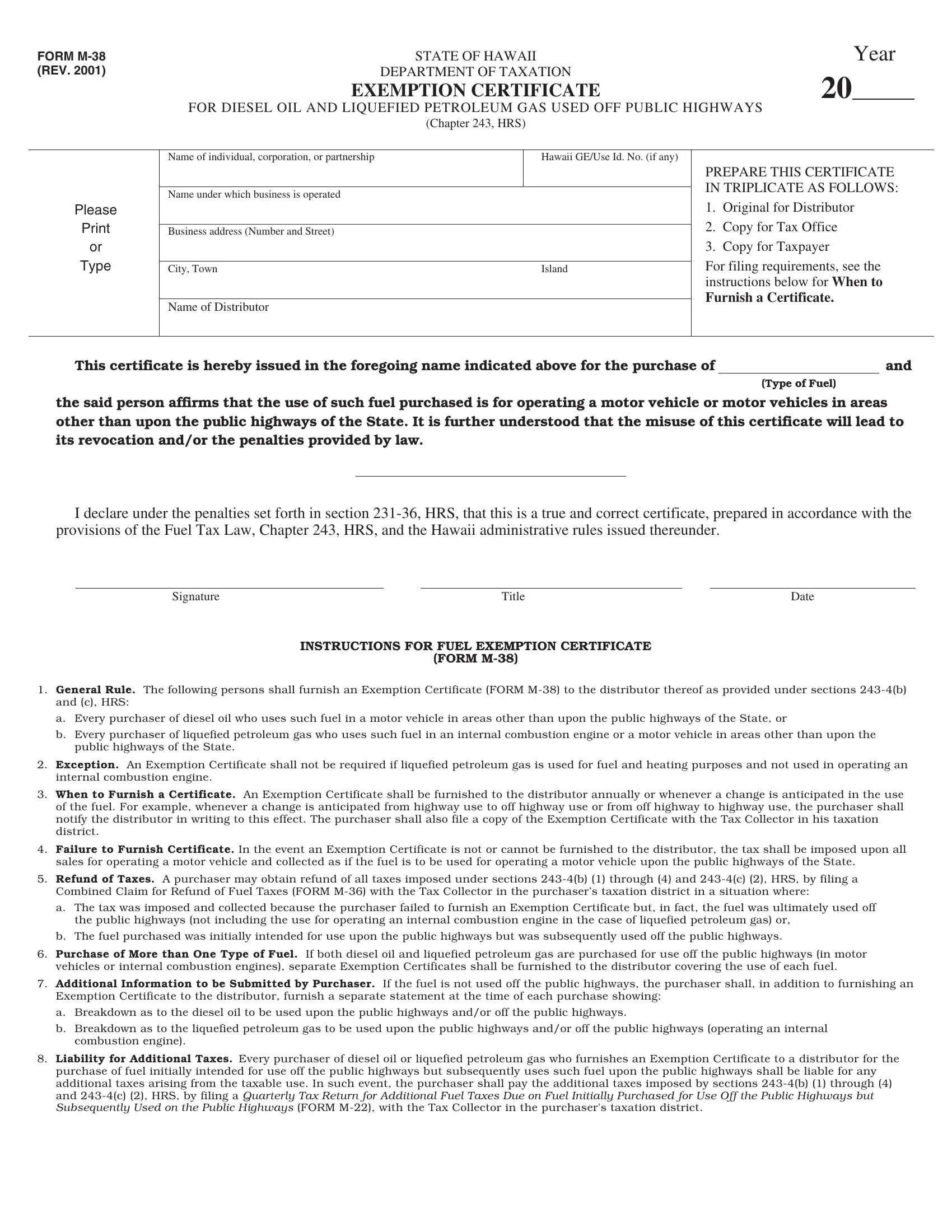

Hawaii's Form M 38 is the report of mortgage loan application activity and originator information for single-family 1-4 unit residential property loans. The form is filed with the Hawaii Division of Financial Institutions (DFI) by licensed mortgage loan originators (MLOs), as required by state law.

| Question | Answer |

|---|---|

| Form Name | Hawaii Form M 38 |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | Diesel_Form_M 38 state of hawaii law on tax exemption m38 form |

FORM |

|

STATE OF HAWAII |

|

|

Year |

|

||

(REV. 2001) |

|

DEPARTMENT OF TAXATION |

|

20 |

|

|

|

|

|

EXEMPTION CERTIFICATE |

|

|

|

|

|||

|

FOR DIESEL OIL AND LIQUEFIED PETROLEUM GAS USED OFF PUBLIC HIGHWAYS |

|

||||||

|

|

(Chapter 243, HRS) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of individual, corporation, or partnership |

|

Hawaii GE/Use Id. No. (if any) |

|

|

|

|

|

|

|

|

|

PREPARE THIS CERTIFICATE |

|

|||

|

|

|

|

IN TRIPLICATE AS FOLLOWS: |

|

|||

|

Name under which business is operated |

|

|

|

||||

|

|

|

|

|

|

|

|

|

Please |

|

|

|

1. |

Original for Distributor |

|

||

|

|

|

2. Copy for Tax Office |

|

||||

Business address (Number and Street) |

|

|

|

|||||

or |

|

|

|

3. Copy for Taxpayer |

|

|||

Type |

|

|

|

For filing requirements, see the |

|

|||

City, Town |

|

Island |

|

|||||

|

|

|

|

instructions below for WHEN TO |

|

|||

|

|

|

|

FURNISH A CERTIFICATE. |

|

|||

|

Name of Distributor |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This certificate is hereby issued in the foregoing name indicated above for the purchase of |

|

|

and |

|

||||

|

|

|

|

|

(Type of Fuel) |

|

||

the said person affirms that the use of such fuel purchased is for operating a motor vehicle or motor vehicles in areas other than upon the public highways of the State. It is further understood that the misuse of this certificate will lead to its revocation and/or the penalties provided by law.

I declare under the penalties set forth in section

Signature |

Title |

Date |

INSTRUCTIONS FOR FUEL EXEMPTION CERTIFICATE

(FORM

1.General Rule. The following persons shall furnish an Exemption Certificate (FORM

a.Every purchaser of diesel oil who uses such fuel in a motor vehicle in areas other than upon the public highways of the State, or

b.Every purchaser of liquefied petroleum gas who uses such fuel in an internal combustion engine or a motor vehicle in areas other than upon the public highways of the State.

2.Exception. An Exemption Certificate shall not be required if liquefied petroleum gas is used for fuel and heating purposes and not used in operating an internal combustion engine.

3.When to Furnish a Certificate. An Exemption Certificate shall be furnished to the distributor annually or whenever a change is anticipated in the use of the fuel. For example, whenever a change is anticipated from highway use to off highway use or from off highway to highway use, the purchaser shall notify the distributor in writing to this effect. The purchaser shall also file a copy of the Exemption Certificate with the Tax Collector in his taxation district.

4.Failure to Furnish Certificate. In the event an Exemption Certificate is not or cannot be furnished to the distributor, the tax shall be imposed upon all sales for operating a motor vehicle and collected as if the fuel is to be used for operating a motor vehicle upon the public highways of the State.

5.Refund of Taxes. A purchaser may obtain refund of all taxes imposed under sections

a.The tax was imposed and collected because the purchaser failed to furnish an Exemption Certificate but, in fact, the fuel was ultimately used off the public highways (not including the use for operating an internal combustion engine in the case of liquefied petroleum gas) or,

b.The fuel purchased was initially intended for use upon the public highways but was subsequently used off the public highways.

6.Purchase of More than One Type of Fuel. If both diesel oil and liquefied petroleum gas are purchased for use off the public highways (in motor vehicles or internal combustion engines), separate Exemption Certificates shall be furnished to the distributor covering the use of each fuel.

7.Additional Information to be Submitted by Purchaser. If the fuel is not used off the public highways, the purchaser shall, in addition to furnishing an Exemption Certificate to the distributor, furnish a separate statement at the time of each purchase showing:

a.Breakdown as to the diesel oil to be used upon the public highways and/or off the public highways.

b.Breakdown as to the liquefied petroleum gas to be used upon the public highways and/or off the public highways (operating an internal combustion engine).

8.Liability for Additional Taxes. Every purchaser of diesel oil or liquefied petroleum gas who furnishes an Exemption Certificate to a distributor for the purchase of fuel initially intended for use off the public highways but subsequently uses such fuel upon the public highways shall be liable for any additional taxes arising from the taxable use. In such event, the purchaser shall pay the additional taxes imposed by sections