When it comes to managing retirement finances, understanding how taxes impact your pension is crucial for making informed decisions. The Maryland Tax 766 form is a pivotal document for those receiving pension allowances from the Maryland State Retirement Agency. It offers retirees an option to specify their preferences for Federal and Maryland State tax withholdings. Filling out this form correctly ensures that the right amount of tax is deducted from your pension payments, potentially avoiding the hassle of owing taxes when filing annual returns. The form serves a dual purpose, covering both federal and state tax elections in one go, simplifying the process for retirees. Whether opting to adjust Federal tax withholdings through specifying allowances or an additional dollar amount or making a clear decision on Maryland State tax deductions, the form provides retirees with flexibility and control over their financial planning. Importantly, any elections made using this form override previous tax withholding requests, making it essential to consider any changes in tax laws or personal circumstances. For Federal taxes, the form aligns with the Internal Revenue Service’s guidelines, specifically relating to the W-4P form, and outlines the implications of not having enough tax withheld. For State taxes, it offers varying options catering to both resident and non-resident retirees of Maryland, acknowledging that everyone’s situation is unique. Understanding and navigating the specifics of the Maryland Tax 766 can ensure a smoother financial transition into retirement, making it an essential task for retirees within the state.

| Question | Answer |

|---|---|

| Form Name | Maryland Tax Form 766 |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | maryland state retirement agency form w 4p, maryland state retirement agency form 766, maryland stat retirement agency form 766, md form766 |

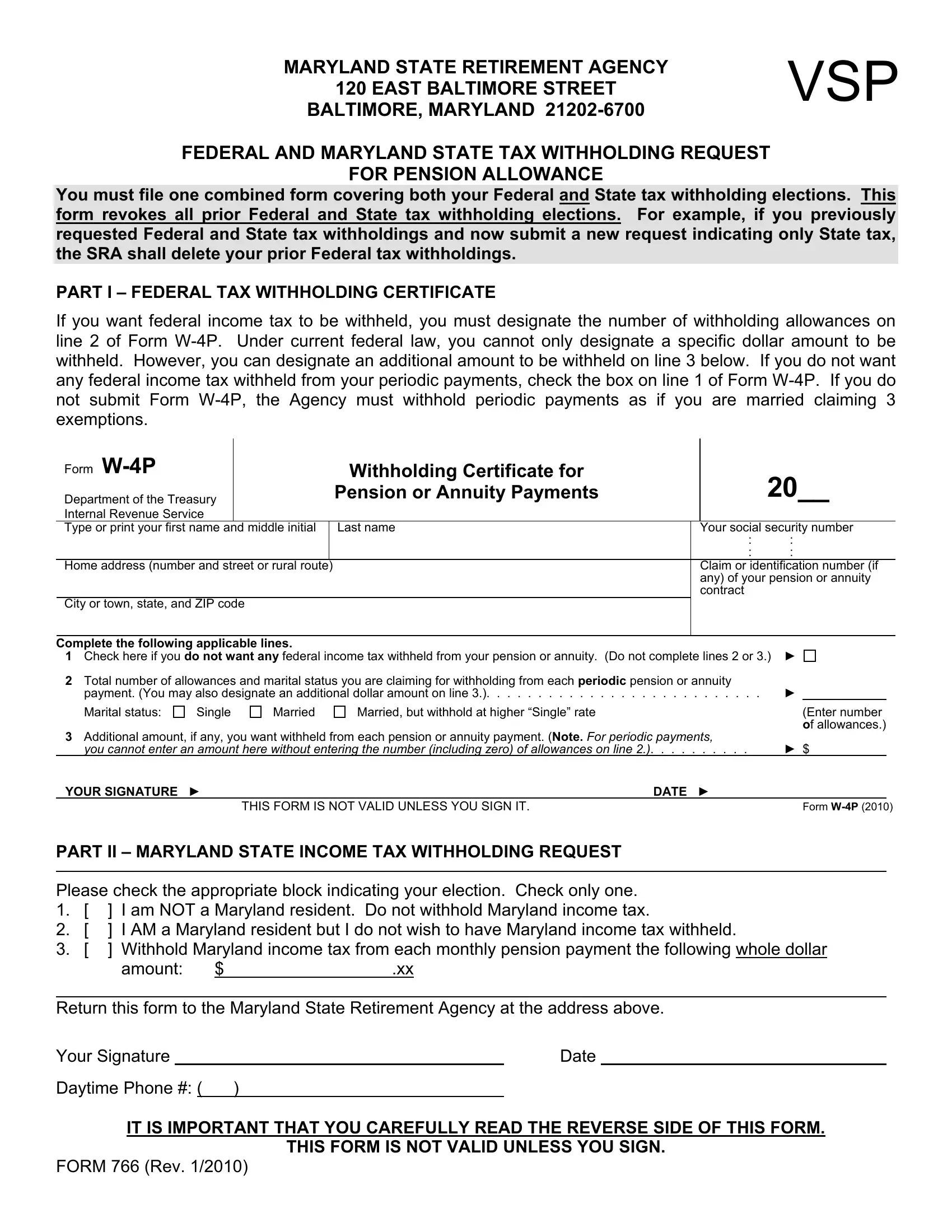

MARYLAND STATE RETIREMENT AGENCY |

VSP |

|

|

120 EAST BALTIMORE STREET |

|

BALTIMORE, MARYLAND |

|

FEDERAL AND MARYLAND STATE TAX WITHHOLDING REQUEST

FOR PENSION ALLOWANCE

You must file one combined form covering both your Federal and State tax withholding elections. This form revokes all prior Federal and State tax withholding elections. For example, if you previously requested Federal and State tax withholdings and now submit a new request indicating only State tax, the SRA shall delete your prior Federal tax withholdings.

PART I – FEDERAL TAX WITHHOLDING CERTIFICATE

If you want federal income tax to be withheld, you must designate the number of withholding allowances on line 2 of Form

Form |

|

|

|

Withholding Certificate for |

|

20__ |

|

||

Department of the Treasury |

|

|

Pension or Annuity Payments |

|

|

||||

|

|

|

|

|

|

|

|

||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

Type or print your first name and middle initial |

|

Last name |

|

Your social security number |

|||||

|

|

|

|

|

: |

: |

|

|

|

|

|

|

|

|

: |

: |

|

|

|

Home address (number and street or rural route) |

|

|

Claim or identification number (if |

||||||

|

|

|

|

|

|

any) of your pension or annuity |

|||

|

|

|

|

|

|

contract |

|

|

|

City or town, state, and ZIP code |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|||

Complete the following applicable lines. |

|

|

|

► |

|||||

1 Check here if you do not want any federal income tax withheld from your pension or annuity. (Do not complete lines 2 or 3.) |

|||||||||

2 Total number of allowances and marital status you are claiming for withholding from each periodic pension or annuity |

► |

|

|

||||||

payment. (You may also designate an additional dollar amount on line 3.) |

|||||||||

Marital status: |

Single |

Married |

Married, but withhold at higher “Single” rate |

|

|

(Enter number |

|||

|

|

|

|

|

|

|

|

of allowances.) |

|

3 Additional amount, if any, you want withheld from each pension or annuity payment. (Note. For periodic payments, |

► $ |

||||||||

you cannot enter an amount here without entering the number (including zero) of allowances on line 2.). . . . |

. . . . . . |

||||||||

YOUR SIGNATURE |

► |

|

|

DATE |

► |

|

|

|

|

|

|

THIS FORM IS NOT VALID UNLESS YOU SIGN IT. |

|

|

|

Form |

|||

PART II – MARYLAND STATE INCOME TAX WITHHOLDING REQUEST

Please check the appropriate block indicating your election. Check only one.

1.[ ] I am NOT a Maryland resident. Do not withhold Maryland income tax.

2.[ ] I AM a Maryland resident but I do not wish to have Maryland income tax withheld.

3.[ ] Withhold Maryland income tax from each monthly pension payment the following whole dollar

amount: |

$ |

.xx |

Return this form to the Maryland State Retirement Agency at the address above.

Your Signature |

|

|

Date |

|

Daytime Phone #: ( |

) |

|

||

|

|

|

|

|

IT IS IMPORTANT THAT YOU CAREFULLY READ THE REVERSE SIDE OF THIS FORM.

THIS FORM IS NOT VALID UNLESS YOU SIGN.

FORM 766 (Rev. 1/2010)

2

Part I

FEDERAL INCOME TAX WITHHOLDING

The monthly retirement payments you receive from the Maryland State Retirement and Pension System may be subject to Federal income tax withholding. For further information, please refer to Internal Revenue Service Publication 575 regarding the taxability of pension and annuity income.

As a retiree, the following Federal income tax withholding alternatives are available to you:

1.You may elect not to have Federal income tax deducted from your monthly retirement payment, or

2.You may claim a certain number of exemptions and have the Maryland State Retirement and Pension System deduct the appropriate amount, if any, in accordance with the Federal income tax tables and you may designate an additional specific whole dollar amount to be withheld from your monthly retirement payment.

If you elect not to have Federal withholding apply to your monthly retirement payments, or if you do not have enough Federal income tax withheld, you may be responsible for payment of estimated tax. You may incur penalties under the Internal Revenue Service estimated tax rules if your withholding and estimated tax payment are not sufficient. New retirees, especially, should see IRS Publication 505.

Part II

MARYLAND STATE INCOME TAX WITHHOLDING

The monthly retirement payments you receive from the Maryland State Retirement and Pension System may be subject to Maryland income tax withholding.

As a retiree and a Maryland resident, the following Maryland income tax withholding alternatives are available to you:

1.You may elect not to have Maryland income tax deducted from your monthly retirement payment, or

2.You may designate a specific whole dollar amount to be withheld from your monthly retirement payment.

If you elect not to have Maryland withholding apply to your monthly retirement payments, or if you do not have enough Maryland income tax withheld, you may be responsible for payment of estimated tax.

An election of any one of the alternatives will remain in effect until you revoke it. You may revoke or change your election at any time by filing a new Federal and Maryland State Tax Withholding Request.

The Maryland State Retirement Agency can not assist you in the preparation of tax returns. Please contact the Internal Revenue Service at

To receive additional copies of the Federal and Maryland State Tax Withholding Request form, or for other information concerning your retirement benefits, call

SEE REVERSE SIDE FOR FEDERAL AND MARYLAND STATE TAX WITHHOLDING REQUEST

FORM 766 (Rev. 1/2010)

Additional Instructions:

Section references are to the Internal Revenue Code. Agency refers to the Maryland State Retirement Agency.

When should I complete the form? Complete Form

Other income. If you have a large amount of income from other sources not subject to withholding (such as interest, dividends, or capital gains), consider making estimated tax payments using Form

Withholding From Pensions and Annuities

Generally, federal income tax withholding applies to the taxable part of payments made from pension,

Because your tax situation may change from year to year, you may want to refigure your withholding each year. You can change the amount to be withheld by using lines 2 and 3 of Form

Choosing not to have income tax withheld. You (or in the event of death, your beneficiary or estate) can choose not to have federal income tax withheld from your payments by using line 1 of Form

Caution. There are penalties for not paying enough federal income tax during the year, either through withholding or estimated tax payments. New retirees, especially, should see Pub. 505. It explains your estimated tax requirements and describes penalties in detail. You may be able to avoid quarterly estimated tax payments by having enough tax withheld from your pension or annuity using Form

Periodic payments. Withholding from periodic payments of a pension or annuity is figured in the same manner as withholding from wages. Periodic payments are made in installments at regular intervals over a period of more than 1 year. They may be paid annually, quarterly, monthly, etc.

If you want federal income tax to be withheld, you must designate the number of withholding allowances on line 2 of Form

3

designate an additional amount to be withheld on line 3. If you do not want any federal income tax withheld from your periodic payments, check the box on line 1 of Form

Caution. If you do not submit Form

If you submit a Form

taxpayer identification number (TIN), the payer must withhold as if you are single claiming zero withholding allowances even if you choose not to have federal income tax withheld.

There are some kinds of periodic payments for which you cannot use Form

For periodic payments, your Form

Changing Your “No Withholding” Choice

Periodic Payments. If you previously chose not to have federal income tax withheld and you now want withholding, complete another Form

Payments to Foreign Persons and

Payments Outside the United States

Unless you are a nonresident alien, withholding (in the manner described above) is required on any periodic or nonperiodic payments that are delivered to you outside the United States or its possessions. You cannot choose not to have federal income tax withheld on line 1 of Form

In the absence of a tax treaty exemption, nonresident aliens, nonresident alien beneficiaries, and foreign estates generally are subject to a 30% federal withholding tax under section 1441 on the taxable portion of a periodic or nonperiodic pension or annuity payment that is from U.S. sources. However, most tax treaties provide that private pensions and annuities are exempt from withholding and tax. Also, payments from certain pension plans are exempt from withholding even if no tax treaty applies. See Pub.

Statement of Federal Income Tax Withheld From Your Pension or Annuity

By January 31 of next year, your payer will furnish a statement to you on Form