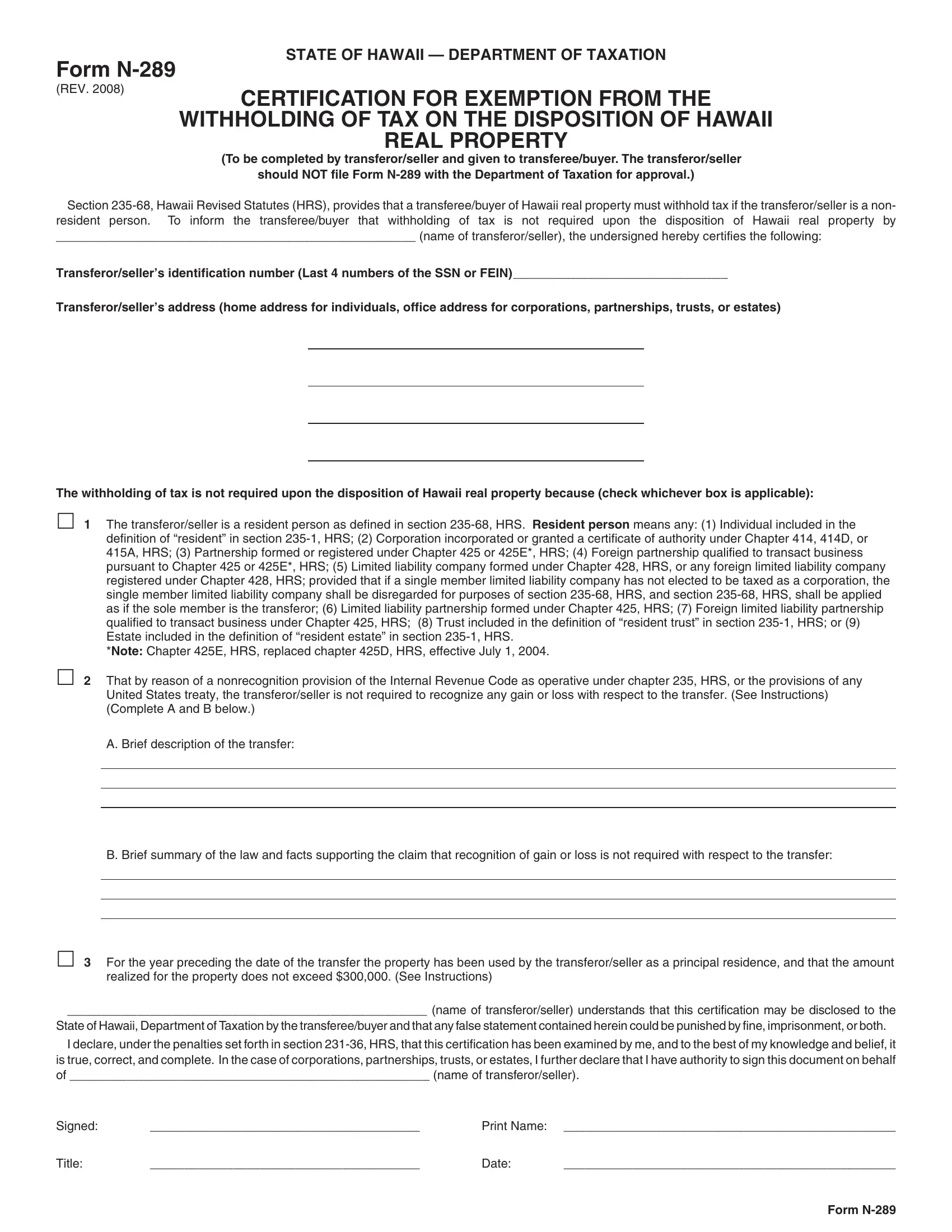

A crucial aspect of real estate transactions in Hawaii involves understanding and properly executing Form N-289, officially termed the Certification for Exemption from the Withholding of Tax on the Disposition of Hawaii Real Property. This form plays an essential role in facilitating the smooth transfer of property by providing a mechanism for certain sellers to certify their exemption from tax withholding requirements at the point of sale. Predominantly, this form is applicable to three categories of transactions: those involving resident sellers, transactions exempt under specific nonrecognition provisions of the Internal Revenue Code or U.S. treaties, and sales of principal residences that fall within specified financial thresholds. A notable feature of this process is that this declaration of exemption, although mandatory for qualifying sellers to complete and provide to buyers, does not require submission to the Hawaii Department of Taxation. The guidelines also spell out who may complete the form — including individuals, corporations, partnerships, trusts, and estates — underscoring the significance of accurate completion that requires detailed personal and transactional information. The form mandates disclosing the identity and status of the seller, along with a descriptive and legal rationale for the exemption claimed, thereby ensuring that all parties are well-informed and compliant with Hawaiian tax laws. Additionally, Form N-289 underscores the continual obligation of sellers to report the transaction on their income tax returns, despite the potential exemption from withholding. Instructions accompanying the form provide further clarification on these procedures, aiming to streamline the process for all involved parties while aligning with statutory requirements. Thus, Form N-289 serves as a critical tool in the conveyance of real property in Hawaii, embodying proactive measures to facilitate compliance, transparency, and fairness in property transactions.

| Question | Answer |

|---|---|

| Form Name | Hawaii Form N 289 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | ITINs, N-288, 425D, transferee |