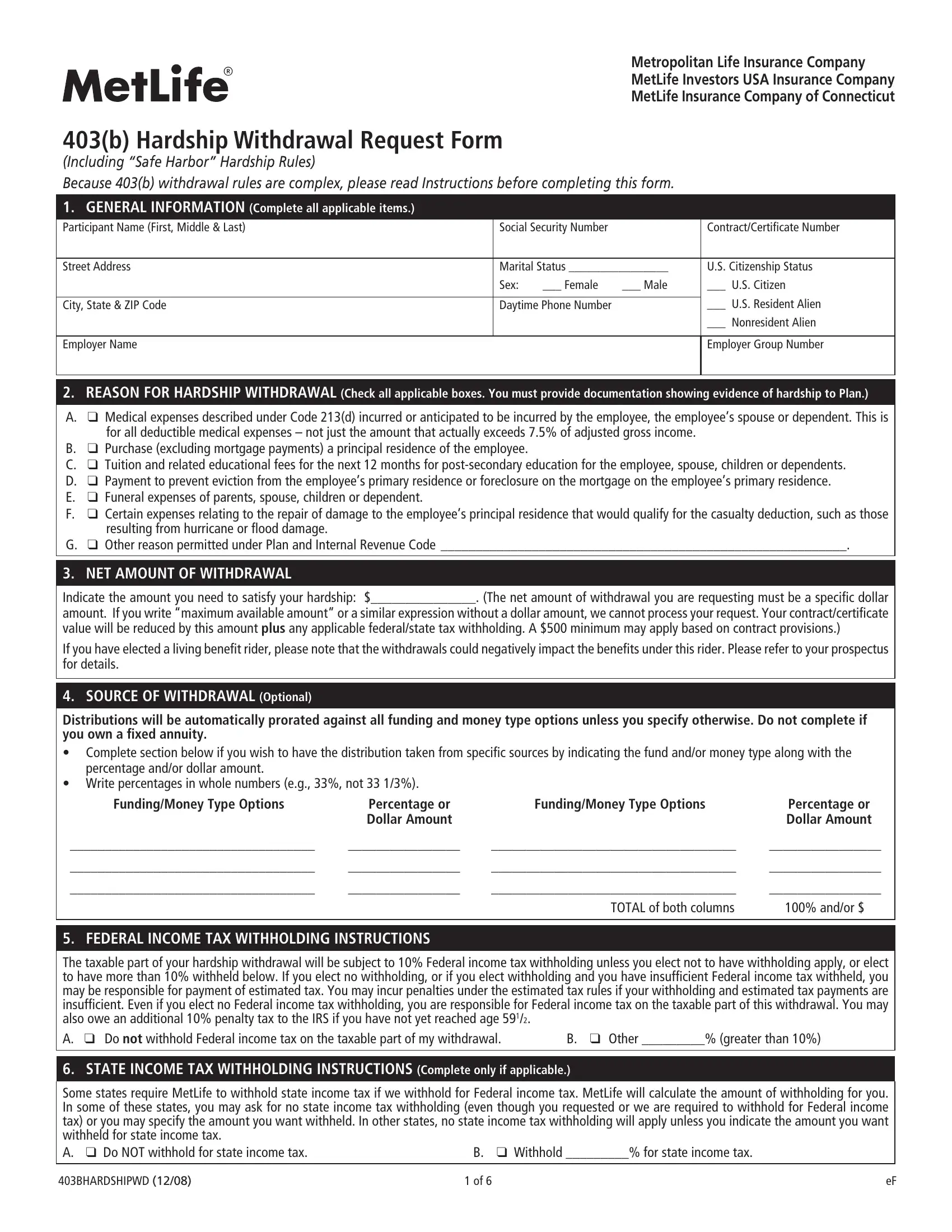

Facing financial hardship can be a demanding and stressful experience, especially when you need access to funds locked in retirement plans. The MetLife Withdrawal Form presents a pathway for individuals to tap into their 403(b) accounts during difficult times under specific hardship circumstances, adhering to strict regulations and requirements set forth by both the plan provider and the IRS. This form caters to various hardship reasons including medical expenses, purchase of a principal residence, educational fees, prevention of eviction or foreclosure, funeral expenses, and certain repair costs from damage to a principal residence, among others. Participants are required to provide documentation demonstrating their hardship and specify the net amount needed to alleviate their situation, subject to a minimum amount and potential impact on benefits from living benefit riders. Additionally, the form outlines federal and state income tax withholding instructions, enabling participants to opt out or specify a withholding percentage, recognizing the potential tax implications and penalties associated with early withdrawals. Moreover, specific sections address annuity information, qualified joint and survivor annuity waivers, and spousal consent, ensuring all regulatory bases are covered. As such, completing the MetLife Hardship Withdrawal Request Form involves careful consideration of one’s immediate financial needs, the impact on future retirement benefits, and the accompanying tax responsibilities.

| Question | Answer |

|---|---|

| Form Name | Metlife Withdrawal Form |

| Form Length | 6 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 30 sec |

| Other names | metlife hardship withdrawal form, 403b hardship form, 403 b withdrawal request form, 403b withdrawal form |