In Massachusetts, individuals who have filed joint income tax returns sometimes find themselves seeking relief from liabilities that arise due to discrepancies or omissions in their shared filing. The Massachusetts Department of Revenue provides a form, known as Form 84, that allows eligible taxpayers to apply for relief from such joint income tax liabilities under specific conditions. This form serves as a critical resource for those who believe they should not be held responsible for a substantial understatement of tax resulting from their spouse's erroneous items of income, deductions, exemptions, credits, or basis claims. The application process outlined in Form 84 requires applicants to provide detailed information and supportive documentation, including any previous appeals for federal tax relief, notices of assessment or intention to assess, and a thorough explanation of the circumstances that justify their request for relief. Additionally, the form mandates a declaration of truthfulness under penalty of perjury by both the applicant and, if applicable, their preparer. The provision of relief, as decided by the Department of Revenue, depends on a multifaceted review of the application, emphasizing the fairness and equity of holding the applicant liable given their knowledge and benefit from the understatement. Importantly, the filing of Form 84 does not automatically stay the collection of taxes owed unless the application for relief is granted, highlighting the importance of understanding the procedural nuances and timely submission of this application within Massachusetts' tax relief framework.

| Question | Answer |

|---|---|

| Form Name | Massachusetts Form 84 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | 84 mass form 84 fillable |

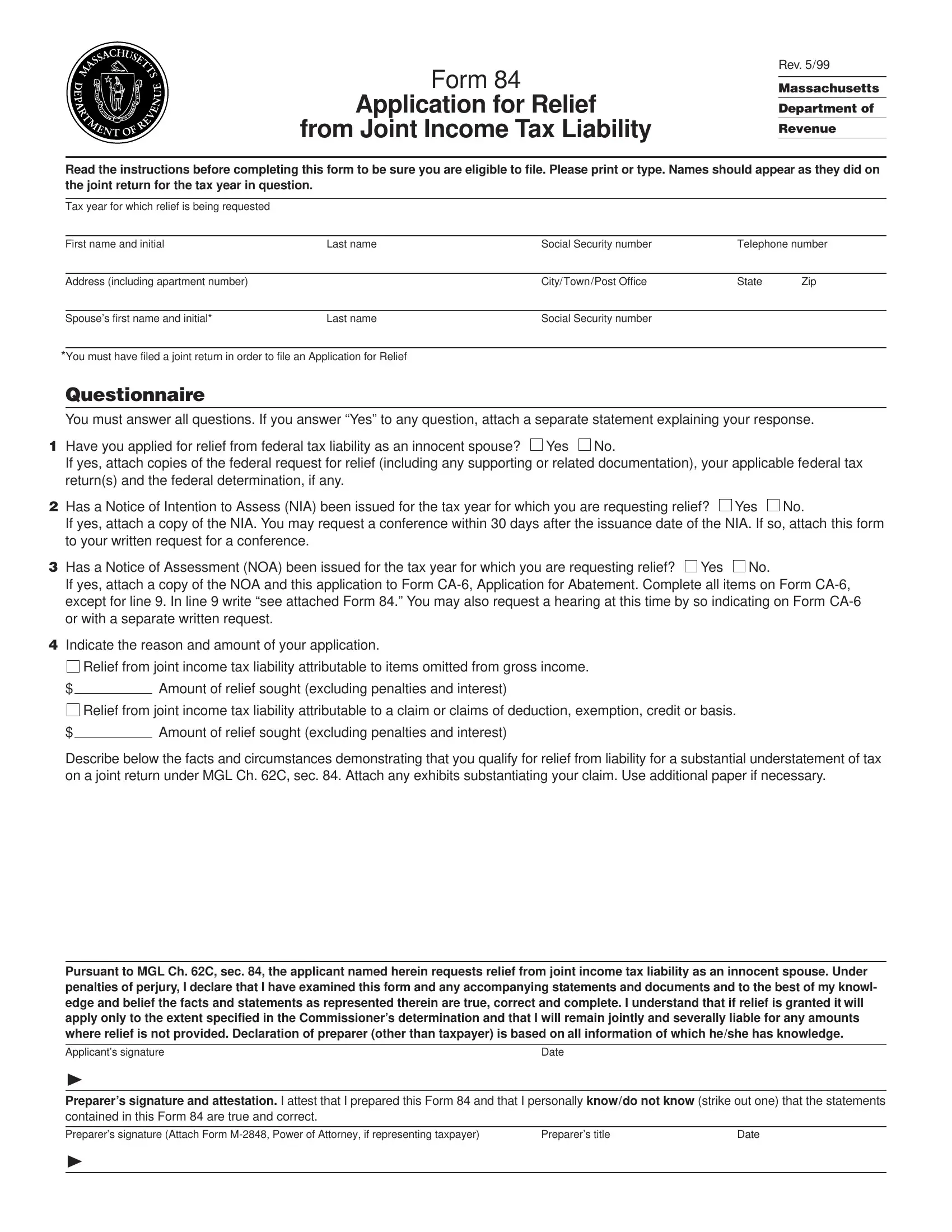

Form 84

Application for Relief

from Joint Income Tax Liability

Rev. 5/99

Massachusetts

Department of

Revenue

Read the instructions before completing this form to be sure you are eligible to file. Please print or type. Names should appear as they did on the joint return for the tax year in question.

Tax year for which relief is being requested

First name and initial |

Last name |

Social Security number |

Telephone number |

|

|

|

|

|

|

Address (including apartment number) |

|

City/Town/Post Office |

State |

Zip |

|

|

|

|

|

Spouse’s first name and initial* |

Last name |

Social Security number |

|

|

*You must have filed a joint return in order to file an Application for Relief

Questionnaire

You must answer all questions. If you answer “Yes” to any question, attach a separate statement explaining your response.

1Have you applied for relief from federal tax liability as an innocent spouse? Yes No.

If yes, attach copies of the federal request for relief (including any supporting or related documentation), your applicable federal tax return(s) and the federal determination, if any.

2Has a Notice of Intention to Assess (NIA) been issued for the tax year for which you are requesting relief? Yes No.

If yes, attach a copy of the NIA. You may request a conference within 30 days after the issuance date of the NIA. If so, attach this form to your written request for a conference.

3Has a Notice of Assessment (NOA) been issued for the tax year for which you are requesting relief? Yes No.

If yes, attach a copy of the NOA and this application to Form

4Indicate the reason and amount of your application.

Relief from joint income tax liability attributable to items omitted from gross income.

$ |

|

Amount of relief sought (excluding penalties and interest) |

Relief from joint income tax liability attributable to a claim or claims of deduction, exemption, credit or basis.

$ |

|

Amount of relief sought (excluding penalties and interest) |

Describe below the facts and circumstances demonstrating that you qualify for relief from liability for a substantial understatement of tax on a joint return under MGL Ch. 62C, sec. 84. Attach any exhibits substantiating your claim. Use additional paper if necessary.

Pursuant to MGL Ch. 62C, sec. 84, the applicant named herein requests relief from joint income tax liability as an innocent spouse. Under penalties of perjury, I declare that I have examined this form and any accompanying statements and documents and to the best of my knowl- edge and belief the facts and statements as represented therein are true, correct and complete. I understand that if relief is granted it will apply only to the extent specified in the Commissioner’s determination and that I will remain jointly and severally liable for any amounts where relief is not provided. Declaration of preparer (other than taxpayer) is based on all information of which he/she has knowledge.

Applicant’s signature |

Date |

¨

Preparer’s signature and attestation. I attest that I prepared this Form 84 and that I personally know/do not know (strike out one) that the statements contained in this Form 84 are true and correct.

Preparer’s signature (Attach Form |

Preparer’s title |

Date |

¨

Form 84 Instructions

General Information

The Department of Revenue is authorized to grant relief from a joint income tax liability under certain conditions. Relief can be granted where a taxpayer and a spouse file a joint income tax return reporting a substantial understatement of tax attributable to grossly erroneous items of one spouse if (1) the spouse requesting relief establishes that he or she did not know, and had no reason to know, that there was such a substantial under- statement; and (2) taking into account all facts and circum- stances of a case, it would be inequitable to hold the applicant liable for the deficiency.

For further information refer to Regulation 830 CMR 62C.84.1 Spousal Relief From Joint Income Tax Liability. This regulation is available by calling the Rulings and Regulations Bureau at (617)

Substantial Understatement

To be considered substantial, the understated tax, excluding any interest and penalties, must exceed $200 where due to an item omitted from gross income; or exceed $500 where due to a claim or claims of deduction, exemption, credit or basis, for which there is no basis in fact or law.

Inequitable Liability

Whether it is inequitable to hold a person liable for a tax defi- ciency will be determined by all the facts and circumstances of a case. Although no single factor is controlling, consideration will be given to whether the applicant significantly benefited from the substantial understatement of tax.

Application for Relief

A taxpayer wishing to apply for relief must submit this form within the time prescribed for challenging an assessment or a proposed assessment under MGL Ch. 62C, sections 26 and 37. Applicants should attach copies of any federal claim for relief,

the federal determination, and the federal tax return. Applicants should also submit any documents or exhibits substantiating this application. The filing of this form will not stay the collection of tax unless or until this application is approved. If the applica- tion is approved, a refund of any resulting overpayment of tax will be made to the applicant.

Application Prior to Assessment

If a taxpayer has received a Notice of Intention to Assess (NIA), this application must be received within 30 days following the issuance of the NIA. The applicant is entitled to a conference if one is requested within this

Application After Assessment

If a taxpayer has received a Notice of Assessment (NOA), this application must be made by filing an Application for Abatement (Form

(617)

Notice of Determination

A written notice of determination will be issued to the applicant. A grant of relief will only apply to the extent specified in the writ- ten determination. The applicant remains jointly and severally li- able for any amounts where relief is not granted. Also, the appli- cant’s spouse remains liable for the entire tax determined to be due. If the grant of relief was obtained by false or fraudulent means, the grant of relief is void.