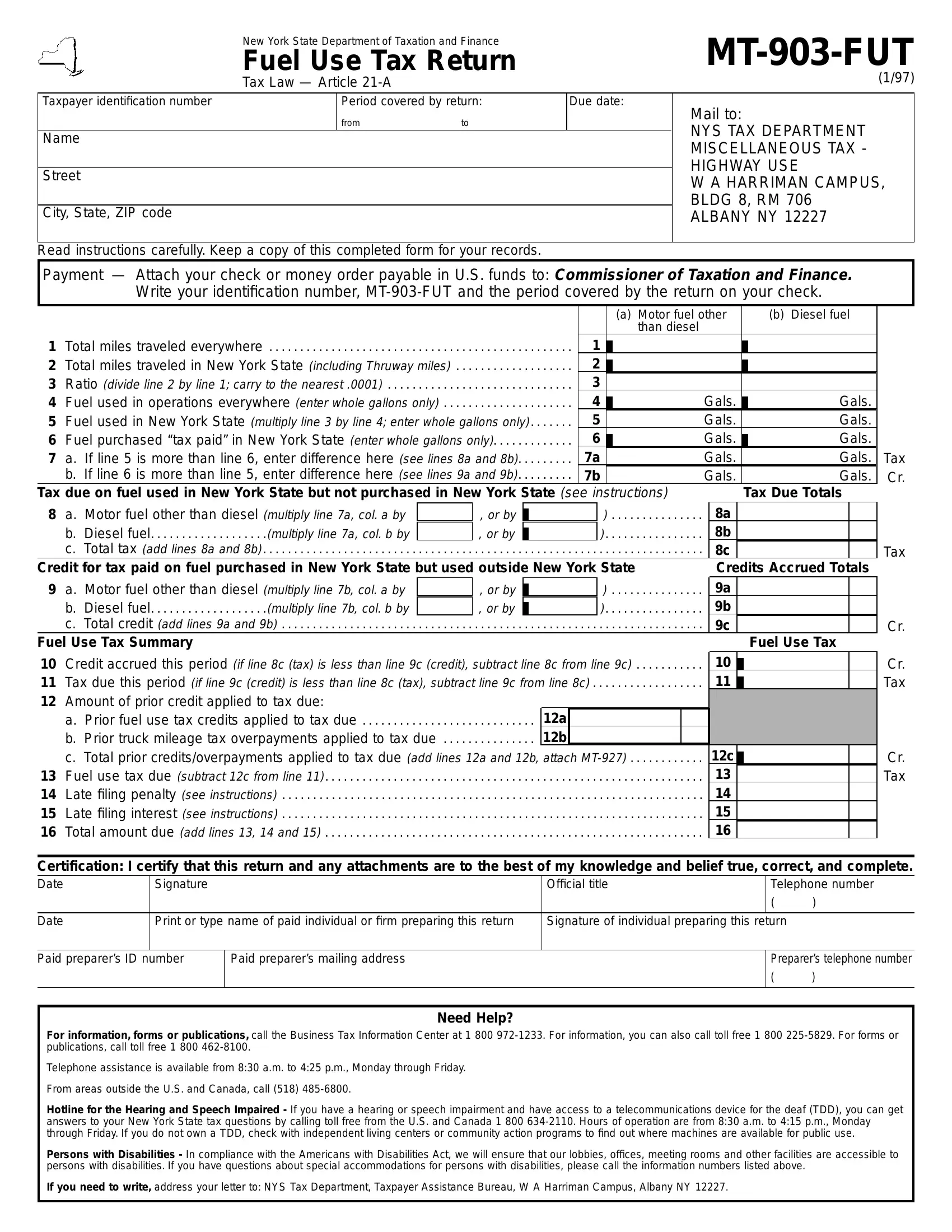

Understanding the intricacies of the Mt 903 Fut form, an essential document for those navigating New York State's taxation landscape, is invaluable for carriers operating vehicles subject to fuel use taxation. Issued by the New York State Department of Taxation and Finance, this Fuel Use Tax Return, adhering to Tax Law Article 21-A, plays a critical role in ensuring compliance with state tax obligations. Designed for a precise period, and with a strict deadline for submission, it requires detailed information about the taxpayer and the operational metrics of vehicles, including total miles traveled and fuel used both within and outside New York State. It demands meticulous record-keeping and an accurate calculation of the tax payable or credit due, factoring in fuel purchases that have already been taxed. Instructions are provided to aid in the accurate completion of the form, highlighting the importance of keeping a copy for records, the need for accurate figures regarding fuel consumption, and the possibility of facing penalties for late submissions or inaccurate filings. The form also opens up avenues for credits or refunds under certain conditions, emphasizing the state's acknowledgment of fair taxation practices. Carriers must therefore approach this form with diligence, ensuring that all required information is accurately reported to avoid penalties and to capitalize on potential credits.

| Question | Answer |

|---|---|

| Form Name | Mt 903 Fut Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | instruction for mt 903 ny, form mt 903 instructions, mt 903 1 form, mt 903 fut form |