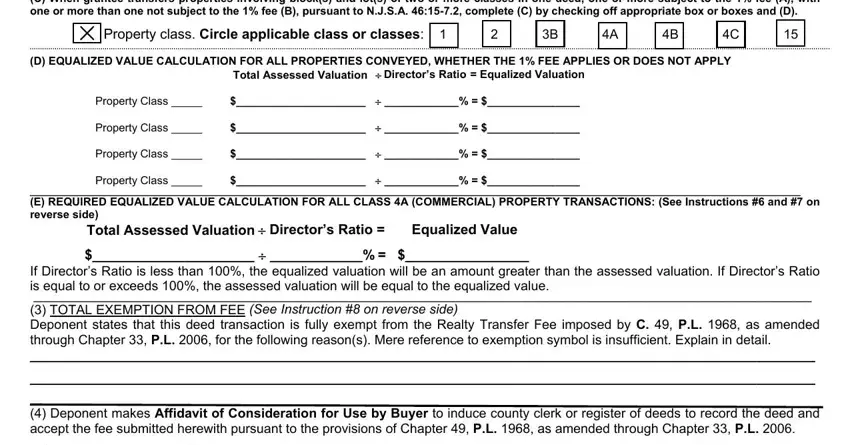

2. Given that the last section is complete, you should add the necessary particulars in C When grantee transfers, Property class Circle applicable, D EQUALIZED VALUE CALCULATION FOR, Property Class Property Class, Total Assessed Valuation, E REQUIRED EQUALIZED VALUE, and Deponent makes Affidavit of allowing you to proceed to the third part.

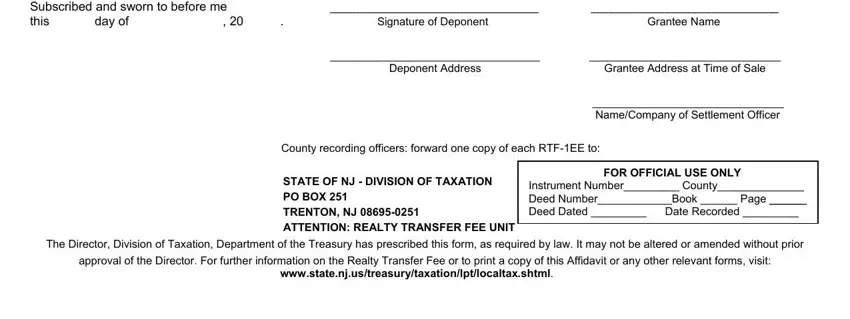

3. Within this stage, look at Deponent makes Affidavit of, Signature of Deponent, Grantee Name, Grantee Address at Time of Sale, Deponent Address, NameCompany of Settlement Officer, County recording officers forward, STATE OF NJ DIVISION OF TAXATION, FOR OFFICIAL USE ONLY Instrument, The Director Division of Taxation, and approval of the Director For. All these will need to be filled in with greatest precision.

Be very careful while completing Deponent Address and STATE OF NJ DIVISION OF TAXATION, since this is where most people make a few mistakes.

Step 3: Prior to getting to the next step, ensure that blanks have been filled in as intended. Once you determine that it's correct, click on “Done." Acquire the Form Rtf 1Ee after you register here for a free trial. Conveniently get access to the form inside your FormsPal account, together with any edits and changes being conveniently kept! FormsPal provides secure form tools devoid of personal information recording or any sort of sharing. Feel safe knowing that your information is secure with us!