Are you having trouble understanding the Tc 675R form? Have you been searching for an overview of the form's purpose and requirements but not had any luck? Look no further; this blog post provides an in-depth analysis of the Tc 675R form, covering topics such as its purpose, contents, when it should be completed, how to fill it out correctly and what resolutions are available if mistakes are made. With our easy-to-understand language and review process, anyone can navigate the complexities of this all-important document. Keep reading to find out more about how Tc 675R forms fit into your annual tax preparation routine!

| Question | Answer |

|---|---|

| Form Name | Tc 675R Form |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | tc form, nyc tc form tc 140, K-1, allocated |

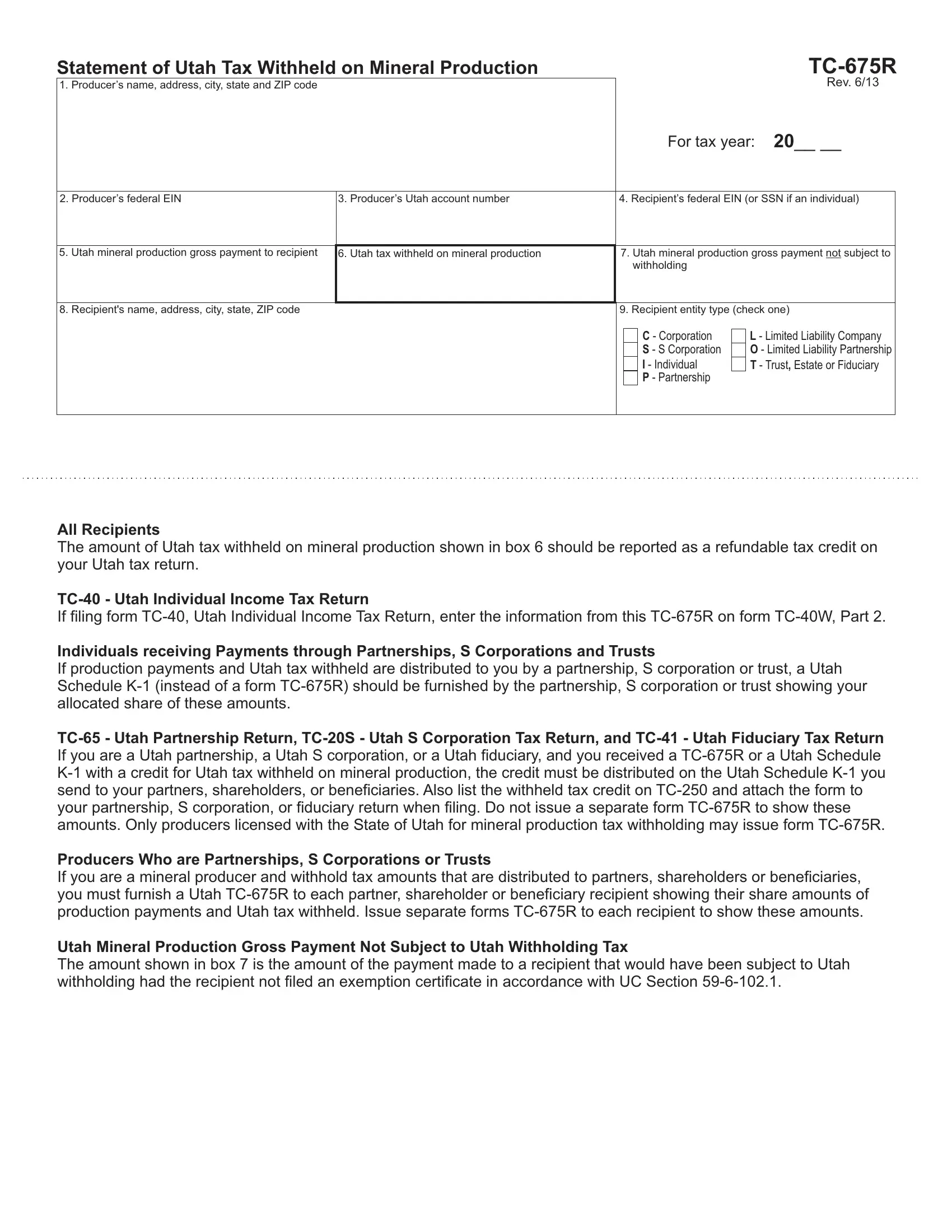

Statement of Utah Tax Withheld on Mineral Production |

|

|

|

|

||

1. Producer’s name, address, city, state and ZIP code |

|

|

|

|

|

Rev. 6/13 |

|

|

|

|

For tax year: 20__ __ |

||

|

|

|

|

|

|

|

2. Producer’s federal EIN |

3. Producer’s Utah account number |

4. Recipient’s federal EIN (or SSN if an individual) |

||||

|

|

|

||||

5. Utah mineral production gross payment to recipient |

6. Utah tax withheld on mineral production |

7. Utah mineral production gross payment not subject to |

||||

|

|

|

withholding |

|

|

|

|

|

|

||||

8. Recipient's name, address, city, state, ZIP code |

|

9. Recipient entity type (check one) |

||||

|

|

|

|

C - Corporation |

|

L - Limited Liability Company |

|

|

|

|

|

||

|

|

|

|

S - S Corporation |

|

O - Limited Liability Partnership |

|

|

|

|

I - Individual |

|

T - Trust, Estate or Fiduciary |

|

|

|

|

P - Partnership |

|

|

|

|

|

|

|

|

|

All Recipients

The amount of Utah tax withheld on mineral production shown in box 6 should be reported as a refundable tax credit on your Utah tax return.

If filing form

Individuals receiving Payments through Partnerships, S Corporations and Trusts

If production payments and Utah tax withheld are distributed to you by a partnership, S corporation or trust, a Utah Schedule

Producers Who are Partnerships, S Corporations or Trusts

If you are a mineral producer and withhold tax amounts that are distributed to partners, shareholders or beneficiaries, you must furnish a Utah

Utah Mineral Production Gross Payment Not Subject to Utah Withholding Tax

The amount shown in box 7 is the amount of the payment made to a recipient that would have been subject to Utah withholding had the recipient not filed an exemption certificate in accordance with UC Section