Understanding the nuances of purchasing utilities like electricity, gas, or water in Kansas has been made more approachable with the introduction of the ST-28B form, a necessary document for those seeking a sales tax exemption. This form, mandated by the Kansas Department of Revenue, requires detailed information about the utility service through one meter and is designed to accommodate various entities including agricultural operations, non-profit organizations, educational institutions, and other specific use cases that qualify for exemption under the Kansas Retailers’ Sales Tax Act. The form requires applicants to provide comprehensive details regarding the utility consumption's purpose at a particular meter location, emphasizing the need to accurately delineate between exempt and taxable usage. Additionally, it mandates the inclusion of an Employer ID Number (EIN) or Kansas Sales Tax Registration Number, highlighting a commitment to precise record-keeping. With its attached worksheets, the form guides applicants through the process of calculating the exempt percentage of their utility consumption, a crucial step in obtaining exemption. The ST-28B form is a testament to the state's compliance infrastructure, designed to streamline the process while ensuring that exemptions are granted to eligible parties, thereby reinforcing the importance of understanding and correctly applying for sales tax exemptions on utility usage in Kansas.

| Question | Answer |

|---|---|

| Form Name | Form St 28B |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | st28b.pdf openele wastar fill 600 form |

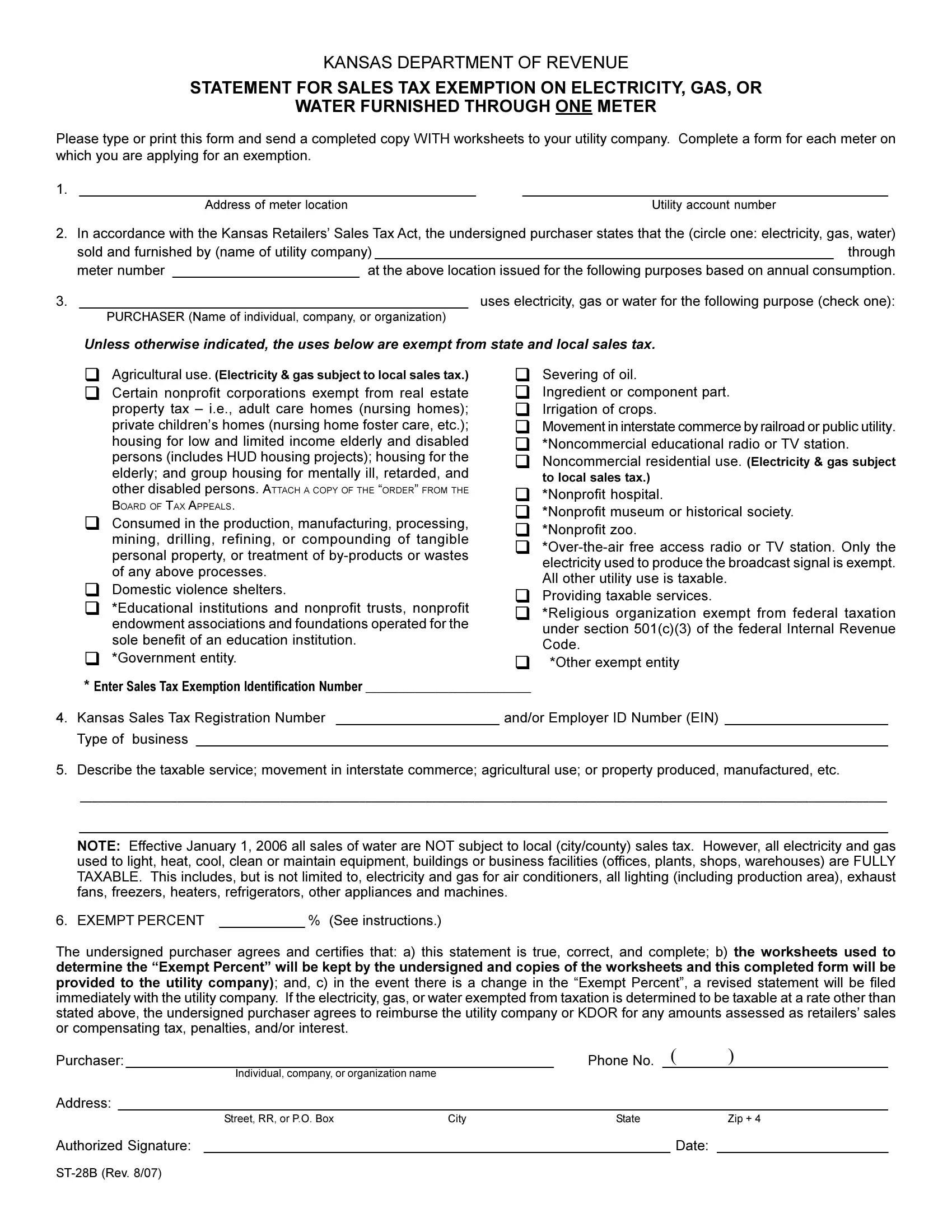

KANSASDEPARTMENTOFREVENUE

STATEMENTFORSALESTAXEXEMPTIONONELECTRICITY,GAS,OR

WATERFURNISHEDTHROUGHONEMETER

Please type or print this form and send a completed copy WITH worksheets to your utility company. Complete a form for each meter on which you are applying for an exemption.

1. |

___________________________________________________ |

_______________________________________________ |

|

Address of meter location |

Utility account number |

2. |

In accordance with the Kansas Retailers’ Sales TaxAct, the undersigned purchaser states that the (circle one: electricity, gas, water) |

|

|

sold and furnished by (name of utility company)___________________________________________________________ through |

|

|

meter number ________________________ at the above location issued for the following purposes based on annual consumption. |

|

3. |

__________________________________________________ |

uses electricity, gas or water for the following purpose (check one): |

|

PURCHASER (Name of individual, company, or organization) |

|

Unless otherwise indicated, theuses beloware exempt from state and local sales tax.

θAgriculturaluse.(Electricity&gassubjecttolocalsalestax.)

θCertain nonprofit corporations exempt from real estate property tax – i.e., adult care homes (nursing homes); private children’s homes (nursing home foster care, etc.); housing for low and limited income elderly and disabled persons (includes HUD housing projects); housing for the elderly; and group housing for mentally ill, retarded, and

other disabled persons. ATTACH A COPY OF THE “ORDER” FROM THE BOARD OF TAX APPEALS.

θConsumed in the production, manufacturing, processing, mining, drilling, refining, or compounding of tangible personal property, or treatment of

θDomestic violence shelters.

θ*Educational institutions and nonprofit trusts, nonprofit endowmentassociationsandfoundationsoperatedforthe sole benefit of an education institution.

θ*Government entity.

θSevering of oil.

θIngredient or component part.

θIrrigation of crops.

θMovementininterstatecommercebyrailroadorpublicutility.

θ*Noncommercial educational radio or TV station.

θNoncommercial residential use. (Electricity & gas subject to local sales tax.)

θ*Nonprofit hospital.

θ*Nonprofit museum or historical society.

θ*Nonprofit zoo.

θ

θProviding taxable services.

θ*Religious organization exempt from federal taxation under section 501(c)(3) of the federal Internal Revenue Code.

θ*Other exempt entity

*Enter Sales Tax Exemption Identification Number __________________________

4.Kansas Sales Tax Registration Number _____________________ and/or Employer ID Number (EIN) _____________________

Type of business _________________________________________________________________________________________

5.Describe the taxable service; movement in interstate commerce; agricultural use; or property produced, manufactured, etc.

_____________________________________________________________________________________________________________________________________

________________________________________________________________________________________________________

NOTE: Effective January 1, 2006 all sales of water are NOT subject to local (city/county) sales tax. However, all electricity and gas used to light, heat, cool, clean or maintain equipment, buildings or business facilities (offices, plants, shops, warehouses) are FULLY TAXABLE. This includes, but is not limited to, electricity and gas for air conditioners, all lighting (including production area), exhaust fans, freezers, heaters, refrigerators, other appliances and machines.

6. EXEMPTPERCENT ___________% (See instructions.)

The undersigned purchaser agrees and certifies that: a) this statement is true, correct, and complete; b) the worksheets used to determine the “Exempt Percent” will be kept by the undersigned and copies of the worksheets and this completed form will be provided to the utility company); and, c) in the event there is a change in the “Exempt Percent”, a revised statement will be filed immediatelywiththeutilitycompany. Iftheelectricity,gas,orwaterexemptedfromtaxationisdeterminedtobetaxableatarateotherthan stated above, the undersigned purchaser agrees to reimburse the utility company or KDOR for any amounts assessed as retailers’sales or compensating tax, penalties, and/or interest.

Purchaser:_______________________________________________________ |

( |

) |

Phone No. _____________________________ |

||

Individual,company,ororganizationname

Address: ___________________________________________________________________________________________________

Street,RR,orP.O.Box City State Zip+4

Authorized Signature: ____________________________________________________________ Date: ______________________

When gas, water, or electricity is furnished through one meter for both taxable and exempt purposes, the purchaser is responsible for determining the percentage of use exempt from sales tax. The sample worksheet provided below will help you todeterminethepercentofelectricity,gas,orwaterthatqualifies for exemption. If you have questions about this form, contact our Taxpayer Assistance Center, Kansas Department of Revenue, 915 SW Harrison St., 1st Floor, Topeka, KS, 66625- 0001, or call (785)

AGRICULTURAL: Electricity and gas for agricultural use is exempt from the state sales tax but not exempt from the local taxes. Agriculturalusedoesnotincludecommercialoperations

CERTAINNONPROFITCORPORATIONS: Salesofelectricity, gas, or water to properties which are exempt from property

CONSUMABLES: The portion of electricity, gas, or water you use that meets the following requirements is exempt from state and local taxes: 1) essential or necessary to the process; 2) used in the actual process at the location during the production activity; 3) immediately consumed or dissipated in the process; and, 4) used in the production, manufacturing, processing, mining, drilling, refining, or compounding of tangible personal

processes. The following uses of electricity, gas, or water are not exempt from sales tax: shipping, repairing, servicing, maintaining,cleaningtheequipmentandthephysicalplant,and storing.

INGREDIENT OR COMPONENT PART: An example of electricity, gas, or water which becomes an ingredient or component part and qualifies for exemption is “water” that is part of the ingredient in a beverage which is bottled and sold to a retailer for resale.

RESIDENTIAL: If the electricity, gas, or water you consume is for residential use only, you do not need to file this form. The utility company automatically exempts you from paying state sales tax (city and county sales tax still applies). However, if theelectricity,gas,orwateryouconsumeispartlyforresidential purposes and partly for commercial use, you must determine the percent of usage that is residential and file copies of your worksheets and this completed form with your utility company and the Department of Revenue. Utilities consumed in commercial common areas such as an office, lounge, hallway, laundryfacility,storagearea,swimmingpool,etc.,donotqualify for exemption.

HOW MUCH OF MY UTILITY USE QUALIFIES FOR EXEMPTION? You will probably need several sheets of paper as worksheets. If your facility is serviced by more than one meter, you need to complete a separate chart to determine the percent of usage for each meter. If the facility is heated and

COLUMN 1 |

|

COLUMN 2 |

COLUMN 3 |

COLUMN 4 |

COLUMN 5 |

COLUMN 6 |

||||

|

|

|

|

|

Estimated |

|

Number of Days |

Usage Per Year |

||

|

|

|

|

Rating of |

Hours of |

|

the Device is |

stated in kWh, |

||

Type of Device |

|

|

Device |

Use Per Day |

Load Factor |

Used Per Year |

BTU, or Gallons |

|||

|

|

|

|

|

|

|

|

|

|

|

20 - light bulbs |

E |

T |

X |

40 watts |

10 |

1.00 |

L |

324 |

E |

2,592 kWh |

|

|

A |

M |

P |

|

|

||||

1 - production machinery |

E |

|

500 watts |

10 |

.50 |

|

255 |

|

637.5 kWh |

|

|

|

|

|

|

|

|

|

|

|

|

1.At the top of each page, place the headers as noted in the example and complete the following information per column:

COLUMN

COLUMN

COLUMN

COLUMN

hours (kWh), BTU, or gallons.

1000 watts = 1 kWh

Horsepower = .746 X H.P. = watts

Ten

1,000,000 BTU in 1 MCF

2.Indicatebesideeachtypeofdevicean“E”forexemptora“T” for taxable.

3.Multiplythequantityincolumn1bycolumn2bycolumn3by column 4 by column 5 to arrive at the sum for column 6.

4.Add the usage per year (column 6) for all of the devices you have indicated as “exempt” then add all of the usage per year(column6)forallthedevicesthatyouhaveindicatedas being“taxable.” Addingtheexemptandtaxableusageshould equalthetotalconsumptionperyearasshownonyourutility bills for the last 12 months.

5.Divide the total number of exempt kWh by the total number of kWh consumed in the last 12 months. This is the percent ofusagethatisexemptfromtax. Enterthisamountonline5 on the front of this form

The instructions provided are intended to help consumers of electricity, gas, or water complete this form.

In case of discrepancies, the applicable law prevails.