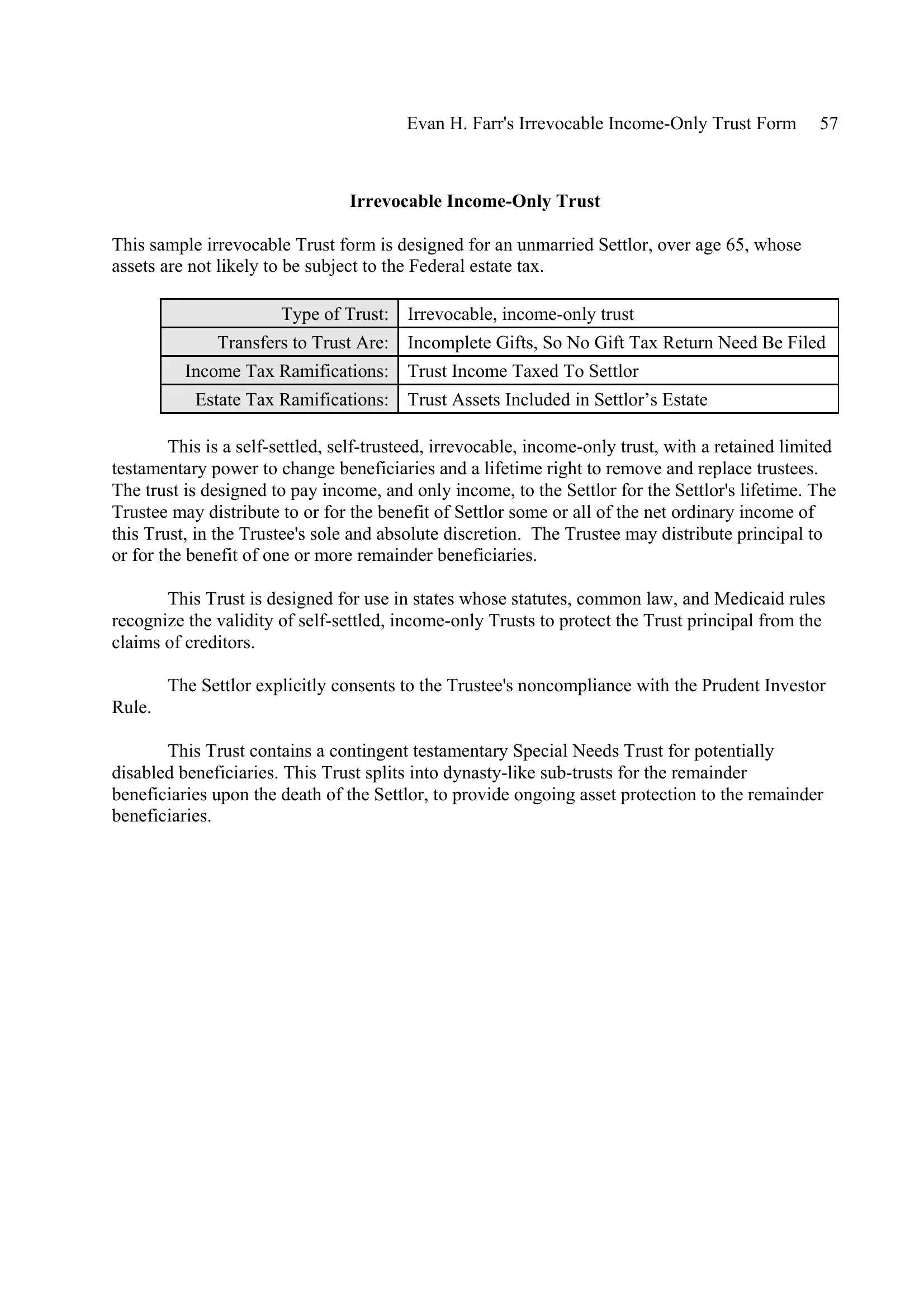

Exploring the nuances of the Income Only Trust form can provide a comprehensive understanding for individuals, particularly unmarried settlers over age 65, looking into estate planning and asset protection. Crafted by Evan H. Farr, this sample Irrevocable Income-Only Trust is designed with a focus on avoiding federal estate tax liabilities, ensuring the settlor's control over income distribution during their lifetime, and protecting the trust principal from creditors' claims. Moreover, an inherent feature of this trust form that stands out is its ability to adapt to the Settlor's needs by allowing the replacement of trustees and the alteration of beneficiaries through a retained limited testamentary power. Despite its rigidity as an irrevocable trust, its design facilitates income provision to the Settlor while offering an elaborate mechanism to safeguard the remainder beneficiaries’ interests. This involves splitting the trust into sub-trusts upon the Settlor's death, each designed to continue the asset protection lineage. Additionally, the trust aligns with the unique Medicaid rules and common law of certain states validating such self-settled, income-only trusts. Important to note is the trust's affirmation of the Settlor’s income tax obligations on trust earnings and the intention for the trust assets to be included in the Settlor’s estate for estate tax purposes. The text not only deliberates on these operational frameworks but also extends into detailing the roles of trustees and trust protectors, including their powers, the process of their appointment, and their independence from the settlor’s influence, to ensure an unbiased administration and protection of the trust's provisions.

| Question | Answer |

|---|---|

| Form Name | Income Only Trust Form |

| Form Length | 5 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 15 sec |

| Other names | irrevocable income form, how to acquire 1 million in income real estate pdf, pdffiller income and expenditure form, how to open a trust |