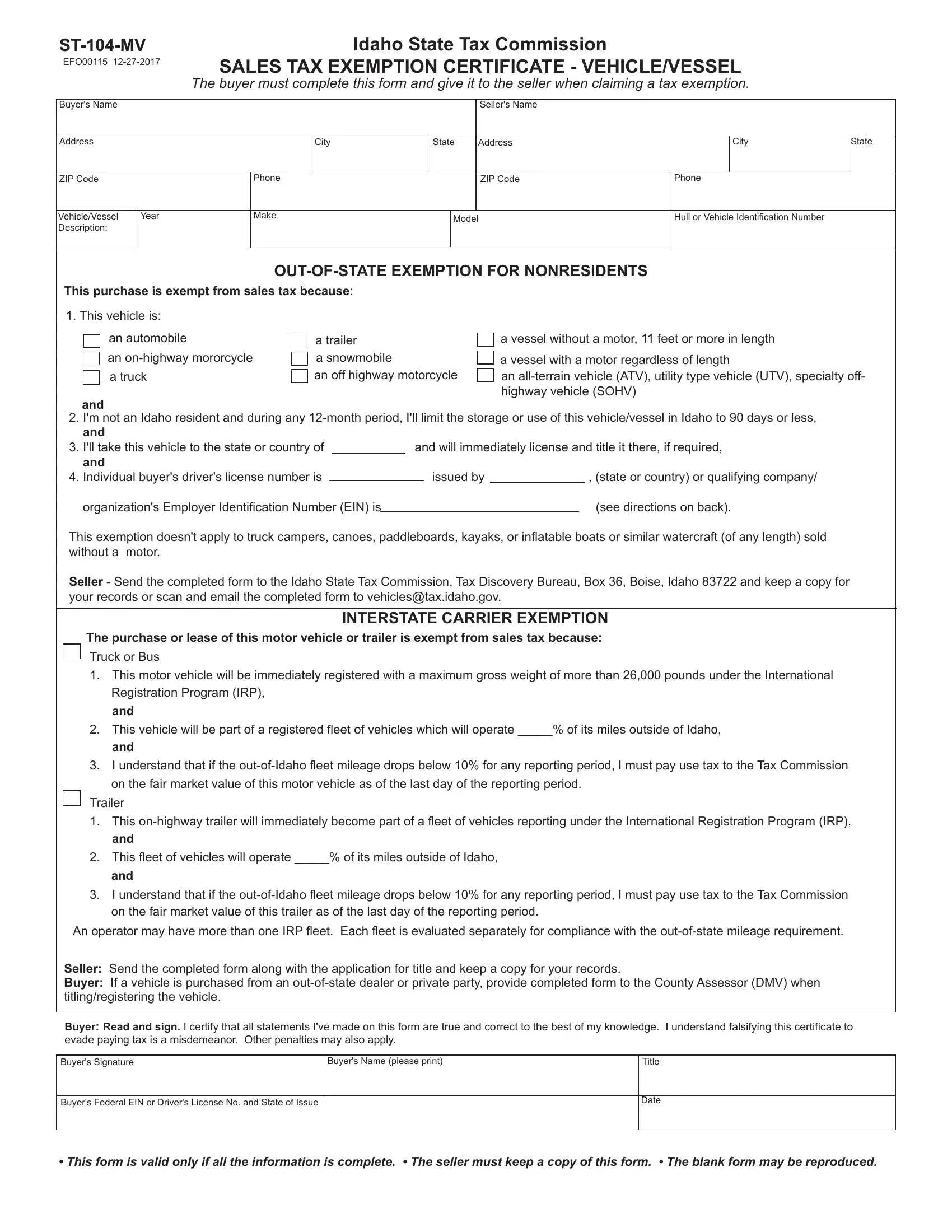

The Idaho ST-104-MV form is a critical document for buyers and sellers engaged in vehicle and vessel transactions within the state, playing a pivotal role in the eligibility and processing of sales tax exemptions. This Sales Tax Exemption Certificate is meticulously designed to facilitate two primary exemptions: one for out-of-state nonresidents and another for interstate carriers. Nonresidents can leverage this form to assert their exemption from Idaho sales tax, provided the vehicle or vessel is intended for immediate use outside Idaho, will not be used or stored within Idaho for more than 90 days annually, and will be registered and titled elsewhere if required. However, it's noteworthy that certain watercraft and vehicles without motors, like truck campers and kayaks, do not qualify under this exemption. On the other hand, the interstate carrier exemption applies to vehicles that will be registered under the International Registration Program with a gross weight exceeding 26,000 pounds, assuming they operate a significant portion of their mileage outside Idaho. This form necessitates comprehensive completion and submission procedures for both buyers and sellers, including forwarding a copy to the Idaho State Tax Commission and keeping a record for verification purposes. Strict compliance and the accuracy of information are imperative, as any intent to furnish false information to evade tax constitutes a misdemeanor, with additional penalties possibly ensuing.

| Question | Answer |

|---|---|

| Form Name | Idaho Form ST-104-MV |

| Form Length | 2 pages |

| Fillable? | Yes |

| Fillable fields | 36 |

| Avg. time to fill out | 7 min 46 sec |

| Other names | id 104 vehicle form, idaho st mv sales tax form, st 104, idaho st 104 mv tax |

|

|

|

|

|

Idaho State Tax Commission |

|

||||||||||||||

EFO00115 |

SALES TAX EXEMPTION CERTIFICATE - VEHICLE/VESSEL |

|

||||||||||||||||||

|

|

|

|

|||||||||||||||||

|

|

|

The buyer must complete this form and give it to the seller when claiming a tax exemption. |

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Buyer's Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

Seller's Name |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

City |

|

|

State |

Address |

|

|

City |

State |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ZIP Code |

|

|

|

|

Phone |

|

|

|

|

ZIP Code |

|

Phone |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vehicle/Vessel |

|

Year |

|

|

Make |

|

|

|

Model |

|

Hull or Vehicle Identification Number |

|

||||||||

Description: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|||||||||||||||

This purchase is exempt from sales tax because: |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

1. This vehicle is: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

an automobile |

|

|

|

a trailer |

|

|

|

|

|

a vessel without a motor, 11 feet or more in length |

|

|||||||||

an |

|

a snowmobile |

|

|

|

|

|

a vessel with a motor regardless of length |

|

|||||||||||

a truck |

|

|

|

an off highway motorcycle |

|

an |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

highway vehicle (SOHV) |

|

||||

and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. I'm not an Idaho resident and during any |

|

|||||||||||||||||||

and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. I'll take this vehicle to the state or country of |

and will immediately license and title it there, if required, |

|

||||||||||||||||||

and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. Individual buyer's driver's license number is |

|

|

|

|

issued by |

, (state or country) or qualifying company/ |

|

|||||||||||||

organization's Employer Identifi cation Number (EIN) is |

|

|

|

|

|

|

|

|

(see directions on back). |

|

||||||||||

This exemption doesn't apply to truck campers, canoes, paddleboards, kayaks, or infl atable boats or similar watercraft (of any length) sold |

|

|||||||||||||||||||

without a |

motor. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Seller - Send the completed form to the Idaho State Tax Commission, Tax Discovery Bureau, Box 36, Boise, Idaho 83722 and keep a copy for your records or scan and email the completed form to vehicles@tax.idaho.gov.

INTERSTATE CARRIER EXEMPTION

The purchase or lease of this motor vehicle or trailer is exempt from sales tax because:

Truck or Bus

1.This motor vehicle will be immediately registered with a maximum gross weight of more than 26,000 pounds under the International Registration Program (IRP),

and

2.This vehicle will be part of a registered fl eet of vehicles which will operate _____% of its miles outside of Idaho, and

3.I understand that if the

Trailer

1.This

2.This fl eet of vehicles will operate _____% of its miles outside of Idaho, and

3.I understand that if the

An operator may have more than one IRP fl eet. Each fl eet is evaluated separately for compliance with the

Seller: Send the completed form along with the application for title and keep a copy for your records.

Buyer: If a vehicle is purchased from an

Buyer: Read and sign. I certify that all statements I've made on this form are true and correct to the best of my knowledge. I understand falsifying this certificate to evade paying tax is a misdemeanor. Other penalties may also apply.

Buyer's Signature

Buyer's Name (please print)

Title

Buyer's Federal EIN or Driver's License No. and State of Issue

Date

• This form is valid only if all the information is complete. • The seller must keep a copy of this form. • The blank form may be reproduced.

Instructions for Form

(Idaho Code Section

When a vehicle or vessel is bought by a nonresident for use outside Idaho, it may qualify for an exemption from Idaho sales tax. Truck campers, canoes, paddleboards, kayaks, infl atable boats, or similar watercraft (of any length) sold without a motor don't qualify for this exemption.

To claim an exemption the buyer must complete a Form

•Will immediately be taken out of Idaho and titled and registered in another state or country (if required), and

•Won't be stored or used in Idaho for more than 90 days in any

Idaho residents can't claim this exemption.

A company/organization qualifi es for this exemption only if it meets all three of the following criteria:

•It's a corporation, partnership, limited liability company, or other organization that isn't formed under the laws of Idaho,

and

•It's not required to be registered with the Idaho Secretary of State to do business in Idaho,

and

•It doesn't have signifi cant contacts and consistent operations in Idaho.

INTERSTATE CARRIER EXEMPTION

Sales of motor vehicles for use in interstate commerce are exempt if:

•The vehicle will be immediately registered with a maximum gross registered weight of more than 26,000 pounds under the International Registration Plan,

and

•At least 10% of the purchaser's total fl eet mileage is outside of Idaho.

The buyer must complete Form

The exemption applies only to purchases of trucks, buses, and trailers, but not their repair or maintenance. However, the sale of a "glider kit" isn't taxable when used to assemble a glider kit vehicle that will be registered in an IRP fl eet and will meet the weight and mileage requirements listed above.

Rule 128 states that if you don't receive an exemption certifi cate from the buyer at the time of sale, the sale is presumed to be taxable. If you receive an exemption certifi cate after the sale, but don't get it within a reasonable length of time, the Tax Commission will review the certifi cate with all other avail- able evidence to determine whether you have clearly proven that the sale was exempt from tax.

EFO00115