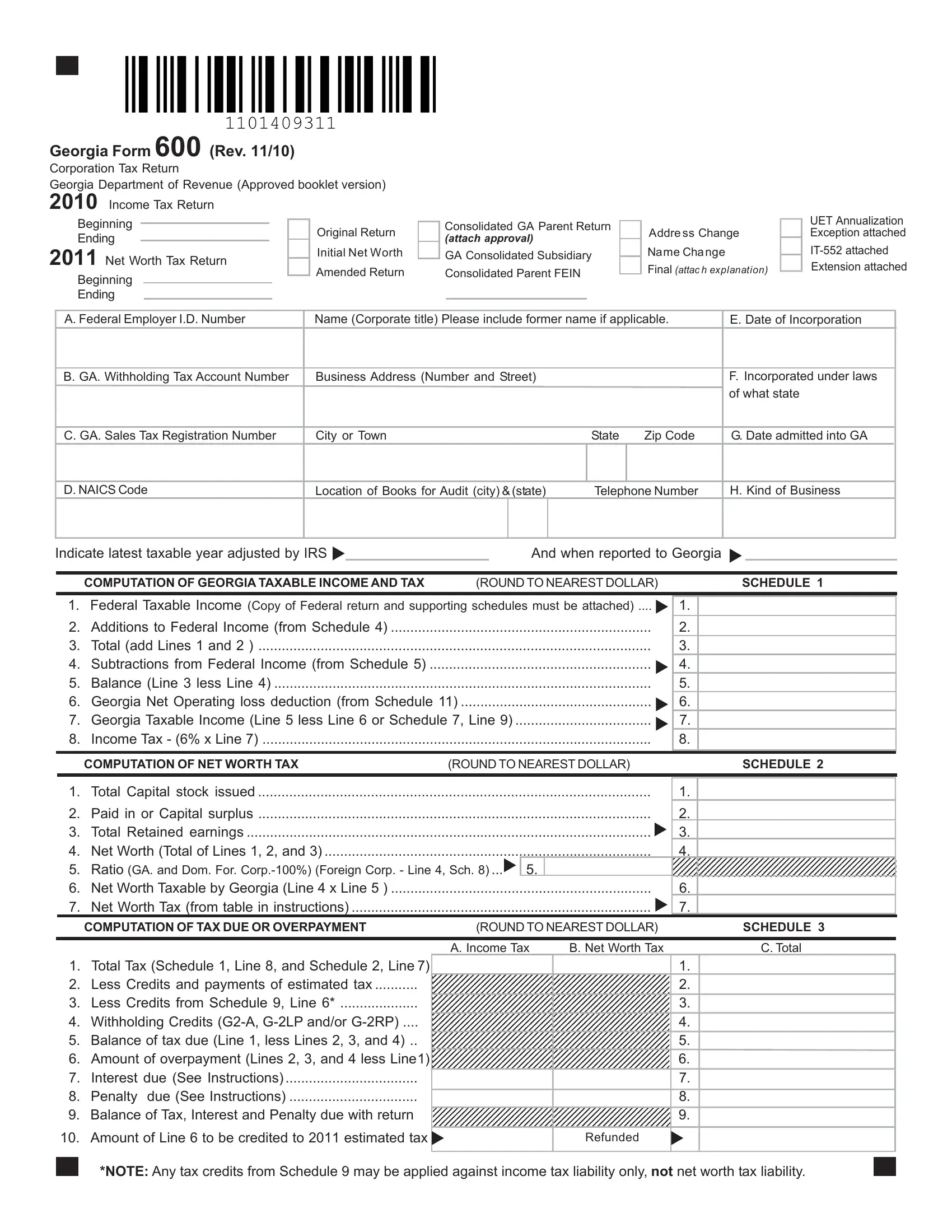

The Georgia Form 600, revised as of November 2010, serves as a critical document for corporations operating within the state, outlining the necessary steps for filing both the Corporation Tax Return and Net Worth Tax Return. Managed by the Georgia Department of Revenue, this form accommodates various filing requirements including original and amended returns, consolidated returns, and instances necessitating an address or name change. The form intricately details the procedure for computing Georgia Taxable Income and Tax, alongside calculations for the Net Worth Tax, adhering to the state's specific guidelines. Such comprehensive computation sections require the submission of the federal return and supporting schedules, underlining the importance of accuracy and completeness in reporting. The form additionally provides space for reporting adjustments to federal taxable income, claiming tax credits, and detailing assignments of such credits among affiliated entities, emphasizing the potential financial implications for the corporation's tax liabilities. The inclusion of a Net Operating Loss (NOL) Carry Forward Worksheet exemplifies the form's role in facilitating longer-term tax planning and management. Furthermore, adherence to payment instructions and the declaration section underscores the legal obligation of corporate officers to ensure the return's veracity. Essentially, Georgia Form 600 encapsulates a crucial aspect of corporate fiscal responsibility within the state, requiring meticulous attention to detail and comprehensive financial reporting.

| Question | Answer |

|---|---|

| Form Name | Georgia Form 600 |

| Form Length | 5 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 15 sec |

| Other names | 600_Blank in ga corp net worth calculation what is g2 a g 2lp andor g 2rp form |