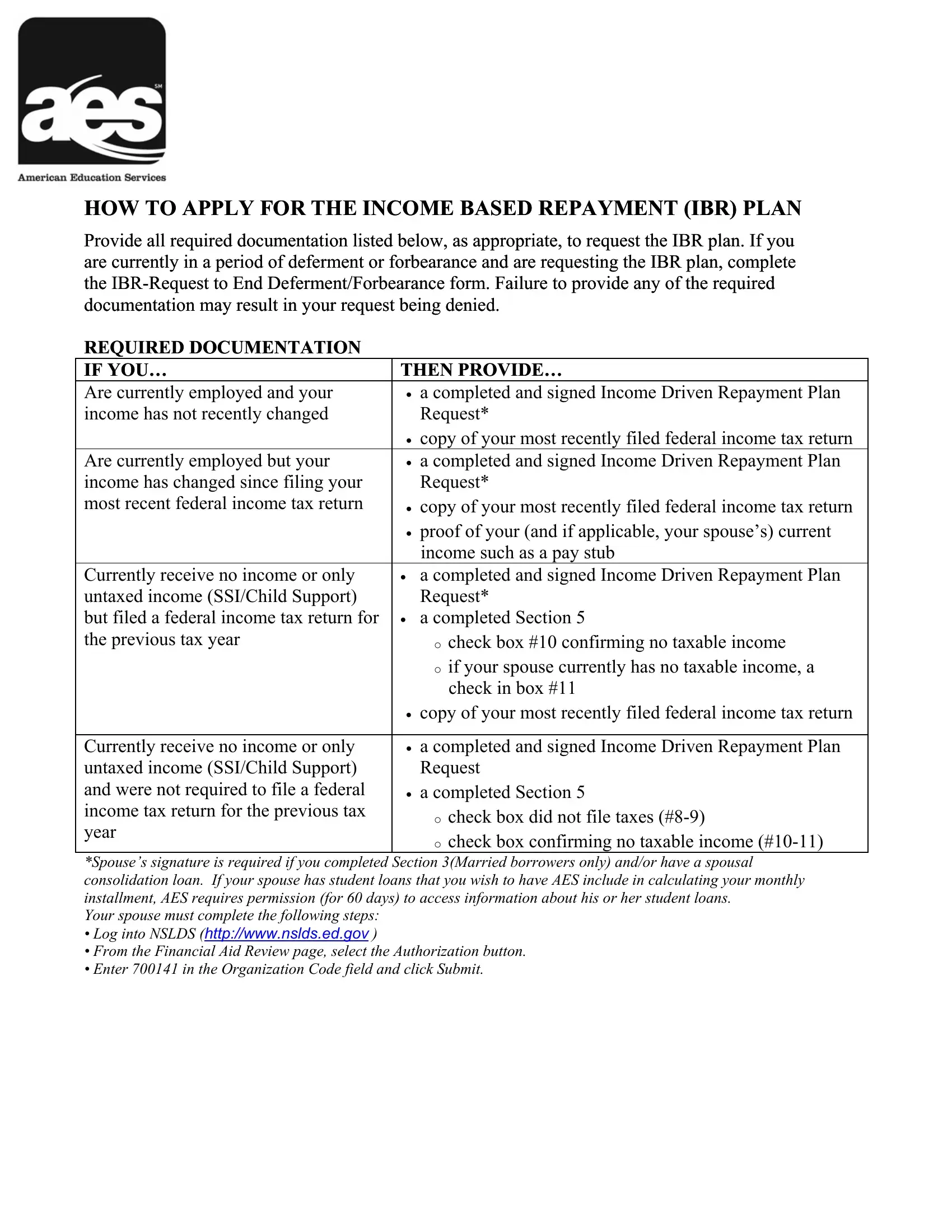

HOW TO APPLY FOR THE INCOME BASED REPAYMENT (IBR) PLAN

Provide all required documentation listed below, as appropriate, to request the IBR plan. If you are currently in a period of deferment or forbearance and are requesting the IBR plan, complete the IBR-Request to End Deferment/Forbearance form. Failure to provide any of the required documentation may result in your request being denied.

REQUIRED DOCUMENTATION

IF YOU… |

THEN PROVIDE… |

Are currently employed and your |

• |

a completed and signed Income Driven Repayment Plan |

income has not recently changed |

|

Request* |

|

• |

copy of your most recently filed federal income tax return |

Are currently employed but your |

• |

a completed and signed Income Driven Repayment Plan |

income has changed since filing your |

|

Request* |

most recent federal income tax return |

• |

copy of your most recently filed federal income tax return |

|

• |

proof of your (and if applicable, your spouse’s) current |

|

|

income such as a pay stub |

Currently receive no income or only |

• |

a completed and signed Income Driven Repayment Plan |

untaxed income (SSI/Child Support) |

|

Request* |

but filed a federal income tax return for |

• |

a completed Section 5 |

the previous tax year |

|

O check box #10 confirming no taxable income |

|

|

O if your spouse currently has no taxable income, a |

|

|

check in box #11 |

|

• |

copy of your most recently filed federal income tax return |

|

|

|

Currently receive no income or only |

• |

a completed and signed Income Driven Repayment Plan |

untaxed income (SSI/Child Support) |

|

Request |

and were not required to file a federal |

• |

a completed Section 5 |

income tax return for the previous tax |

|

O check box did not file taxes (#8-9) |

year |

|

|

O check box confirming no taxable income (#10-11) |

|

|

*Spouse’s signature is required if you completed Section 3(Married borrowers only) and/or have a spousal consolidation loan. If your spouse has student loans that you wish to have AES include in calculating your monthly installment, AES requires permission (for 60 days) to access information about his or her student loans.

Your spouse must complete the following steps:

•Log into NSLDS (http://www.nslds.ed.gov )

•From the Financial Aid Review page, select the Authorization button.

•Enter 700141 in the Organization Code field and click Submit.

Income-Based (IBR) / Pay As You Earn / Income-Contingent (ICR) Repayment Plan Request

William D. Ford Federal Direct Loan (Direct Loan) Program / Federal Family Education Loan (FFEL) Program

Use this form to (1) request an available repayment plan based on your income, (2) provide the required information for the annual reevaluation of your payment amount under one of these plans, or (3) request that your loan holder recalculate your monthly payment amount.

OMB No. 1845-0102

Form Approved

Exp. Date 11-30-2015

IBR/PAYE/ICR |

WARNING: Any person who knowingly makes a false statement or misrepresentation on this form or on any accompanying document is subject to penalties that may include fines, |

|

|

imprisonment, or both, under the U.S. Criminal Code and 20 U.S.C. 1097. |

SECTION 1: BORROWER IDENTIFICATION

Please enter or correct the following information.

Check this box if any of your information has changed.

SSN |

|

Name |

|

Address |

|

City, State, Zip Code |

|

Telephone – Primary |

( |

Telephone – Alternate |

( |

E-mail Address (Optional) |

|

SECTION 2: REPAYMENT PLAN REQUEST

Before completing this form, carefully read the entire form, particularly Sections 7, 8, and 9. Type or print using dark ink. If you need help completing this form, contact your loan holder(s). Return the completed form and any required documentation to the address shown in Section 10. You may be able to complete your request online by visiting studentloans.gov. Information about repayment plans and calculators are available at studentaid.gov.

Other repayment plans, such as extended or graduated, may be available and may offer a lower monthly payment amount. In addition, payment under the IBR, Pay As You Earn, or ICR plans may result in your paying more interest over time and may result in federal income tax liability on any loan amount that is forgiven under these plans.

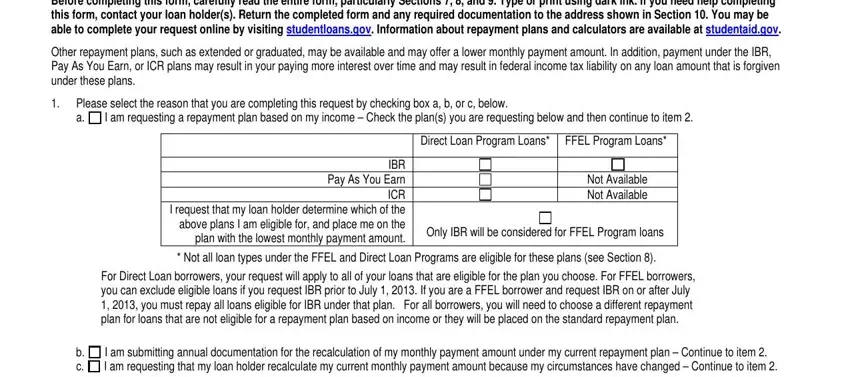

1.Please select the reason that you are completing this request by checking box a, b, or c, below.

a. I am requesting a repayment plan based on my income – Check the plan(s) you are requesting below and then continue to item 2.

|

|

Direct Loan Program Loans* |

FFEL Program Loans* |

|

|

|

|

|

IBR |

|

|

|

Pay As You Earn |

|

Not Available |

|

ICR |

|

Not Available |

|

I request that my loan holder determine which of the |

|

|

|

above plans I am eligible for, and place me on the |

Only IBR will be considered for FFEL Program loans |

|

plan with the lowest monthly payment amount. |

|

|

|

* Not all loan types under the FFEL and Direct Loan Programs are eligible for these plans (see Section 8).

For Direct Loan borrowers, your request will apply to all of your loans that are eligible for the plan you choose. For FFEL borrowers, you can exclude eligible loans if you request IBR prior to July 1, 2013. If you are a FFEL borrower and request IBR on or after July 1, 2013, you must repay all loans eligible for IBR under that plan. For all borrowers, you will need to choose a different repayment plan for loans that are not eligible for a repayment plan based on income or they will be placed on the standard repayment plan.

b. I am submitting annual documentation for the recalculation of my monthly payment amount under my current repayment plan – Continue to item 2.

c. I am requesting that my loan holder recalculate my current monthly payment amount because my circumstances have changed – Continue to item 2.

2. Check this box if you owe eligible loans to more than one loan holder. You must submit a separate request to each holder of the loans you want to repay under the IBR, Pay As You Earn, or ICR plan.

You must promptly submit to your loan holder(s) this completed form and acceptable documentation of your Adjusted Gross Income (see Section 4), or, if applicable, alternative documentation of your current income (see Section 5).

SECTION 3: SPOUSAL INFORMATION

Complete this section if any of the following apply to you:

You file a joint federal income tax return with your spouse and your spouse has eligible loans. Enter information about your spouse, below. You have a joint Direct or FFEL Consolidation Loan that you obtained with your spouse. Enter information about the co-borrower of the loan.

You and your spouse have Direct Loans and both of you want to repay those loans under the ICR Plan. Enter information about your spouse, below.

3. Spouse’s SSN |

|

|

|

- |

|

|

- |

|

|

|

|

|

|

|

4. |

Spouse’s Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

Spouse’s Date of Birth |

|

|

- |

|

|

- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6. |

My spouse and I wish to repay our Direct Loans jointly under the ICR Plan. |

|

|

|

If you file a joint federal income tax return with your spouse, your loan holder(s) will base your eligibility determination and monthly payment amount on your and your spouse’s combined income regardless of whether your spouse has eligible federal student loans. However, if your spouse does not have eligible student loans, you do not need to complete this section.

If you complete this section, your spouse is also required to sign this form. By signing, your spouse is authorizing the loan holder(s) to access information about his or her federal student loans in the National Student Loan Data System (NSLDS). In addition, if the Department is not your loan holder and your FFEL loan holder(s) does not service at least one of your spouse’s loans, your loan holder(s) will need detailed information about all of your spouse’s loans to accurately evaluate your eligibility and payment amount. Your spouse should log into NSLDS at nslds.ed.gov to give your loan holder(s) access to his or her loan information. To obtain the organization code needed for authorization on NSLDS or for other options to provide the loan details needed on your spouse’s loans, contact your loan holder(s).

Page 1 of 5

SECTION 4: FAMILY SIZE AND FEDERAL TAX INFORMATION

Enter your family size (as defined in Section 8).

Note: If you do not enter your family size, your loan holder(s) will assume a family size of one. For purposes of these repayment plans, your family size may be different from the number of exemptions you claim on your federal tax return. By signing this form, you are certifying that the family size you enter above is correct.

8.Did you file a federal income tax return for either of the two most recently completed tax years?

Yes – Continue to Item 9.

No – Skip to Section 5.

9.Is your current income or your spouse’s current income (if you completed Section 3 or file a joint federal income tax return) significantly different than the income used to determine the Adjusted Gross Income* (AGI) reported to the IRS on your most recently filed federal income tax return?

Yes – Continue to Section 5.

No – Provide your most recently filed federal income tax return or IRS tax return transcript. Skip to Section 6.

*You can find your Adjusted Gross Income on your most recently filed IRS Form 1040, 1040A, or 1040EZ.

SECTION 5: ALTERNATIVE DOCUMENTATION OF INCOME

To be completed if (1) you did not file a federal income tax return for the two most recently completed tax years, (2) your AGI from your most recently filed federal income tax return does not reasonably reflect your current income (due to circumstances such as the loss of or change in employment), or (3) your loan holder(s) informed you that alternative documentation of income is required.

10.Do you have taxable income? Check “No” if (1) you do not have any income, (2) receive only untaxed income (such as Supplemental Security Income, child support, or federal or state public assistance), or (3) are not required to file a federal income tax return based on the amount of your taxable income.

Yes – Provide documentation of this income, as described below.

No – By signing this form, you are certifying that you have no taxable income or are not required to file a federal income tax return based on the amount of your taxable income.

11.If you are married and completed Section 3 or file a joint federal income tax return with your spouse, does your spouse have taxable income? Check “No” if (1) your spouse does not have any income, (2) receives only untaxed income (such as Supplemental Security Income, child support, or federal or state public assistance), or (3) is not required to file a federal income tax return based on the amount of his/her taxable income.

Yes – Provide documentation of your spouse’s income, as described below.

No – By signing this form, your spouse is certifying that he/she has no taxable income or is not required to file a federal tax return based on the amount of his/her taxable income.

You must provide documentation of all taxable income that you currently receive from all sources (for example, income from employment, unemployment income, dividend income, interest income, tips, alimony). If you are married and completed Section 3 or file a joint federal income tax return, you must also provide documentation of your spouse’s taxable income. Do not report untaxed income such as Supplemental Security Income, child support, or federal or state public assistance.

You must provide one piece of supporting documentation for each source of income (your and your spouse’s). For example, documentation includes pay stubs, a letter(s) from your employer(s) listing income, interest or bank statements, or dividend statements. If these forms of documentation are unavailable, attach a signed statement from you or your spouse explaining the income source(s) and giving the name and the address of the source(s).

Unless the frequency is clearly indicated on the documentation that you provide, write on your documentation how often you receive the income, for example, “twice per month” or “every other week”. The date on any supporting documentation you provide must be no older than 90 days from the date you sign this form. Copies of original documentation are acceptable.

SECTION 6: BORROWER REQUEST, UNDERSTANDINGS, AGREEMENT, AUTHORIZATION, AND CERTIFICATION

I request to use the plan I selected in Section 2 to repay my eligible Direct Loan or FFEL Program loans held by the holder(s) to which I submit this form. If I selected the option to allow my loan holder(s) to choose my plan, I request my loan holder(s) to place me in the plan with the lowest monthly payment amount. If more than one plan provides the same initial payment amount, I understand that my loan holder will choose the plan that is likely to keep my monthly payment amount lower in subsequent years.

I understand that: (1) If I am entering repayment on my loan(s) for the first time and do not provide my loan holder(s) with this completed form and any other documentation required by my loan holder(s), or if I do not qualify for the repayment plan that I requested, I will be placed on the standard repayment plan (see Section 8). (2) If I am currently repaying my loan(s) under a different repayment plan and want to change to the repayment plan I selected in Section 2, my loan holder(s) may grant me a forbearance for up to 60 days to collect and process documentation supporting my request for the selected plan. I am not required to make loan payments during this period of forbearance, but interest will continue to accrue. Unpaid interest that accrues during this maximum 60-day forbearance period will not be capitalized (see Section 8). (3) If I am delinquent in making payments under my current repayment plan at the time I request one of the repayment plans listed in Section 2, my loan holder(s) may grant me a forbearance to cover any payments that are overdue, or that would be due, at the time I enter the repayment plan I requested. Unpaid interest that accrues during this forbearance period may be capitalized. (4) If I am requesting the ICR plan, my initial payment amount will be the amount of interest that accrues each month on my loan(s) until my loan holder receives the income documentation needed to calculate my ICR payment amount. If I cannot afford the initial interest payments, I may request forbearance by contacting my loan holder.

I authorize the entity to which I submit this request (i.e., the school, the lender, the guaranty agency, the U.S. Department of Education, and their respective agents and contractors) to contact me regarding my request or my loan(s), including repayment of my loan(s), at the number that I provide on this form or any future number that I provide for my cellular telephone or other wireless device using automated telephone dialing equipment or artificial or prerecorded voice or text messages.

I certify that all of the information I have provided on this form and in any accompanying documentation is true, complete, and correct to the best of my knowledge and belief.

|

|

|

|

Borrower’s Signature |

|

Date |

Spouse’s Signature (if required) |

|

Date |

Note: Your spouse’s signature is required if you completed Section 3 and/or completed Item 11. |

|

SECTION 7: INSTRUCTIONS FOR COMPLETING THE FORM

Type or print using dark ink. Enter dates as month-day-year (mm-dd-yyyy). Use only numbers. Example: January 31, 2012 = 01-31-2012. Include your name and account number on any documentation that you are required to submit with this form. If you need help completing this form, contact your loan holder(s). If you want to apply for a repayment plan on loans that are held by different loan holders, you must submit a separate request to each loan holder.

Use this form to (1) request the IBR, Pay As You Earn, or ICR plan for repayment of your Direct Loans or the IBR plan for your FFEL program loan(s), (2) to submit annual documentation for the calculation of the payment amount under the IBR, Pay As You Earn, or ICR plan, or (3) request that your loan holder recalculate your current monthly payment amount because your circumstances have changed. To use the IBR or Pay As You Earn plan, you must meet the eligibility requirements for those plans described in Section 9. Repayment plan calculators are available at studentaid.gov. The calculators are only informational; your loan holder(s) will make the official determination of your eligibility and payment amount based on the information you provide on this form and other required documentation.

You must provide your loan holder(s) with income documentation that will be used to determine your eligibility for the IBR or Pay As You Earn plan and your payment amount for the IBR, Pay As You Earn, or ICR plan, as described in Section 9.

Return the completed form and any required documentation to the address shown in Section 10.

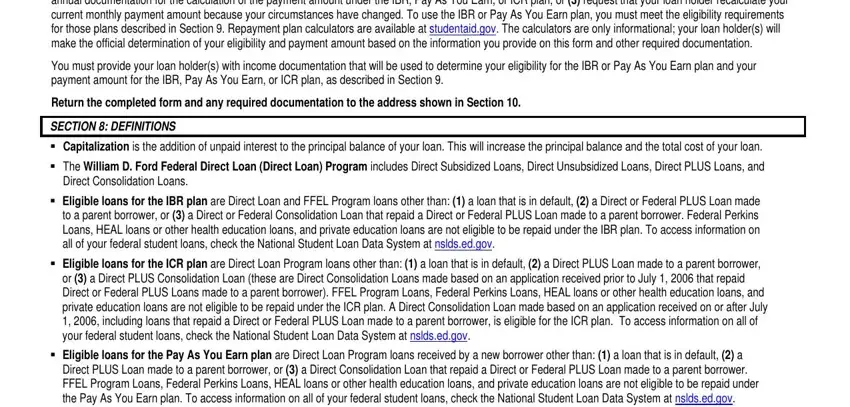

SECTION 8: DEFINITIONS

Capitalization is the addition of unpaid interest to the principal balance of your loan. This will increase the principal balance and the total cost of your loan.

The William D. Ford Federal Direct Loan (Direct Loan) Program includes Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and Direct Consolidation Loans.

Eligible loans for the IBR plan are Direct Loan and FFEL Program loans other than: (1) a loan that is in default, (2) a Direct or Federal PLUS Loan made to a parent borrower, or (3) a Direct or Federal Consolidation Loan that repaid a Direct or Federal PLUS Loan made to a parent borrower. Federal Perkins Loans, HEAL loans or other health education loans, and private education loans are not eligible to be repaid under the IBR plan. To access information on all of your federal student loans, check the National Student Loan Data System at nslds.ed.gov.

Eligible loans for the ICR plan are Direct Loan Program loans other than: (1) a loan that is in default, (2) a Direct PLUS Loan made to a parent borrower, or (3) a Direct PLUS Consolidation Loan (these are Direct Consolidation Loans made based on an application received prior to July 1, 2006 that repaid Direct or Federal PLUS Loans made to a parent borrower). FFEL Program Loans, Federal Perkins Loans, HEAL loans or other health education loans, and private education loans are not eligible to be repaid under the ICR plan. A Direct Consolidation Loan made based on an application received on or after July 1, 2006, including loans that repaid a Direct or Federal PLUS Loan made to a parent borrower, is eligible for the ICR plan. To access information on all of your federal student loans, check the National Student Loan Data System at nslds.ed.gov.

Eligible loans for the Pay As You Earn plan are Direct Loan Program loans received by a new borrower other than: (1) a loan that is in default, (2) a Direct PLUS Loan made to a parent borrower, or (3) a Direct Consolidation Loan that repaid a Direct or Federal PLUS Loan made to a parent borrower. FFEL Program Loans, Federal Perkins Loans, HEAL loans or other health education loans, and private education loans are not eligible to be repaid under the Pay As You Earn plan. To access information on all of your federal student loans, check the National Student Loan Data System at nslds.ed.gov.

Family size includes you, your spouse, and your children (including unborn children who will be born during the year for which you certify your family size), if the children will receive more than half their support from you. It includes other people only if they live with you now, they receive more than half their support from you now, and they will continue to receive this support from you for the year that you certify your family size. Support includes money, gifts, loans, housing, food, clothes, car, medical and dental care, and payment of college costs.

The Federal Family Education Loan (FFEL) Program includes Federal Stafford Loans (both subsidized and unsubsidized), Federal PLUS Loans, Federal Consolidation Loans, and Federal Supplemental Loans for Students (SLS).

The holder of your Direct Loans is the U.S. Department of Education (the Department). The holder(s) of your FFEL Program loan(s) may be a lender, secondary market, guaranty agency, or the Department. Your loan holder(s) may use a servicer to handle billing, payment, repayment options, and other communications on your loans. References to “your loan holder” on this form mean either your loan holder(s) or, if your loan holder(s) and servicer are different entities, your servicer.

The Income-Based Repayment (IBR) plan is a repayment plan with monthly payments that are limited to 15 percent of your discretionary income divided by 12. Discretionary income for this plan is the difference between your adjusted gross income and 150 percent of the poverty guideline amount for your state of residence and family size. To initially qualify for IBR and to continue making income-based payments under this plan, you must have a partial financial hardship (see definition).

The Income-Contingent Repayment (ICR) plan is a repayment plan with monthly payments that are the lesser of (1) what you would pay on a 12-year standard repayment plan multiplied by an income percentage factor or (2) 20 percent of your discretionary income divided by 12. Discretionary income for this plan is the difference between your adjusted gross income and the poverty guideline amount for your state of residence and family size.

You are a new borrower for the Pay As You Earn plan if (1) you have no outstanding balance on a Direct Loan or FFEL Program loan as of October 1, 2007 or have no outstanding balance on a Direct Loan or FFEL Program loan when you obtain a new loan on or after October 1, 2007, and (2) you receive a disbursement of a Direct Subsidized Loan, Direct Unsubsidized Loan, or student Direct PLUS Loan on or after October 1, 2011, or you receive a Direct Consolidation Loan based on an application received on or after October 1, 2011. However, you are not considered a new borrower if the Direct Consolidation Loan you receive repays loans that would make you ineligible under part (1) of this definition.

A partial financial hardship is an eligibility requirement for the IBR and Pay As You Earn plans.

For IBR, you have a partial financial hardship when the annual amount due on all of your eligible loans or, if you are married and file a joint federal income tax return, the annual amount due on all of your eligible loans and your spouse’s eligible loans, exceeds 15 percent of the difference between your adjusted gross income (AGI), as shown on your most recently filed federal income tax return, and 150 percent of the annual poverty guideline amount for your family size and state of residence: Annual amount of payments due > 15% [AGI – (150% x applicable poverty guideline amount)].

For Pay As You Earn, you have a partial financial hardship when the annual amount due on all of your eligible loans or, if you are married and file a joint federal income tax return, the annual amount due on all of your eligible loans and your spouse’s eligible loans, exceeds 10 percent of the difference between your adjusted gross income (AGI), as shown on your most recently filed federal income tax return, and 150 percent of the annual poverty guideline amount for your family size and state of residence: Annual amount of payments due > 10% [AGI – (150% x applicable poverty guideline amount)].

Page 3 of 5

SECTION 8: DEFINITIONS (CONTINUED)

For both plans, the annual amount of payments due is calculated based on the greater of (1) the total amount owed on eligible loans at the time those loans initially entered repayment, or (2) the total amount owed on eligible loans at the time you initially request the IBR or Pay As You Earn plan. The annual amount of payments due is calculated using a standard repayment plan with a 10-year repayment period, regardless as to loan type.

If you are married and file a joint federal income tax return, your AGI includes your spouse’s income.

The Pay As You Earn plan is a repayment plan with monthly payments that are limited to 10 percent of your discretionary income divided by 12. Discretionary income for this plan is the difference between your adjusted gross income and 150 percent of the poverty guideline amount for your state of residence and family size. To initially qualify for the Pay As You Earn plan and to continue to make income-based payments under this plan, you must have a partial financial hardship (see definition) and be a new borrower (see definition).

The poverty guideline amount is the figure for your state and family size from the poverty guidelines published annually by the U.S. Department of Health and Human Services (HHS). The HHS poverty guidelines are used for purposes such as determining eligibility for certain federal benefit programs. If you are not a resident of a state identified in the poverty guidelines, your poverty guideline amount is the amount used for the 48 contiguous states.

The standard repayment plan has a fixed monthly amount over a repayment period of up to 10 years for loans other than Direct or Federal Consolidation Loans, or up to 30 years for Direct and Federal Consolidation Loans.

SECTION 9: ELIGIBILITY REQUIREMENTS

INFORMATION ABOUT THE PAY AS YOU EARN AND IBR PLANS:

To initially qualify to repay your loan(s) under the IBR or Pay As You Earn plan and to continue to qualify to make payments based on your income, you must have a partial financial hardship (as defined in Section 8). If you are married and file a joint federal income tax return, your loan holder(s) will also take your spouse’s income and eligible loans into account when determining whether you have a partial financial hardship.

For the Pay As You Earn plan, you must be a new borrower as defined in Section 8. Although the Pay As You Earn plan is available only for Direct Loan Program loans, your loan holder(s) will take any FFEL Program loans that you have into account when determining whether you have a partial financial hardship except for: (1) a FFEL Program loan that is in default, (2) a Federal PLUS Loan made to a parent borrower, or (3) a Federal Consolidation Loan that repaid a Federal or Direct PLUS Loan made to a parent borrower.

After entry into the IBR or Pay As You Earn plan, you must annually certify your family size and provide income documentation for determination of whether you continue to have a partial financial hardship. Your loan holder(s) will notify you of the deadline by which you are required to provide this documentation. Your monthly payment amount may be adjusted annually. The new payment amount may be higher or lower, depending on the income documentation and family size information you provide each year.

You will never pay more per month than you would on the 10-year standard repayment plan, based upon the amount owed on your eligible loans at the time you initially entered the IBR or Pay As You Earn plan. If you do not provide updated income documentation annually, within 10 days of the deadline provided by your loan holder, after requested to do so by your loan holder, your payment amount will be the 10-year standard payment amount calculated at the time that you initially entered the IBR or Pay As You Earn plan and any outstanding interest will be capitalized (added to your principal balance).Under the IBR or Pay As You Earn plan, your monthly payment may be less than the monthly accruing interest. On subsidized loans, you are not required to pay any monthly accrued interest that exceeds your monthly payment amount for a maximum of three consecutive years from the date that you start repaying your loans under the IBR or Pay As You Earn plan. The three-year consecutive period limit does not include any period during which you receive an Economic Hardship Deferment. On unsubsidized loans, all accruing interest is your responsibility.

If you are determined to no longer have a partial financial hardship or leave the IBR or Pay As You Earn plan, any unpaid interest will be capitalized (added to your principal balance). However, if you are in the Pay As You Earn plan, the amount that is capitalized is limited to 10 percent of the outstanding principal balance on your loans at the time that you entered the Pay As You Earn plan.

If you leave the IBR plan, your payment amount will be the standard payment amount calculated based on the outstanding balance of your eligible loans at the time you leave the IBR plan and the repayment period remaining for your loans. If you wish to repay your loans under a different repayment plan, you must first make one payment under the standard repayment plan or make a reduced payment under a forbearance agreement while on the standard repayment plan with your loan holder(s).

Under the IBR plan, if your loan(s) is not repaid in full after you have made the equivalent of 25 years of qualifying monthly payments and at least 25 years have elapsed, any remaining debt will be forgiven. If you receive an Economic Hardship Deferment, any months of Economic Hardship Deferment are considered the equivalent of qualifying payments. Months for which you receive any other type of deferment or months of forbearance are not counted as qualifying payments, and do not count toward the 25-year forgiveness period. Any amount forgiven under the IBR plan may be considered income by the Internal Revenue Service and subject to federal income tax. The Public Service Loan Forgiveness Program allows eligible borrowers to cancel the remaining balance of their Direct Loans after they have served full time at a public service organization for at least 10 years, while making 120 qualifying loan payments, including payments under the IBR plan. For more information, see studentaid.gov/publicservice.

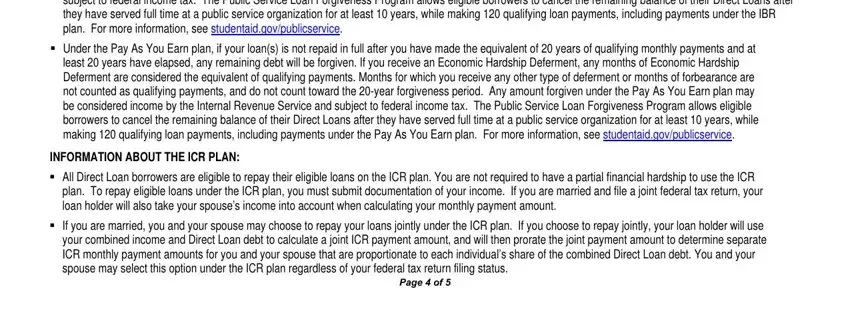

Under the Pay As You Earn plan, if your loan(s) is not repaid in full after you have made the equivalent of 20 years of qualifying monthly payments and at least 20 years have elapsed, any remaining debt will be forgiven. If you receive an Economic Hardship Deferment, any months of Economic Hardship Deferment are considered the equivalent of qualifying payments. Months for which you receive any other type of deferment or months of forbearance are not counted as qualifying payments, and do not count toward the 20-year forgiveness period. Any amount forgiven under the Pay As You Earn plan may be considered income by the Internal Revenue Service and subject to federal income tax. The Public Service Loan Forgiveness Program allows eligible borrowers to cancel the remaining balance of their Direct Loans after they have served full time at a public service organization for at least 10 years, while making 120 qualifying loan payments, including payments under the Pay As You Earn plan. For more information, see studentaid.gov/publicservice.

INFORMATION ABOUT THE ICR PLAN:

All Direct Loan borrowers are eligible to repay their eligible loans on the ICR plan. You are not required to have a partial financial hardship to use the ICR plan. To repay eligible loans under the ICR plan, you must submit documentation of your income. If you are married and file a joint federal tax return, your loan holder will also take your spouse’s income into account when calculating your monthly payment amount.

If you are married, you and your spouse may choose to repay your loans jointly under the ICR plan. If you choose to repay jointly, your loan holder will use your combined income and Direct Loan debt to calculate a joint ICR payment amount, and will then prorate the joint payment amount to determine separate ICR monthly payment amounts for you and your spouse that are proportionate to each individual’s share of the combined Direct Loan debt. You and your spouse may select this option under the ICR plan regardless of your federal tax return filing status.

SECTION 9: ELIGIBILITY REQUIREMENTS (CONTINUED)

After entry into the ICR plan, you must annually certify your family size and provide income documentation so that your loan holder can adjust your payment amount to reflect more recent income information. Your new payment amount may be higher or lower, depending on the income documentation and family size information you provide each year. Your loan holder will notify you when you are required to provide this documentation.

If you do not provide updated income documentation annually by the deadline provided by your loan holder(s), your payment amount will be calculated based on a 10-year standard repayment plan using the loan balance at the time you entered repayment under the ICR repayment plan.

Under the ICR plan, your monthly payment may be less than the monthly accruing interest. The accruing interest that is not satisfied by your monthly payment will be capitalized annually. You will receive a notice telling you when the interest will be capitalized, and you will have the opportunity to pay that interest before it is capitalized. While you remain in ICR, the amount of interest that is capitalized will be limited to 10 percent of the outstanding principal balance on your loans at the time that you entered repayment.

Under the ICR plan, if your loan(s) is not repaid in full after you have made the equivalent of 25 years of qualifying monthly payments and at least 25 years have elapsed, any remaining debt will be forgiven. If you receive an Economic Hardship Deferment, any months of Economic Hardship Deferment are considered the equivalent of qualifying payments. Months for which you receive any other type of deferment or months of forbearance are not counted as qualifying payments, and do not count toward the 25-year forgiveness period. Any amount forgiven under the ICR plan may be considered income by the Internal Revenue Service and subject to federal income tax. The Public Service Loan Forgiveness Program allows eligible borrowers to cancel the remaining balance of their Direct Loans after they have served full time at a public service organization for at least 10 years, while making 120 qualifying loan payments, including payments under the ICR plan. For more information, see studentaid.gov/publicservice.

IMPORTANT INFORMATION ABOUT ALTERNATIVE DOCUMENTATION OF INCOME

YOU ARE REQUIRED to provide alternative documentation of your income if:

OYou did not file a federal tax return for the either of the two most recently completed tax years; or

OYou have been notified by your loan holder(s) that alternative documentation of your income is required.

YOU MAY provide alternative documentation of your income if your Adjusted Gross Income (AGI), as reported on your most recently filed federal tax return, does not reasonably reflect your current income, because, for example, of a loss of or change in employment by you or your spouse.

YOU ARE NOT REQUIRED to provide alternative documentation of your income if you can provide a copy of your most recently filed federal tax return or an IRS tax return transcript from either of the two most recently completed tax years; and that documentation reasonably reflects your current income.

SECTION 10: WHERE TO SEND THE COMPLETED REPAYMENT PLAN REQUEST

Return the completed form and any required documentation to:

If you need help completing this form, call:

If no address is shown, return to your loan holder(s).

If no telephone number is shown, call your loan holder(s).

SECTION 11: IMPORTANT NOTICES

Privacy Act Notice. The Privacy Act of 1974 (5 U.S.C. 552a) requires that the following notice be provided to you:

The authorities for collecting the requested information from and about you are §421 et seq. and §451 et seq. of the Higher Education Act of 1965, as amended (20 U.S.C. 1071 et seq. and 20 U.S.C. 1087a et seq.) and the authorities for collecting and using your Social Security Number (SSN) are §§428B(f) and 484(a)(4) of the HEA (20 U.S.C. 1078-2(f) and 1091(a)(4)) and 31 U.S.C. 7701(b). Participating in the Federal Family Education Loan (FFEL) Program or the William D. Ford Federal Direct Loan (Direct Loan) Program and giving us your SSN are voluntary, but you must provide the requested information, including your SSN, to participate.

The principal purposes for collecting the information on this form, including your SSN, are to verify your identity, to determine your eligibility to receive a loan or a benefit on a loan (such as a deferment, forbearance, discharge, or forgiveness) under the FFEL and/or Direct Loan Programs, to permit the servicing of your loan(s), and, if it becomes necessary, to locate you and to collect and report on your loan(s) if your loan(s) becomes delinquent or defaults. We also use your SSN as an account identifier and to permit you to access your account information electronically.

The information in your file may be disclosed, on a case-by-case basis or under a computer matching program, to third parties as authorized under routine uses in the appropriate systems of records notices. The routine uses of this information include, but are not limited to, its disclosure to federal, state, or local agencies, to private parties such as relatives, present and former employers, business and personal associates, to consumer reporting agencies, to financial and educational institutions, and to guaranty agencies in order to verify your identity, to determine your eligibility to receive a loan or a benefit on a loan, to permit the servicing or collection of your loan(s), to enforce the terms of the loan(s), to investigate possible fraud and to verify compliance with federal student financial aid program regulations, or to locate you if you become delinquent in your loan payments or if you default. To provide default rate calculations, disclosures may be made to guaranty agencies, to financial and educational institutions, or to state agencies. To provide financial aid history information, disclosures may be made to educational institutions. To assist program administrators with tracking refunds and cancellations, disclosures may be made to guaranty agencies, to financial and educational institutions, or to federal or state agencies. To provide a standardized method for educational institutions to efficiently submit student enrollment statuses, disclosures may be made to guaranty agencies or to financial and educational institutions. To counsel you in repayment efforts, disclosures may be made to guaranty agencies, to financial and educational institutions, or to federal, state, or local agencies.

In the event of litigation, we may send records to the Department of Justice, a court, adjudicative body, counsel, party, or witness if the disclosure is relevant and necessary to the litigation. If this information, either alone or with other information, indicates a potential violation of law, we may send it to the appropriate authority for action. We may send information to members of Congress if you ask them to help you with federal student aid questions. In circumstances involving employment complaints, grievances, or disciplinary actions, we may disclose relevant records to adjudicate or investigate the issues. If provided for by a collective bargaining agreement, we may disclose records to a labor organization recognized under 5 U.S.C. Chapter 71. Disclosures may be made to our contractors for the purpose of performing any programmatic function that requires disclosure of records. Before making any such disclosure, we will require the contractor to maintain Privacy Act safeguards. Disclosures may also be made to qualified researchers under Privacy Act safeguards.

Paperwork Reduction Notice. According to the Paperwork Reduction Act of 1995, no persons are required to respond to a collection of information unless it displays a currently valid OMB control number. Public reporting burden for this collection of information is estimated to average 0.5 hours (30 minutes) per response, including the time for reviewing instructions, searching existing data resources, gathering and maintaining the data needed, and completing and reviewing the information collection. Individuals are obligated to respond to this collection to obtain a benefit in accordance with 34 CFR 682.215, 685.209, or 685.221. Send comments regarding the burden estimate(s) or any other aspect of this collection of information, including suggestions for reducing this burden to the U.S. Department of Education, 400 Maryland Avenue, SW, Washington, DC 20210-4537 or e-mail ICDocketMgr@ed.gov and reference OMB Control Number 1845-0102.

Note: Please do not return the completed form to this address. If you have questions regarding the status of your individual submission of this form, contact your loan holder(s) (see Section 10).

IBR - Request to End Deferment/Forbearance

Federal Family Education Loan Program

BORROWER NAME: ____________________________________________

ACCOUNT NUMBER: ________________________________

I am requesting to have my deferment/forbearance terminated on my eligible loan(s) for the purpose of allowing AES to process my Income Based Repayment plan request.

I understand that I am only requesting the termination of my current deferment/forbearance if I qualify for the Income Based Repayment plan. I also understand that if my current deferment / forbearance is ended, any unpaid accrued interest will be capitalized (added to the balance) and my loan(s) will be placed into repayment on the Income Based Repayment plan.

__________________________________________ |

__________________ |

Borrower's Signature |

Date |