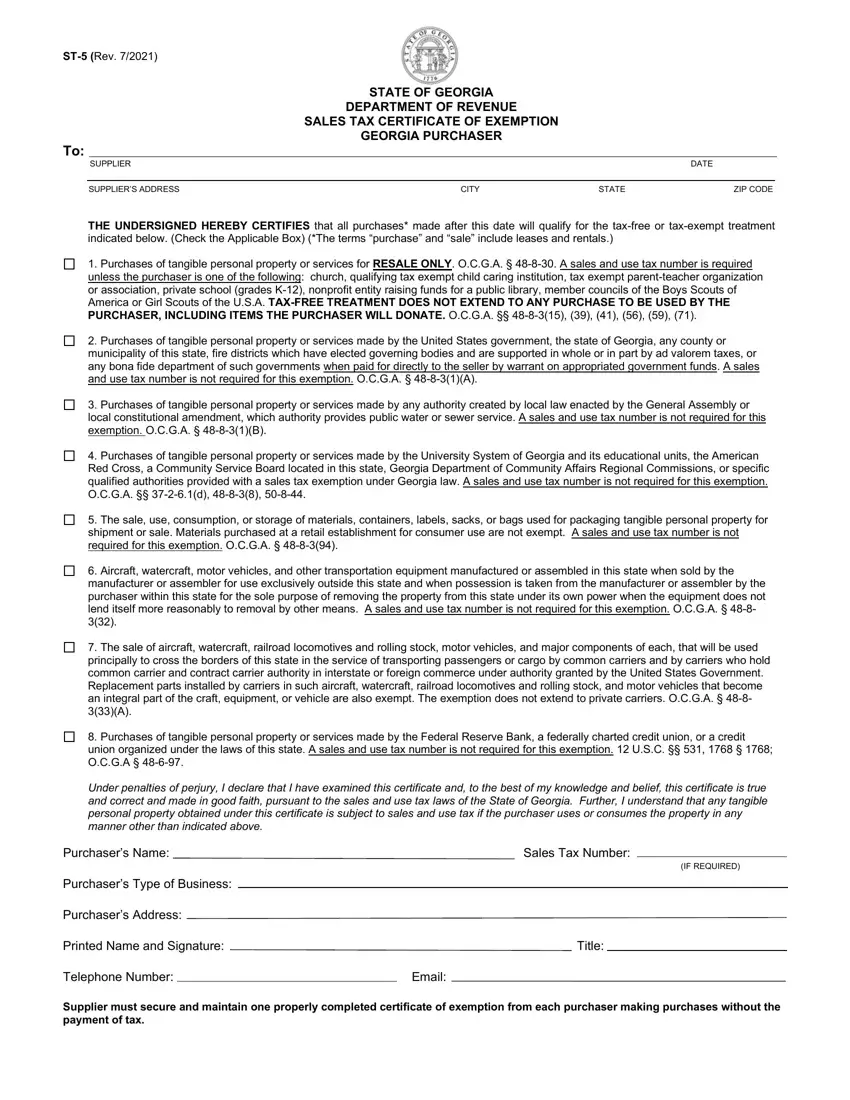

ST-5 (Rev. 7/2021)

STATE OF GEORGIA

DEPARTMENT OF REVENUE

SALES TAX CERTIFICATE OF EXEMPTION

GEORGIA PURCHASER

To:

|

SUPPLIER |

|

|

DATE |

|

|

|

|

|

SUPPLIER’S ADDRESS |

CITY |

STATE |

ZIP CODE |

THE UNDERSIGNED HEREBY CERTIFIES that all purchases* made after this date will qualify for the tax-free or tax-exempt treatment indicated below. (Check the Applicable Box) (*The terms “purchase” and “sale” include leases and rentals.)

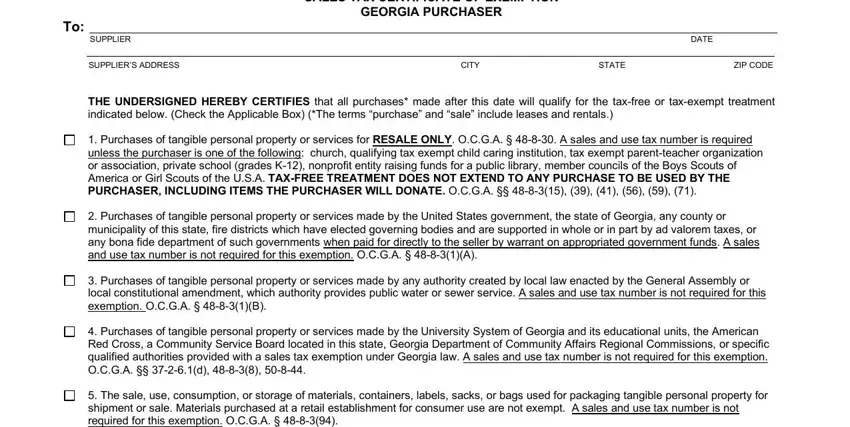

1. Purchases of tangible personal property or services for RESALE ONLY. O.C.G.A. § 48-8-30. A sales and use tax number is required unless the purchaser is one of the following: church, qualifying tax exempt child caring institution, tax exempt parent-teacher organization or association, private school (grades K-12), nonprofit entity raising funds for a public library, member councils of the Boys Scouts of America or Girl Scouts of the U.S.A. TAX-FREE TREATMENT DOES NOT EXTEND TO ANY PURCHASE TO BE USED BY THE PURCHASER, INCLUDING ITEMS THE PURCHASER WILL DONATE. O.C.G.A. §§ 48-8-3(15), (39), (41), (56), (59), (71).

2. Purchases of tangible personal property or services made by the United States government, the state of Georgia, any county or municipality of this state, fire districts which have elected governing bodies and are supported in whole or in part by ad valorem taxes, or any bona fide department of such governments when paid for directly to the seller by warrant on appropriated government funds. A sales and use tax number is not required for this exemption. O.C.G.A. § 48-8-3(1)(A).

3. Purchases of tangible personal property or services made by any authority created by local law enacted by the General Assembly or local constitutional amendment, which authority provides public water or sewer service. A sales and use tax number is not required for this exemption. O.C.G.A. § 48-8-3(1)(B).

4. Purchases of tangible personal property or services made by the University System of Georgia and its educational units, the American Red Cross, a Community Service Board located in this state, Georgia Department of Community Affairs Regional Commissions, or specific qualified authorities provided with a sales tax exemption under Georgia law. A sales and use tax number is not required for this exemption. O.C.G.A. §§ 37-2-6.1(d), 48-8-3(8), 50-8-44.

5. The sale, use, consumption, or storage of materials, containers, labels, sacks, or bags used for packaging tangible personal property for shipment or sale. Materials purchased at a retail establishment for consumer use are not exempt. A sales and use tax number is not required for this exemption. O.C.G.A. § 48-8-3(94).

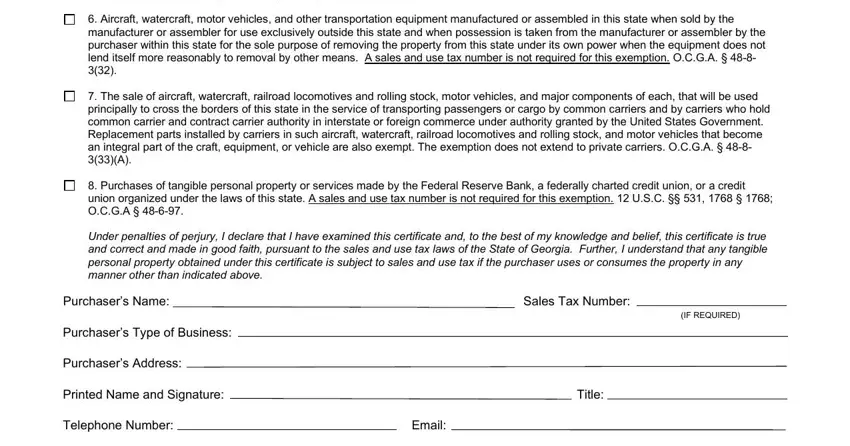

6. Aircraft, watercraft, motor vehicles, and other transportation equipment manufactured or assembled in this state when sold by the manufacturer or assembler for use exclusively outside this state and when possession is taken from the manufacturer or assembler by the purchaser within this state for the sole purpose of removing the property from this state under its own power when the equipment does not lend itself more reasonably to removal by other means. A sales and use tax number is not required for this exemption. O.C.G.A. § 48-8- 3(32).

7. The sale of aircraft, watercraft, railroad locomotives and rolling stock, motor vehicles, and major components of each, that will be used principally to cross the borders of this state in the service of transporting passengers or cargo by common carriers and by carriers who hold common carrier and contract carrier authority in interstate or foreign commerce under authority granted by the United States Government. Replacement parts installed by carriers in such aircraft, watercraft, railroad locomotives and rolling stock, and motor vehicles that become an integral part of the craft, equipment, or vehicle are also exempt. The exemption does not extend to private carriers. O.C.G.A. § 48-8- 3(33)(A).

8. Purchases of tangible personal property or services made by the Federal Reserve Bank, a federally charted credit union, or a credit union organized under the laws of this state. A sales and use tax number is not required for this exemption. 12 U.S.C. §§ 531, 1768 § 1768; O.C.G.A § 48-6-97.

Under penalties of perjury, I declare that I have examined this certificate and, to the best of my knowledge and belief, this certificate is true and correct and made in good faith, pursuant to the sales and use tax laws of the State of Georgia. Further, I understand that any tangible personal property obtained under this certificate is subject to sales and use tax if the purchaser uses or consumes the property in any manner other than indicated above.

Purchaser’s Name: |

Sales Tax Number: |

|

|

|

|

|

|

(IF REQUIRED) |

Purchaser’s Type of Business: |

|

|

|

|

|

|

|

|

Purchaser’s Address: |

|

|

|

Printed Name and Signature: |

Title: |

|

Telephone Number: |

|

|

Email: |