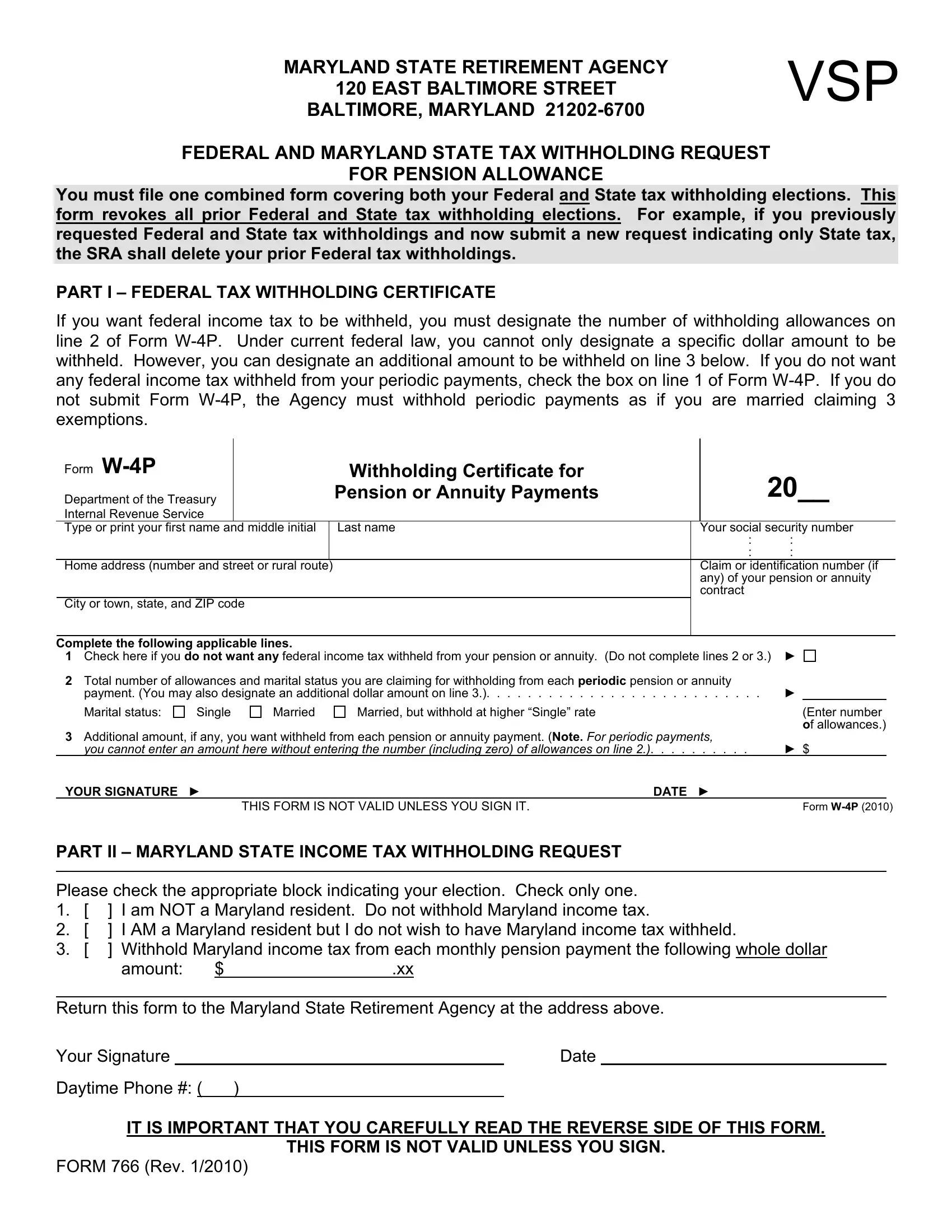

When it comes to managing retirement finances, understanding how taxes impact your pension is crucial for making informed decisions. The Maryland Tax 766 form is a pivotal document for those receiving pension allowances from the Maryland State Retirement Agency. It offers retirees an option to specify their preferences for Federal and Maryland State tax withholdings. Filling out this form correctly ensures that the right amount of tax is deducted from your pension payments, potentially avoiding the hassle of owing taxes when filing annual returns. The form serves a dual purpose, covering both federal and state tax elections in one go, simplifying the process for retirees. Whether opting to adjust Federal tax withholdings through specifying allowances or an additional dollar amount or making a clear decision on Maryland State tax deductions, the form provides retirees with flexibility and control over their financial planning. Importantly, any elections made using this form override previous tax withholding requests, making it essential to consider any changes in tax laws or personal circumstances. For Federal taxes, the form aligns with the Internal Revenue Service’s guidelines, specifically relating to the W-4P form, and outlines the implications of not having enough tax withheld. For State taxes, it offers varying options catering to both resident and non-resident retirees of Maryland, acknowledging that everyone’s situation is unique. Understanding and navigating the specifics of the Maryland Tax 766 can ensure a smoother financial transition into retirement, making it an essential task for retirees within the state.

| Question | Answer |

|---|---|

| Form Name | Maryland Tax Form 766 |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | maryland state retirement agency form w 4p, maryland state retirement agency form 766, maryland stat retirement agency form 766, md form766 |