Instructions

Future Developments

For the latest information about developments related to Form 1042-T and its instructions, such as legislation enacted after they were published, go to www.irs.gov/Form1042T.

Purpose of Form

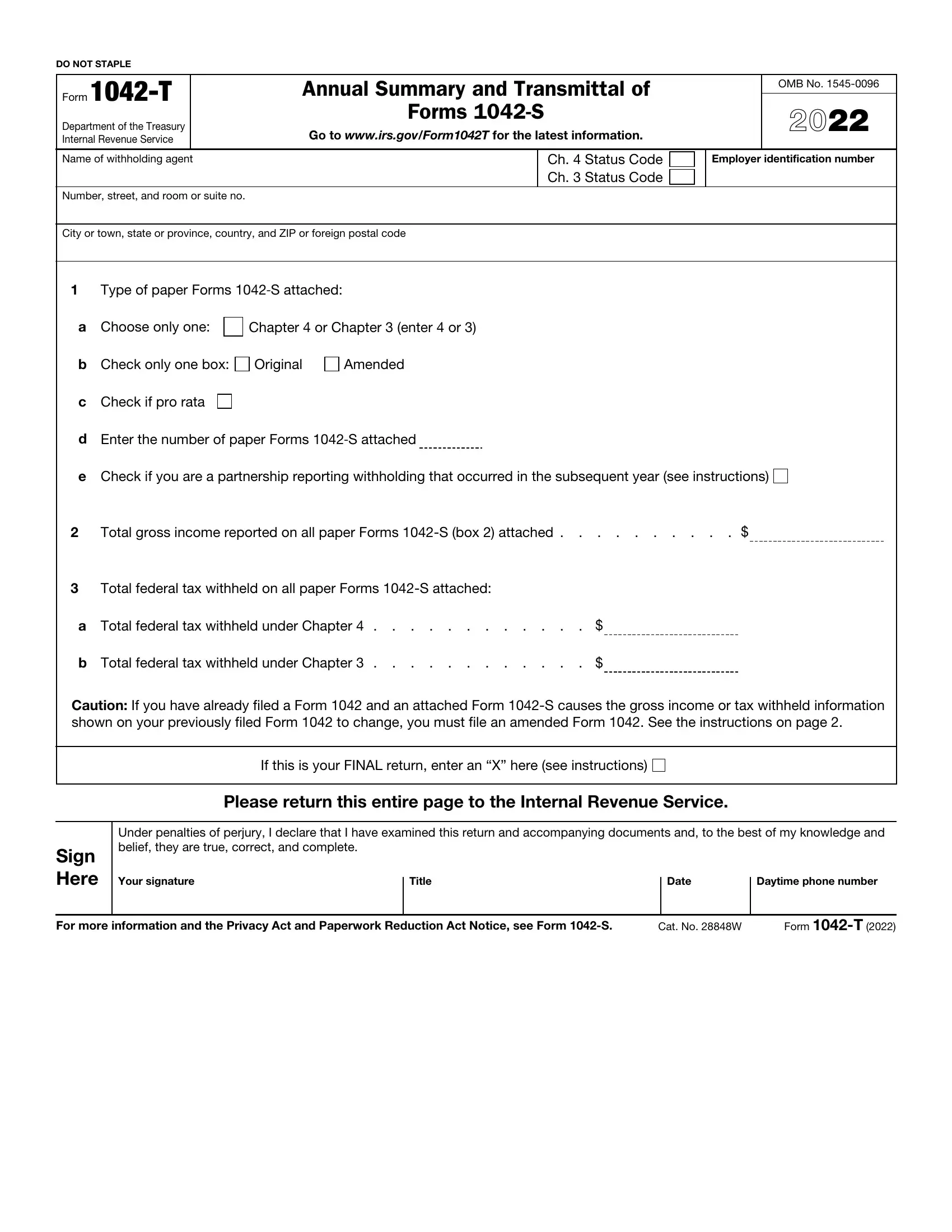

Use this form to transmit paper Forms 1042-S, Foreign Person’s U.S. Source Income Subject to Withholding, to the Internal Revenue Service. Use a separate Form 1042-T to transmit each type of Form 1042-S (see the instructions for line 1 below).

▲Do not use Form 1042-T if you submit Forms 1042-S ! electronically. See the instructions for Form 1042-S

for the electronic filing requirements for Form 1042-S.

CAUTION

Filing Forms 1042 and 1042-S

Use of this form to transmit paper Forms 1042-S does not affect your obligation to file Form 1042, Annual Withholding Tax Return for U.S. Source Income of Foreign Persons.

If you have not yet filed a Form 1042 for 2021, you may send in more than one Form 1042-T to submit paper Forms 1042-S prior to filing your Form 1042. You may submit amended Forms 1042-S even though changes reflect differences in gross income and tax withheld information of Forms 1042-S previously submitted with a Form 1042-T.

If you have already filed a Form 1042 for 2021 and an attached Form 1042-S caused the gross income or tax withheld information previously reported on line 62c or 63e of your Form 1042 to change, you must file an amended Form 1042.

Where and When To File

File Form 1042-T (and Copy A of the paper Forms 1042-S being transmitted) with the Ogden Service Center, P.O. Box 409101, Ogden, UT 84409, by March 15, 2022. Send the forms in a flat mailing (not folded).

Line Instructions

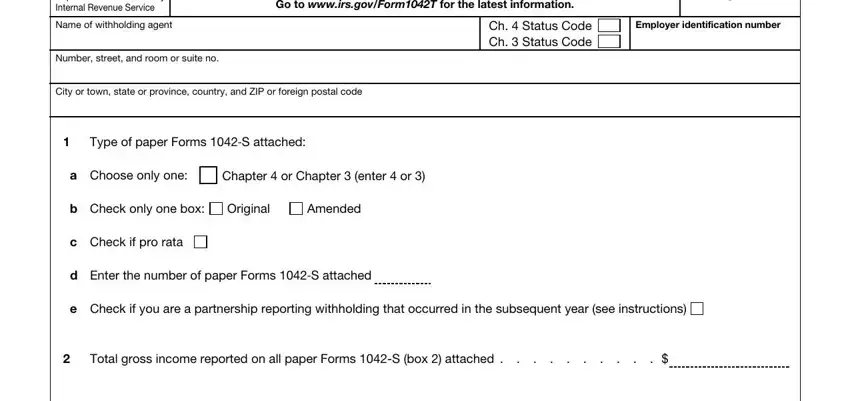

Identifying information at top of form. The name, address, EIN, and chapter 4 and chapter 3 status codes of the withholding agent named on this form must be the same as those you enter on Forms 1042 and 1042-S. See the Instructions for Form 1042 for the definition of withholding agent. See the Instructions for Form 1042-S for the withholding agent codes for the chapter 4 and chapter 3 status codes. You must enter both a chapter 4 and a chapter 3 withholding agent status code regardless of the type of payment being made.

Line 1. You must file a separate Form 1042‐T for each type of paper Form 1042‐S you are transmitting.

Line 1a. Withholding agents are not permitted to file a single Form 1042‐T to transmit both chapter 4 and chapter 3 amounts. Withholding agents must indicate either chapter 4 or chapter 3 to designate the chapter for which they are filing a given Form 1042‐T. The chapter you designate on this form must be the same as that on all attached Forms 1042‐S. See Chapter indicator in the Form 1042‐S instructions for additional information.

Line 1b. Check either the Original or Amended box (but not both).

Line 1c. Check the box on this line 1c if you are filing pro rata Forms 1042‐S (see the Form 1042‐S instructions).

Line 1e. Check the box on line 1e if you are a partnership reporting withholding that occurred in the subsequent year with respect to a foreign partner’s share of undistributed income for the prior year. The attached Form(s) 1042-S should have the checkbox checked in box 7c.

As a result of the above rules, there are sixteen possible types of Form 1042‐S that may be transmitted, and each type requires a separate Form 1042‐T.

•Chapter 4, original, pro rata.

•Chapter 4, original, non‐pro rata.

•Chapter 4, amended, pro rata.

•Chapter 4, amended, non‐pro rata.

•Chapter 4, original, pro rata, partnership.

•Chapter 4, original, non-pro rata, partnership.

•Chapter 4, amended, pro rata, partnership.

•Chapter 4, amended, non-pro rata, partnership.

•Chapter 3, original, pro rata.

•Chapter 3, original, non‐pro rata.

•Chapter 3, amended, pro rata.

•Chapter 3, amended, non‐pro rata.

•Chapter 3, original, pro rata, partnership.

•Chapter 3, original, non-pro rata, partnership.

•Chapter 3, amended, pro rata, partnership.

•Chapter 3, amended, non-pro rata, partnership.

Each type must be transmitted with a separate Form 1042-T. For example, you must transmit only Chapter 3, original, pro rata Forms 1042-S with one Form 1042-T.

Line 2. Enter the total of the gross income amounts shown on the Forms 1042-S (box 2) being transmitted with this Form 1042-T.

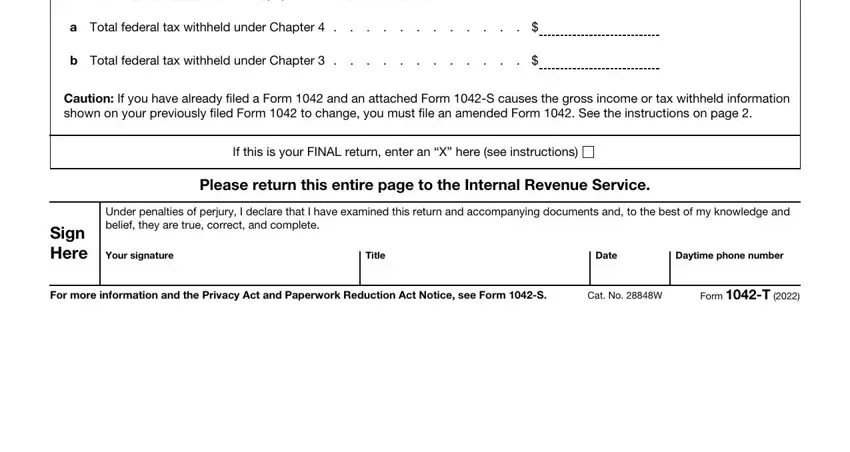

Line 3. Enter the total of the federal tax withheld amounts shown on all Forms 1042-S (total of amounts reported in boxes 10 and 11) being transmitted with this Form 1042-T. On this Form 1042-T, complete either line 3a or line 3b, but not both. If you indicated “Chapter 4” on line 1a, complete line 3a to report the total amounts withheld pursuant to chapter 4. If you indicated “Chapter 3” on line 1a, complete line 3b to report the total amounts withheld pursuant to chapter 3.

Final return. If you will not be required to file additional Forms 1042-S, including amended Forms 1042-S for the 2021 year (on paper or electronically), enter an “X” in the FINAL return box.

Paperwork Reduction Act Notice. The time needed to complete and file this form will vary depending on individual circumstances. The estimated average time is 12 minutes.