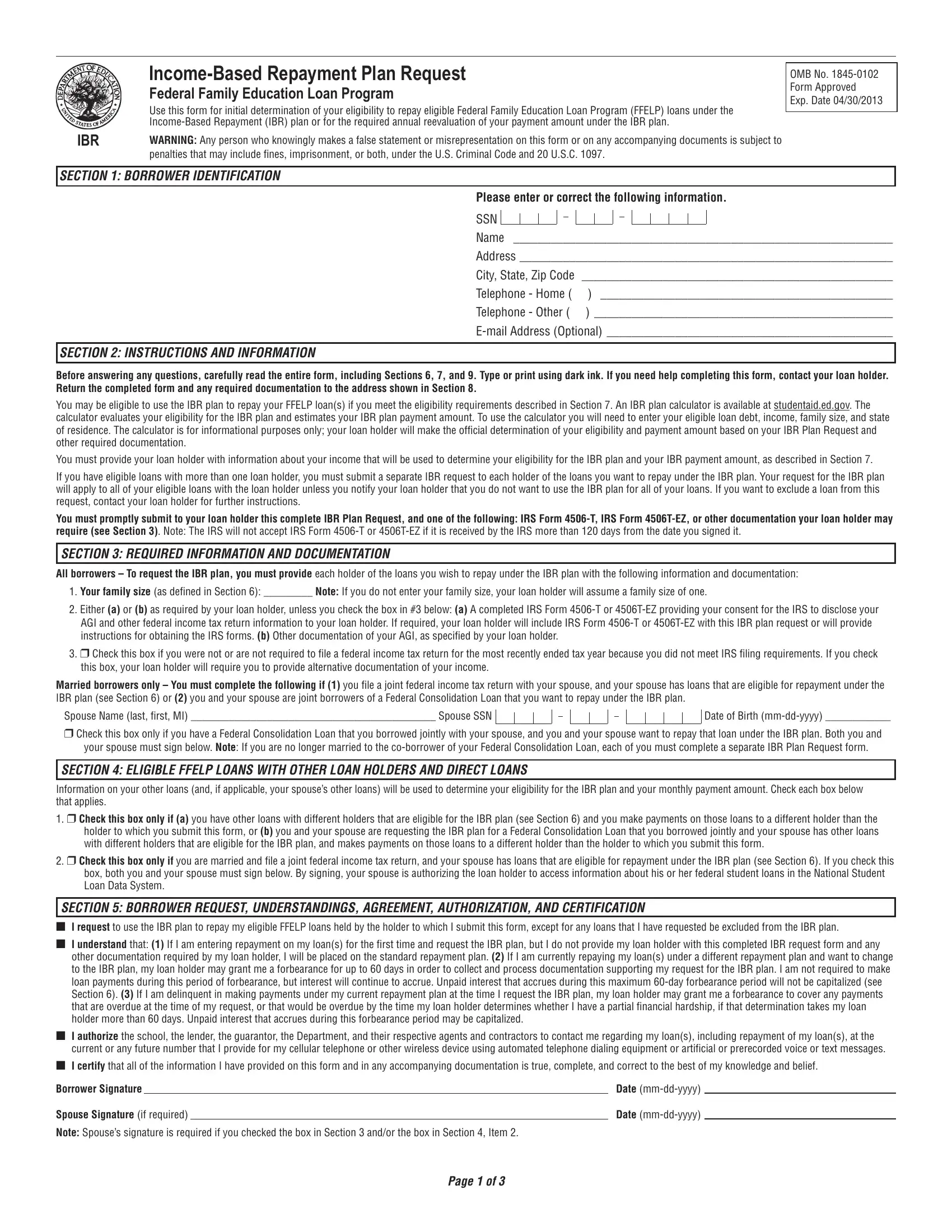

For those navigating the complexities of repaying federal student loans, the Income Based Repayment Plan Request form serves as a crucial tool. Designed for borrowers under the Federal Family Education Loan Program (FFELP), this form enables individuals to apply for an income-based repayment plan or to obtain a required annual reevaluation of their payment amount. The form underscores the serious legal implications of providing false information, emphasizing its significance in the loan repayment process. Key elements include borrower identification, detailed instructions, necessary documentation, and criteria for eligibility, each carefully outlined to guide borrowers through the application process. Additionally, it incorporates provisions for married borrowers, considerations for loans with other holders, and a comprehensive definition section, all aimed at ensuring a smooth transition to an income-based repayment plan. Borrowers are urged to carefully provide accurate information about their income, as this directly influences eligibility and payment calculations, a process further supported by an available IBR plan calculator. The emphasis on annual recertification illustrates the program's adaptability to changing financial circumstances, offering a reimbursement strategy rooted in current income levels. This form not only facilitates entry into the IBR plan but also outlines obligations, including the potential for loan forgiveness after 25 years of qualifying payments, fundamentally aiming to make loan repayment more manageable based on the borrower's financial situation.

| Question | Answer |

|---|---|

| Form Name | Income Based Repayment Plan Request Form |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | nelnet ibr form, nelnet income based repayment form, nelnet income based repayment form pdf, nelnet income based repayment application |

|

|

|

Federal Family Education Loan Program |

|

Use this form for initial determination of your eligibility to repay eligible Federal Family Education Loan Program (FFELP) loans under the |

|

|

IBR |

WARNING: Any person who knowingly makes a false statement or misrepresentation on this form or on any accompanying documents is subject to |

|

penalties that may include ines, imprisonment, or both, under the U.S. Criminal Code and 20 U.S.C. 1097. |

OMB No.

Form Approved

Exp. Date 04/30/2013

SECTION 1: BORROWER IDENTIFICATION

Please enter or correct the following information.

SSN

Name _____________________________________________________________

Address ____________________________________________________________

City, State, Zip Code __________________________________________________

Telephone - Home ( ) _______________________________________________

Telephone - Other ( ) ________________________________________________

SECTION 2: INSTRUCTIONS AND INFORMATION

Before answering any questions, carefully read the entire form, including Sections 6, 7, and 9. Type or print using dark ink. If you need help completing this form, contact your loan holder. Return the completed form and any required documentation to the address shown in Section 8.

You may be eligible to use the IBR plan to repay your FFELP loan(s) if you meet the eligibility requirements described in Section 7. An IBR plan calculator is available at studentaid.ed.gov. The calculator evaluates your eligibility for the IBR plan and estimates your IBR plan payment amount. To use the calculator you will need to enter your eligible loan debt, income, family size, and state of residence. The calculator is for informational purposes only; your loan holder will make the oficial determination of your eligibility and payment amount based on your IBR Plan Request and other required documentation.

You must provide your loan holder with information about your income that will be used to determine your eligibility for the IBR plan and your IBR payment amount, as described in Section 7.

If you have eligible loans with more than one loan holder, you must submit a separate IBR request to each holder of the loans you want to repay under the IBR plan. Your request for the IBR plan will apply to all of your eligible loans with the loan holder unless you notify your loan holder that you do not want to use the IBR plan for all of your loans. If you want to exclude a loan from this request, contact your loan holder for further instructions.

You must promptly submit to your loan holder this complete IBR Plan Request, and one of the following: IRS Form

require (see Section 3). Note: The IRS will not accept IRS Form

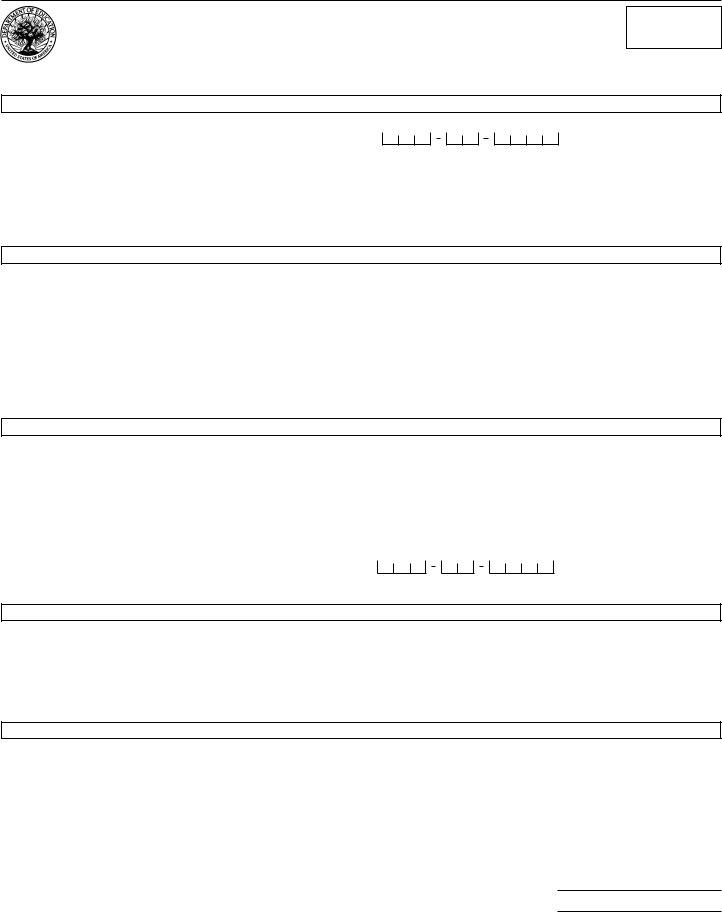

SECTION 3: REQUIRED INFORMATION AND DOCUMENTATION

All borrowers – To request the IBR plan, you must provide each holder of the loans you wish to repay under the IBR plan with the following information and documentation:

1.Your family size (as deined in Section 6): _________ Note: If you do not enter your family size, your loan holder will assume a family size of one.

2.Either (a) or (b) as required by your loan holder, unless you check the box in #3 below: (a) A completed IRS Form

3.r Check this box if you were not or are not required to ile a federal income tax return for the most recently ended tax year because you did not meet IRS iling requirements. If you check this box, your loan holder will require you to provide alternative documentation of your income.

Married borrowers only – You must complete the following if (1) you ile a joint federal income tax return with your spouse, and your spouse has loans that are eligible for repayment under the IBR plan (see Section 6) or (2) you and your spouse are joint borrowers of a Federal Consolidation Loan that you want to repay under the IBR plan.

Spouse Name (last, irst, MI) _____________________________________________ Spouse SSN

Date of Birth

r Check this box only if you have a Federal Consolidation Loan that you borrowed jointly with your spouse, and you and your spouse want to repay that loan under the IBR plan. Both you and your spouse must sign below. Note: If you are no longer married to the

SECTION 4: ELIGIBLE FFELP LOANS WITH OTHER LOAN HOLDERS AND DIRECT LOANS

Information on your other loans (and, if applicable, your spouse’s other loans) will be used to determine your eligibility for the IBR plan and your monthly payment amount. Check each box below that applies.

1.r Check this box only if (a) you have other loans with different holders that are eligible for the IBR plan (see Section 6) and you make payments on those loans to a different holder than the holder to which you submit this form, or (b) you and your spouse are requesting the IBR plan for a Federal Consolidation Loan that you borrowed jointly and your spouse has other loans with different holders that are eligible for the IBR plan, and makes payments on those loans to a different holder than the holder to which you submit this form.

2.r Check this box only if you are married and ile a joint federal income tax return, and your spouse has loans that are eligible for repayment under the IBR plan (see Section 6). If you check this box, both you and your spouse must sign below. By signing, your spouse is authorizing the loan holder to access information about his or her federal student loans in the National Student Loan Data System.

SECTION 5: BORROWER REQUEST, UNDERSTANDINGS, AGREEMENT, AUTHORIZATION, AND CERTIFICATION

nI request to use the IBR plan to repay my eligible FFELP loans held by the holder to which I submit this form, except for any loans that I have requested be excluded from the IBR plan.

nI understand that: (1) If I am entering repayment on my loan(s) for the irst time and request the IBR plan, but I do not provide my loan holder with this completed IBR request form and any other documentation required by my loan holder, I will be placed on the standard repayment plan. (2) If I am currently repaying my loan(s) under a different repayment plan and want to change to the IBR plan, my loan holder may grant me a forbearance for up to 60 days in order to collect and process documentation supporting my request for the IBR plan. I am not required to make loan payments during this period of forbearance, but interest will continue to accrue. Unpaid interest that accrues during this maximum

nI authorize the school, the lender, the guarantor, the Department, and their respective agents and contractors to contact me regarding my loan(s), including repayment of my loan(s), at the current or any future number that I provide for my cellular telephone or other wireless device using automated telephone dialing equipment or artiicial or prerecorded voice or text messages.

nI certify that all of the information I have provided on this form and in any accompanying documentation is true, complete, and correct to the best of my knowledge and belief.

Borrower Signature |

|

Date |

|

Spouse Signature (if required) |

|

Date |

|

Note: Spouse’s signature is required if you checked the box in Section 3 and/or the box in Section 4, Item 2. |

|

||

Page 1 of 3

SECTION 6: DEFINITIONS

n Capitalization is the addition of unpaid interest to the principal balance of your loan. This will increase the principal balance and the total cost of your loan.

n Eligible loans for the IBR plan are FFELP and Direct Loan Program loans other than: (1) a loan that is in default, (2) a Federal or Direct PLUS Loan made to a parent borrower, or (3) a Federal or Direct Consolidation Loan that repaid a Federal or Direct PLUS Loan made to a parent borrower. Federal Perkins Loans, HEAL loans or other health education loans, and private education loans are not eligible for the IBR plan. To access information on all of your federal student loans, check the National Student Loan Data System at www.nslds.ed.gov.

n Family size includes you, your spouse, and your children (including unborn children who will be born during the year for which you certify your family size), if the children will receive more than half their support from you. It includes other people only if they live with you now, they receive more than half their support from you now, and they will continue to receive this support from you for the year that you certify your family size. Support includes money, gifts, loans, housing, food, clothes, car, medical and dental care, and payment of college costs.

n The Federal Family Education Loan Program (FFELP) includes Federal Stafford Loans (both subsidized and unsubsidized), Federal PLUS Loans, Federal Consolidation Loans, and Federal Supplemental Loans for Students (SLS).

n The holder of your FFELP loan(s) may be a lender or the U.S. Department of Education (the Department). The holder of Direct Loan Program loans is the Department. Your loan holder may use a servicer to handle billing and other communications related to your loan(s). If your loan holder uses a servicer, the term “holder” as used throughout this form may also refer to the servicer.

n

n Partial inancial hardship is when the annual amount due on all of your eligible loans or, if you are married and ile a joint federal income tax return, the annual amount due on all of your eligible loans and your spouse’s eligible loans, exceeds 15% of the difference between your adjusted gross income (AGI), as shown on your most recently iled federal income tax return, and 150% of the annual poverty guideline amount for your family size and state of residence:

Annual amount of payments due > 15% [AGI – (150% x applicable poverty guideline amount)]

The annual amount of payments due is calculated based on the greater of (1) the total amount owed on eligible loans at the time those loans initially entered repayment or

(2)the total amount owed on eligible loans at the time you or, if applicable, your spouse requested the IBR plan. The annual amount of payments due is calculated using a standard repayment plan with a

ile a joint federal income tax return, the amount owed on your spouse’s eligible loans. If you are married and ile a joint federal income tax return, your AGI includes your spouse’s income.

n Poverty guideline amount is the igure for your state and family size from the poverty guidelines published annually by the U.S. Department of Health and Human Services (HHS). The HHS poverty guidelines are used for purposes such as determining eligibility for certain federal beneit programs. If you are not a resident of a state identiied in the poverty guidelines, your poverty guideline amount is the amount used for the 48 contiguous states.

n The William D. Ford Federal Direct Loan (Direct Loan) Program includes Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and Direct Consolidation Loans.

SECTION 7: ELIGIBILITY CRITERIA

Important information about the IBR plan includes:

n You may use the IBR plan to repay your eligible FFELP loan(s), as deined in Section 6.

n To initially qualify to repay your loan(s) under the IBR plan and to continue to qualify to make

n You must submit required information about your income to your loan holder for determination of your eligibility for the IBR plan and your IBR payment amount. You must provide your loan holder with Internal Revenue Service (IRS) Form

n When you have a partial inancial hardship, your monthly payment amount under the IBR plan will not exceed 15% of the amount by which your AGI exceeds 150% of the poverty guideline amount for your family size and state of residence, divided by 12:

Monthly payment = 15% [AGI – (150% x applicable poverty guideline amount)] ÷ 12

n After entry into the IBR plan, you must annually certify your family size and provide income documentation for determination of whether you have a partial inancial hardship. Your monthly payment amount for the IBR plan may be adjusted annually. It may be higher or lower, depending on the income documentation and family size information you provide each year. Your loan holder will notify you when you are required to provide this documentation.

n For any year you do not have a partial inancial hardship, your payment amount will be the payment amount for your loan(s) under the standard repayment plan with a

n In some circumstances your IBR plan monthly payment amount may not cover all interest that accrues, and your debt may increase. While you are in repayment under IBR, if your monthly payment amount does not cover all interest that accrues each month, the U.S. Department of Education will pay the unpaid interest on your subsidized Stafford loan(s) and on the subsidized portion of your Federal Consolidation Loan(s) for not more than the irst 3 consecutive years after you initially enter the IBR plan. If you receive an economic hardship deferment during this

n Accrued interest is capitalized at the time you choose to leave the IBR plan or no longer have a partial inancial hardship.

n If your loan(s) is not repaid in full after you have made the equivalent of 25 years of qualifying monthly payments and at least 25 years have elapsed, any remaining debt will be eligible for forgiveness. If you receive an economic hardship deferment, any months of economic hardship deferment are considered the equivalent of qualifying payments. Months for which you receive any other type of deferment or months of forbearance are not counted as qualifying payments, and do not count toward the

SECTION 8: WHERE TO SEND THE COMPLETED

Return the completed IBR Plan Request and any required documentation to: (If no address is shown, return to your loan holder.)

NELNET

P.O. BOX 82565

LINCOLN, NE

FAX: 1.866.545.9196

If you need help completing this form, call:

(If no telephone number is shown, call your loan holder.)

Page 2 of 3

SECTION 9: IMPORTANT NOTICES

Privacy Act Notice

The Privacy Act of 1974 (5 U.S.C. 552a) requires that the following notice be provided to you:

The authority for collecting the requested information from and about you is §428(b)(2)(A) et seq. of the Higher Education Act (HEA) of 1965, as amended (20 U.S.C. 1078(b)(2)(A) et seq.) and the authorities for collecting and using your Social Security Number (SSN) are §484(a)(4) of the HEA (20 U.S.C. 1091(a)(4)) and 31 U.S.C. 7701(b). Participating in the Federal Family Education Loan (FFEL) Program and giving us your SSN are voluntary, but you must provide the requested information, including your SSN, to participate.

The principal purposes for collecting the information on this form, including your SSN, are to verify your identity, to determine your eligibility to receive a loan or a beneit on a loan (such as a deferment, forbearance, discharge, or forgiveness) under the FFEL Program, to permit the servicing of your loan(s), and, if it becomes necessary, to locate you and to collect and report on your loan(s) if your loan(s) become delinquent or in default. We also use your SSN as an account identiier and to permit you to access your account information electronically. The information in your ile may be disclosed, on a

in order to verify your identity, to determine your eligibility to receive a loan or a beneit on a loan, to permit the servicing or collection of your loan(s), to enforce the terms of the loan(s), to investigate possible fraud and to verify compliance with federal student inancial aid program regulations, or to locate you if you become delinquent in your loan payments or if you default. To provide default rate calculations, disclosures may be made to guaranty agencies, to inancial and educational institutions, or to state agencies. To provide inancial aid history information, disclosures may be made to educational institutions. To assist program administrators with tracking refunds and cancellations, disclosures may be made to guaranty agencies, to inancial and educational institutions, or to federal or state agencies. To provide a standardized method for educational institutions eficiently to submit student enrollment status, disclosures may be made to guaranty agencies or to inancial and educational institutions. To counsel you in repayment efforts, disclosures may be made to guaranty agencies, to inancial and educational institutions, or to federal, state, or local agencies.

In the event of litigation, we may send records to the Department of Justice, a court, adjudicative body, counsel, party, or witness if the disclosure is relevant and necessary to the litigation. If this information, either alone or with other information, indicates a potential violation of law, we may send it to the appropriate authority for action. We may send information to members of Congress if you ask them to help you with federal student aid questions. In circumstances involving employment complaints, grievances, or disciplinary actions, we may disclose relevant records to adjudicate or investigate the issues. If provided for by a collective bargaining agreement, we may disclose records to a labor organization recognized under 5 U.S.C. Chapter 71. Disclosures may be made to our contractors for the purpose of performing any programmatic function that requires disclosure of records. Before making any such disclosure, we will require the contractor to maintain Privacy Act safeguards. Disclosures may also be made to qualiied researchers under Privacy

Act safeguards.

Paperwork Reduction Notice

According to the Paperwork Reduction Act of 1995, no persons are required to respond to a collection of information unless it displays a currently valid OMB control number. The valid OMB control number for this information collection is

U.S. Department of Education, Washington, DC

If you have any comments or concerns regarding the status of your individual submission of this form, write directly to the address shown in Section 8.

Page 3 of 3