Our top level web developers have worked collectively to make the PDF editor that you'll operate. The following software allows you to fill in new york capital improvement documents quickly and efficiently. This is all you need to do.

Step 1: Choose the "Get Form Now" button to begin the process.

Step 2: Now you may edit the new york capital improvement. You may use the multifunctional toolbar to insert, eliminate, and transform the content of the file.

Enter the information required by the application to complete the file.

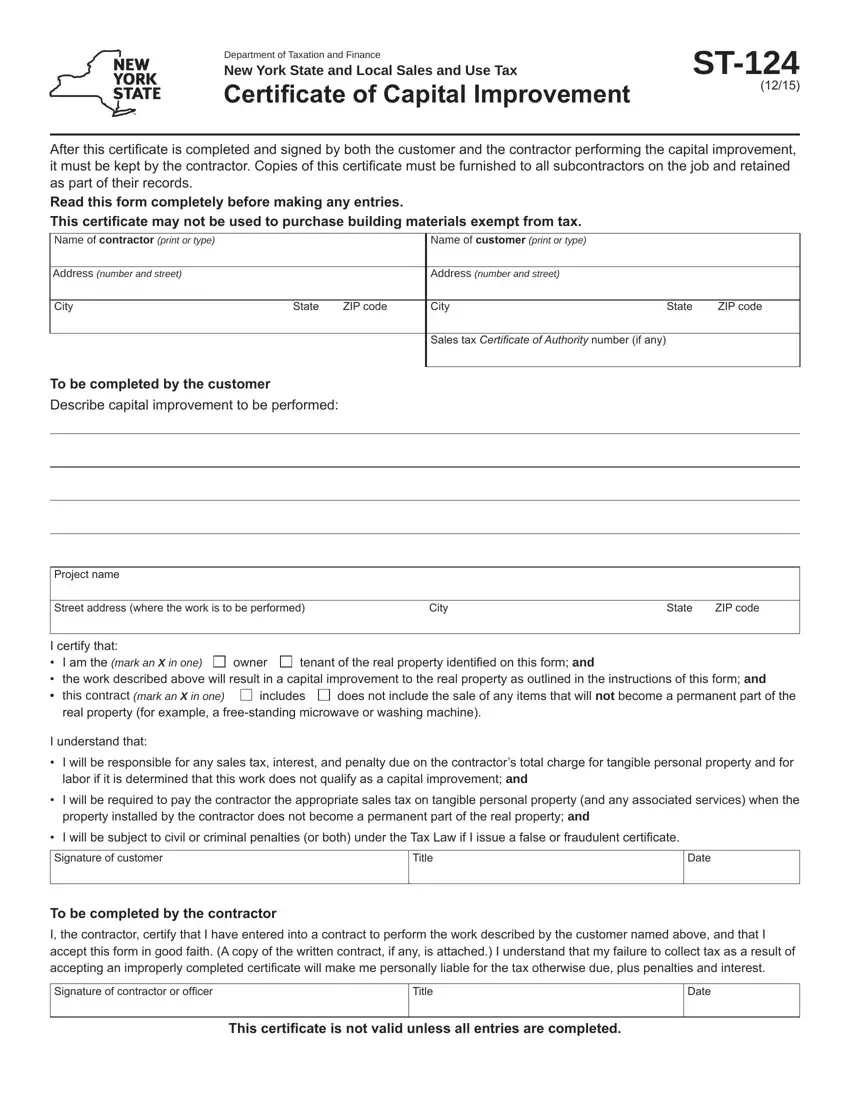

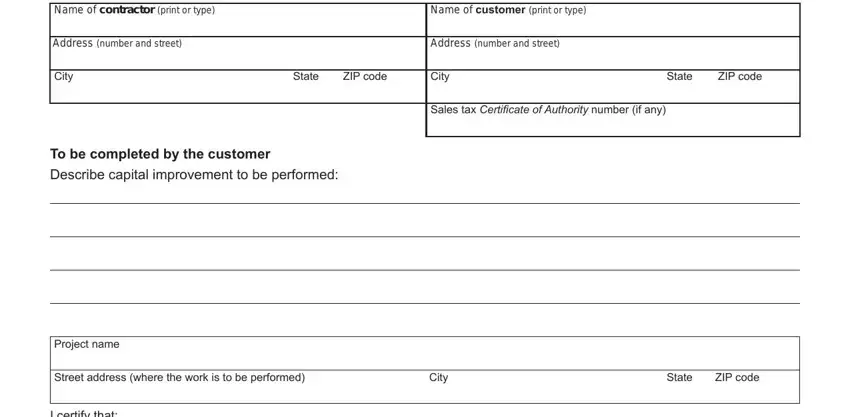

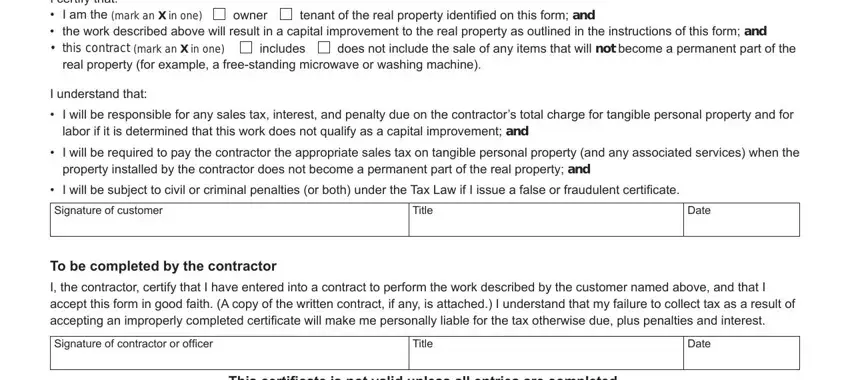

Type in the necessary details in the area I certify that I am the mark an X, tenant of the real property, does not include the sale of any, includes, owner, real property for example a, I understand that, I will be responsible for any, labor if it is determined that, I will be required to pay the, property installed by the, I will be subject to civil or, Signature of customer, Title, and Date.

Step 3: Select the button "Done". The PDF form may be exported. You can easily download it to your device or send it by email.

Step 4: In order to avoid any complications down the road, be sure to prepare up to a few duplicates of your file.