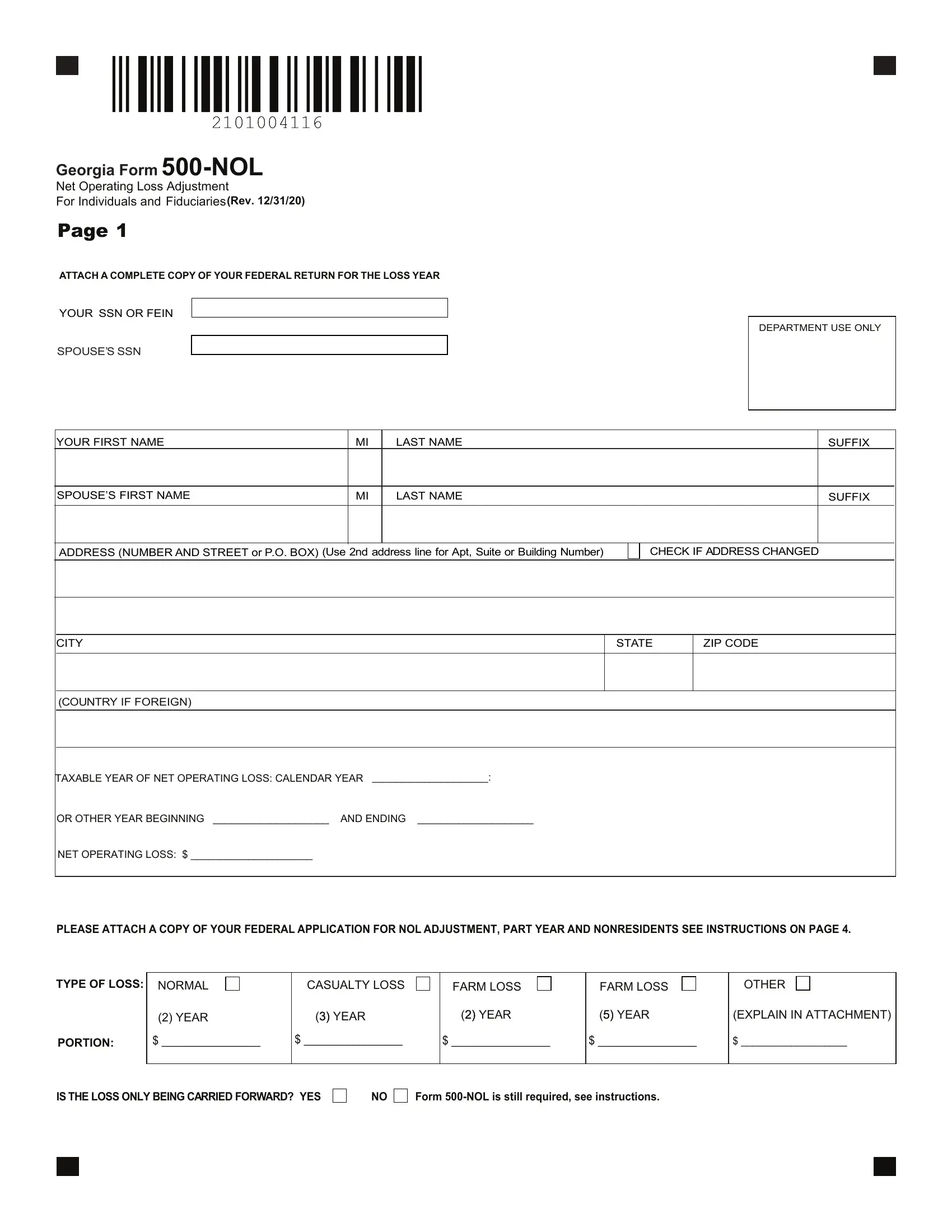

The intricacies of managing financial challenges that arise in the wake of operational losses can be complex for individuals and fiduciaries alike. In Georgia, Form 500-NOL serves as a pivotal tool in navigating these waters, enabling the adjustment of net operating losses. With its detailed requirements, including the attachment of a complete federal return for the loss year and a thorough accounting of the net operating loss across a variety of potential categories such as normal, casualty, and farm losses, the form provides a comprehensive framework for taxpayers. It allows for adjustments to be made over different taxable years, addressing residency status and filing specifics to ensure accurate recalibration of tax obligations. Beyond the mere claim of losses, the form delves into the computation of Georgia adjusted gross income, and deductions, underpinning the determination of taxable income after credits. Moreover, the necessary conditions under which the form must be filed—no later than three years from the due date of the loss year's income tax return, including any extensions—emphasize its role in timely tax planning and amendment. Further complicating matters is the dual mandate that taxpayers also adhere to the procedural sequence dictated by Section 172 of the Internal Revenue Code of 1986 for carrying losses back (if applicable) and forward, with specific exceptions and adjustments unique to Georgia tax law. By requiring a meticulous compilation of both federal and Georgia-specific documents, the form not only seeks to establish a taxpayer's net operating loss within the state's Department of Revenue system but also outlines various carryover schedules and adjustments critical for years following the loss year. The form’s structure and accompanying instructions underscore a broader goal: to provide a clear path for individuals and fiduciaries grappling with operational downturns, ensuring that the process of adjusting for net operating losses is both structured and legally sound.

| Question | Answer |

|---|---|

| Form Name | Georgia Form 500 Nol |

| Form Length | 6 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 30 sec |

| Other names | georgia nol carryback, ga 500 nol instructions, georgia nol carryback instructions, 500 nol |