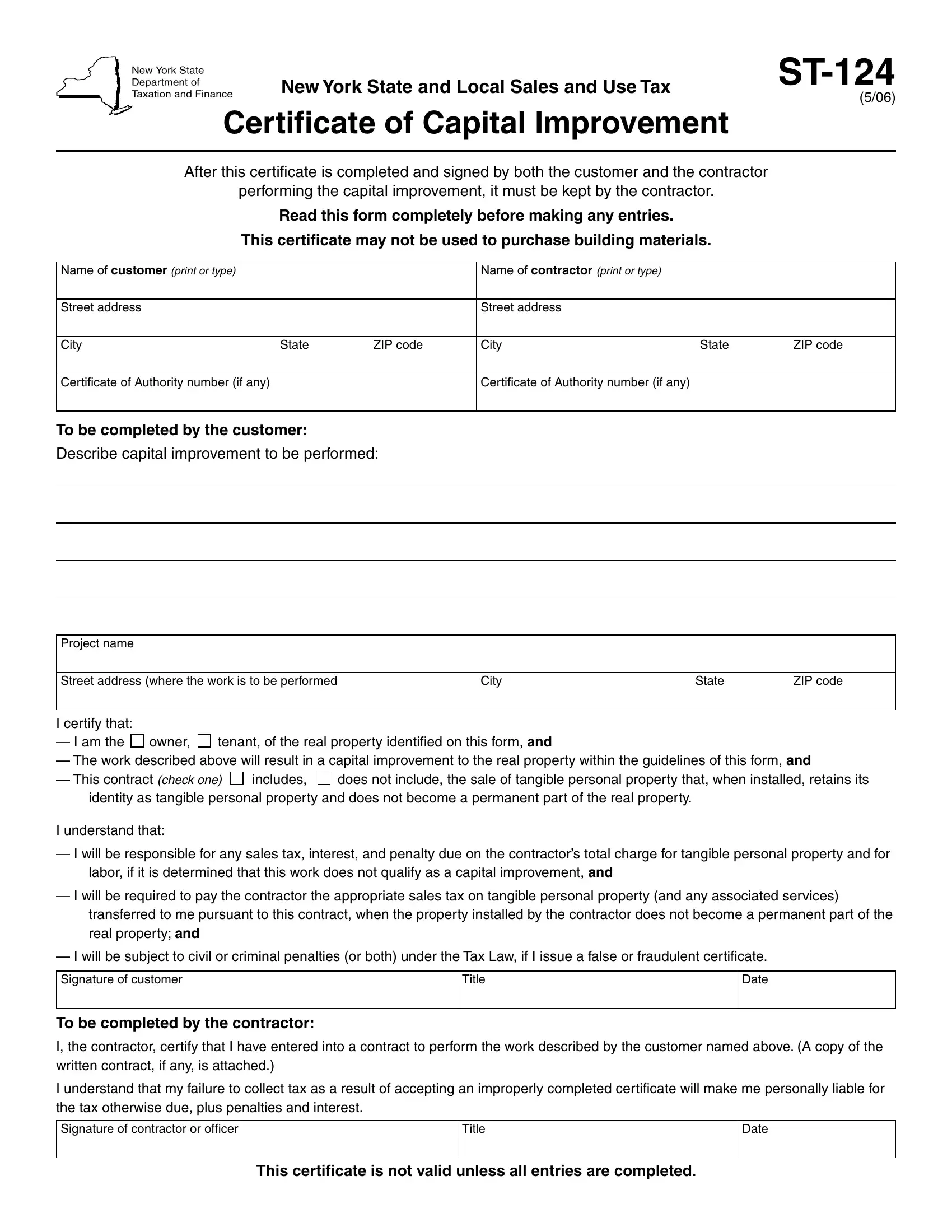

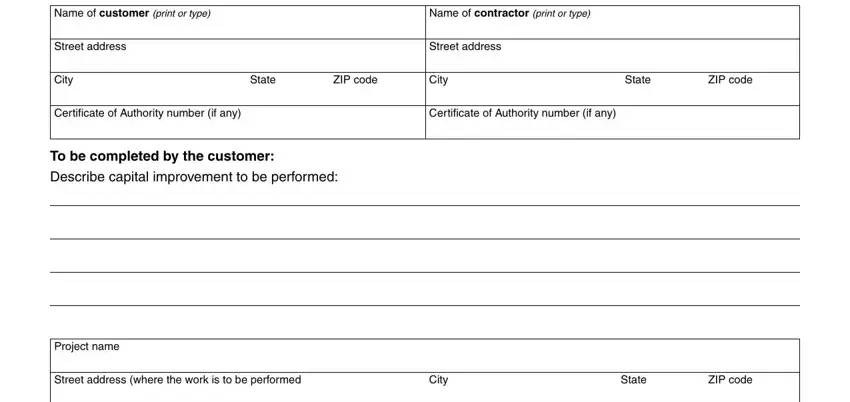

If a contractor gets a properly completed (that is, no required entries on the form are left blank) Form ST-124, Certificate of Capital Improvement, from the customer within 90 days after rendering services, the customer bears the burden of proving the job or transaction was a capital improvement (that is, was not taxable to the customer).

If a contractor does not get a properly completed Certificate of Capital Improvement within 90 days, the contractor bears the burden of proving the work or transaction was a capital improvement. The failure to get a properly completed certificate, however, does not change the taxable status of a transaction; that is, a contractor may still show that the transaction was a capital improvement. If a contractor erects a building for a customer, or performs some other work that constitutes a capital improvement, the contractor must pay tax on the purchase of building materials or other tangible personal property, but is not required to collect tax from the customer for the capital improvement. If the work performed is taxable (such as repair, service, or maintenance), the contractor must collect tax from the customer on the full charge to the customer, including labor and materials.

The contractor must keep any exemption certificate for at least three years after the due date of the last return to which it relates, or the date the return was filed, if later. The contractor must also maintain a method of associating an exempt sale made to a particular customer with the exemption certificate on file for that customer.

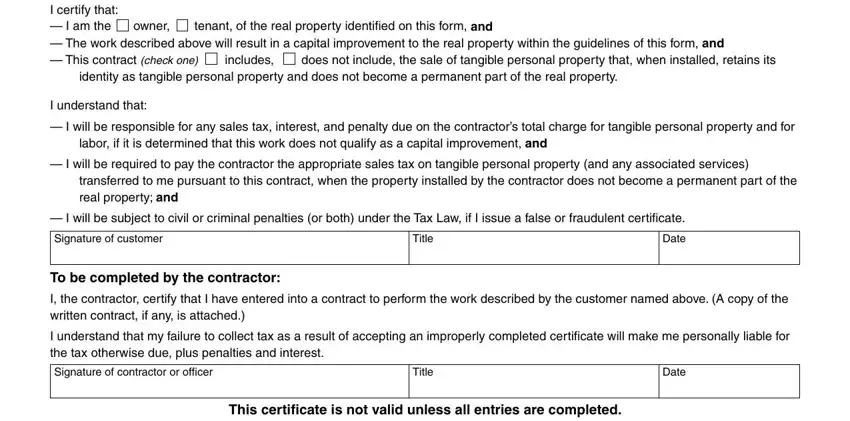

When the customer completes this certificate and gives it to the contractor, it is evidence that the work to be performed will result in a capital improvement to real property.

A capital improvement to real property is defined in

section 1101 (b)(9) of the Tax Law and Sales Tax Regulation section 527.7(a)(3), as an addition or alteration to real property that:

(a)substantially adds to the value of the real property or appreciably prolongs the useful life of the real property,

and

(b)becomes part of the real property or is permanently affixed to the real property so that removal would cause material damage to the property or article itself,

and

(c) is intended to become a permanent installation.

The work performed by the contractor must meet all three of these requirements to be considered a capital improvement. This certificate may not be issued unless the work qualifies as a capital improvement.

A contractor, subcontractor, property owner, or tenant, may not use this certificate to purchase building materials or other tangible personal property tax free. A contractor’s acceptance of this certificate does not relieve the contractor of the liability

for sales tax. A contractor must pay sales tax on the purchase of building materials or other tangible personal property subsequently incorporated into the real property as a capital improvement (see Publication 862, Sales and Use Tax Classifications of Capital Improvements and Repairs to Real Property, for additional information) unless the contractor can legally issue Form ST-120.1, Contractor Exempt Purchase Certificate.

The term materials is defined as items that become a physical component part of real or personal property, such as lumber, bricks, or steel (Sales Tax Regulation, section 541.2(i)).

This term also includes items such as doors, windows, kits, and prefabricated buildings used in construction.

Floor covering

Floor covering such as carpet, carpet padding, linoleum and vinyl roll flooring, carpet tile, linoleum tile, and vinyl tile installed as the initial finished floor covering in (1) new construction, (2) a new addition to an existing building or structure, or (3) in a total reconstruction of an existing building or structure, constitutes a capital improvement regardless of the method of installation. As a capital improvement, the charge to the property owner for the installation of floor covering is not subject to New York State and local sales and use taxes. However, the retail purchase of floor covering (such as carpet or padding) itself is subject to tax.

Floor covering installed other than as described in the preceding paragraph does not qualify as a capital improvement, even though it meets the criteria stated in (a), (b), and (c). Therefore, the charge for materials and labor is subject to the sales tax, regardless of the manner in which the covering is installed (see Publication 864.1, Floor Coverings and the Sales Tax Law, for additional information), but the contractor may apply for a credit or refund of any sales tax already paid on the materials.

The term floor covering does not include flooring such as ceramic tile, hardwood, slate, terrazzo, and marble. Thus, the rules for determining when floor covering constitutes a capital improvement do not apply to such flooring. Rather, the criteria stated in (a), (b), and (c) above apply to the flooring.

For guidance as to whether a job is a repair or a capital improvement, refer to Publication 862, Sales and Use Tax Classifications of Capital Improvements and Repairs to Real Property.

Need help?

Internet access: www.nystax.gov

(for information, forms, and publications)

Fax-on-demand forms: |

1 800 748-3676 |

Telephone assistance is available from 8:00 A.M. to 5:00 P.M. (eastern time), Monday through Friday.

To order forms and publications: |

1 800 |

462-8100 |

Sales Tax Information Center: |

1 800 |

698-2909 |

From areas outside the U.S. and outside Canada: |

(518) |

485-6800 |

Hearing and speech impaired (telecommunications |

|

|

device for the deaf (TDD) callers only): |

1 800 |

634-2110 |

Persons with disabilities: In compliance with the

Americans with Disabilities Act, we will ensure that our lobbies, offices, meeting rooms, and other facilities are accessible to

persons with disabilities. If you have questions about special accommodations for persons with disabilities, please call 1 800 972-1233.