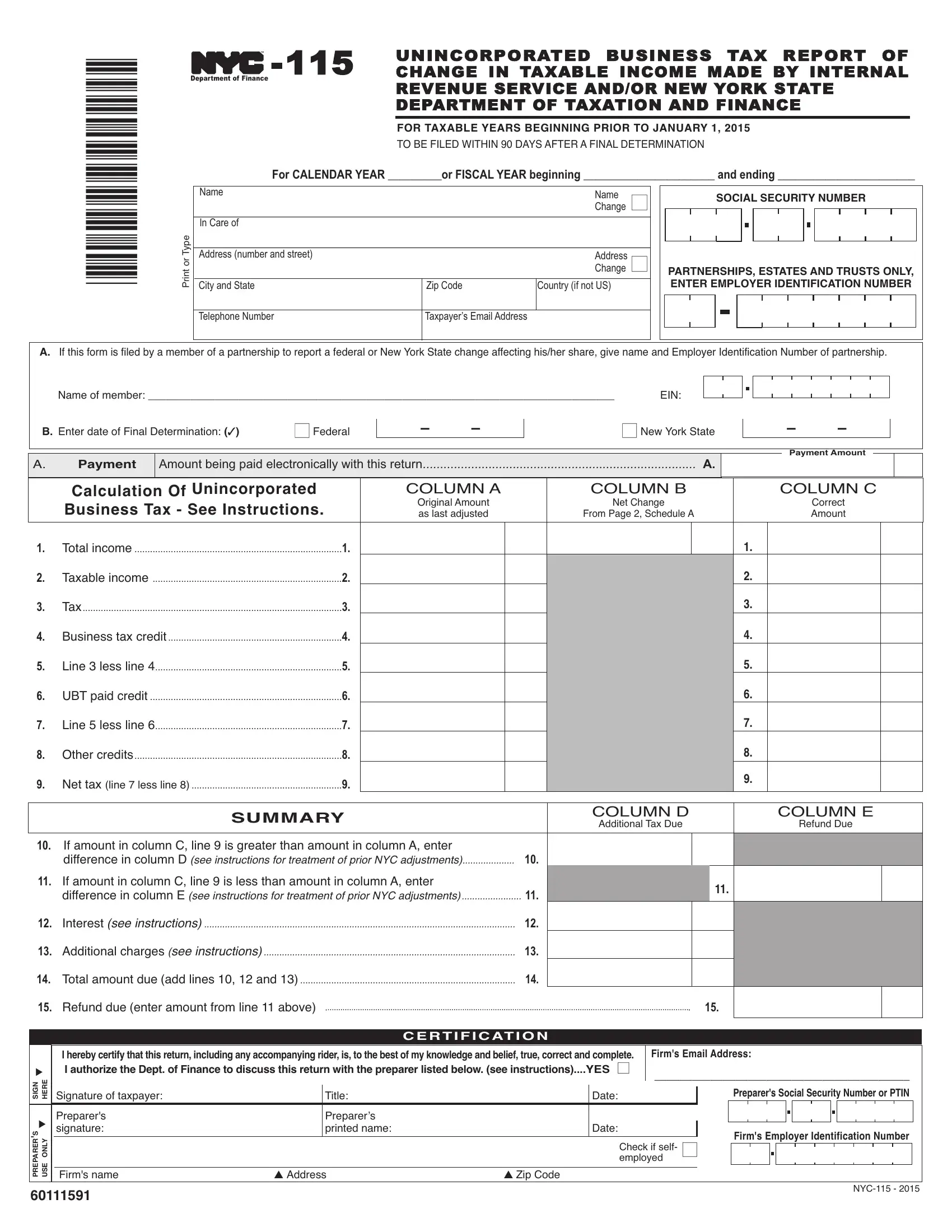

The NYC-115 form, a crucial document issued by the Department of Finance, is designed to report adjustments in taxable income as a result of audits conducted by the Internal Revenue Service (IRS) and/or the New York State Department of Taxation and Finance. Intended for taxable years beginning before January 1, 2015, this form must be filed within 90 days following a final determination from these audits. It encompasses various sections, including information about the taxpayer, detailed calculations of unincorporated business tax, and adjustments resulting from federal or state changes. Moreover, it lays out specific instructions for payment, including options for electronic submissions and the necessity of using payment voucher Form NYC-200V in certain cases. Schedules A and B further detail adjustments made and the computation of business tax credit, respectively. This form not only serves as a means to comply with tax obligations following audit adjustments but also includes provisions for claiming refunds or reporting additional tax due. With its comprehensive instructions and structured format, the NYC-115 form aids taxpayers in accurately reporting audit-induced income adjustments, ensuring compliance with the city's taxation regulations.

| Question | Answer |

|---|---|

| Form Name | Nyc 115 Form |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | form nyc 115, form nyc115, nyc 115, finance form nyc 115 |

*60111591*

TM |

UNINCORPORATED BUSINESS TAX REPORT OF |

Department of Finance |

CHANGE IN TAXABLE INCOME MADE BY INTERNAL |

REVENUE SERVICE AND/OR NEW YORK STATE

DEPARTMENT OF TAXATION AND FINANCE

FOR TAXABLE YEARS BEGINNING PRIOR TO JANUARY 1, 2015

TO BE FILED WITHIN 90 DAYSAFTERAFINAL DETERMINATION

For CALENDAR YEAR _________or FISCAL YEAR beginning ______________________ and ending _______________________

|

Name |

|

Name |

n |

|

|

|

||

|

|

|

Change |

|

|

|

|

|

|

|

In Care of |

|

|

|

Type |

|

|

|

|

Address (number and street) |

|

Address |

|

|

or |

|

|

||

|

|

Change n |

||

|

|

|||

City and State |

Zip Code |

Country (if not US) |

|

|

|

|

|||

|

|

|

|

|

|

Telephone Number |

Taxpayer’s Email Address |

|

|

|

|

|

|

|

SOCIAL SECURITY NUMBER

PARTNERSHIPS, ESTATESAND TRUSTS ONLY, ENTER EMPLOYER IDENTIFICATION NUMBER

A.If this form is filed by a member of a partnership to report a federal or New York State change affecting his/her share, give name and Employer Identification Number of partnership.

Name of member: _____________________________________________________________________________ |

EIN: |

B. Enter date of Final Determination: (3) |

nFederal |

- -

nNew York State

- -

A.Payment

...............................................................................Amountbeingpaidelectronicallywiththisreturn |

A. |

|

|

Payment Amount

|

Calculation Of Unincorporated |

|

COLUMN A |

|

COLUMN B |

|

|

|

COLUMN C |

||

|

Business Tax - See Instructions. |

|

Original Amount |

|

Net Change |

|

|

|

Correct |

||

|

|

as last adjusted |

|

From Page 2, ScheduleA |

|

|

|

Amount |

|||

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Total income |

|

|

|

|

|

|

1. |

|

|

|

2. |

Taxable income |

2. |

|

|

|

|

|

|

2. |

|

|

3. |

Tax |

3. |

|

|

|

|

|

|

3. |

|

|

4. |

Business tax credit |

4. |

|

|

|

|

|

|

4. |

|

|

5. |

Line 3 less line 4 |

5. |

|

|

|

|

|

|

5. |

|

|

6. |

UBT paid credit |

6. |

|

|

|

|

|

|

6. |

|

|

7. |

Line 5 less line 6 |

7. |

|

|

|

|

|

|

7. |

|

|

8. |

Other credits |

8. |

|

|

|

|

|

|

8. |

|

|

9. |

Net tax (line 7 less line 8) |

9. |

|

|

|

|

|

|

9. |

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

SUMMARY |

|

COLUMN D |

|

|

|

COLUMN E |

||||

|

|

Additional Tax Due |

|

|

|

Refund Due |

|||||

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|||

10. If amount in column C, line 9 is greater than amount in column A, enter |

|

|

|

|

|

|

|

|

|||

|

difference in column D (see instructions for treatment of prior NYC adjustments) |

10. |

|

|

|

|

|

|

|

||

11. |

If amount in column C, line 9 is less than amount in column A, enter |

|

|

|

|

11. |

|

|

|

||

|

difference in column E (see instructions for treatment of prior NYC adjustments) |

11. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

||||

12. |

Interest (see instructions) |

|

12. |

|

|

|

|

|

|

|

|

13. |

Additional charges (see instructions) |

|

13. |

|

|

|

|

|

|

|

|

14. |

Total amount due(add lines 10, 12 and 13) |

|

14. |

|

|

|

|

|

|

|

|

15. |

Refund due(enter amount from line 11 above) |

|

|

|

|

|

15. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CERTIFICATION

t |

|

SIGN |

HERE |

|

|

|

t |

PREPARER'S |

USE ONLY |

|

|

Iherebycertifythatthisreturn,includinganyaccompanyingrider,is,tothebestofmyknowledgeandbelief,true,correctandcomplete. |

Firm's EmailAddress: |

||||||||||||||||||

IauthorizetheDept.ofFinancetodiscussthisreturnwiththepreparerlistedbelow.(seeinstructions)....YES n |

_________________________________________ |

||||||||||||||||||

Signature of taxpayer: |

|

Title: |

|

Date: |

|

|

Preparer'sSocialSecurityNumberorPTIN |

||||||||||||

|

|

|

|

||||||||||||||||

Preparer's |

|

Preparer’s |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

signature: |

|

printed name: |

|

Date: |

|

|

Firm's Employer Identification Number |

||||||||||||

|

|

|

|

Check if self- n |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

employed |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm's name |

s Address |

s Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

60111591

Form |

Page 2 |

SCHEDULEA

Explanation of Federal and/or New York StateAdjustments (if additional space is needed, attach schedule)

1. |

Items increasing profit (or decreasing loss) from business or profession (federal Schedule C) or |

COLUMN F |

|

|

partnership income (federal Form 1065 or Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Total increases |

|

|

3.Items decreasing profit (or increasing loss) from business or profession (federal Schedule C) or partnership income (federal Form 1065 or Form

4.Total decreases

5.Net (federal/New York State) adjustments (combine lines 2 and 4)

NEW YORK CITY CHANGESAFFECTING (Federal/New York State)ADJUSTMENTS LISTEDABOVE

6.Additions (see instructions) t

7. Total additions

8.Subtractions (see instructions) t

9.Total subtractions

10.Net New York City changes (combine lines 7 and 9)

11.Net reportable changes (transfer amount to page 1, column B, line 1)

SCHEDULE B

Computation of Business Tax Credit - page 1, line 4, column C (check one)

nBusiness Tax Credit for 1996

1.If the tax on page 1, line 3, Column C is $800 or less, your credit on line 4 is the entire amount of tax on page 1, line 3, Column C.

2.If the tax on page 1, line 3, Column C is $1,000 or over, no credit is allowed. Enter “0” on page 1, line 4, Column C.

3.If the tax on page 1, line 3, Column C is over $800 but less than $1,000, your credit is computed by the following formula:

tax on page 1, line 3, Column C X ( |

$1,000 minus tax on page 1, line 3, Column C ) |

= |

___________ |

|

$200 |

|

(your credit) |

nBusiness Tax Credit for 1997 through 2008

1.Ifthetaxonpage1,line3,ColumnCis$1,800orless,yourcreditonline4istheentireamountoftaxonpage1,line3,ColumnC.

2.If the tax on page 1, line 3, Column C is $3,200 or over, no credit is allowed. Enter “0” on page 1, line 4, Column C.

3.If the tax on page 1, line 3, Column C is over $1,800 but less than $3,200, your credit is computed by the following formula:

tax on page 1, line 3, Column C X ( $3,200 minus tax on page 1, line 3, Column C ) |

= |

___________ |

$1,400 |

|

(your credit) |

*60121591*

nBusiness Tax Credit for 2009 and Later

1.Iftheamountonpage1,line3,ColumnCis$3,400orless,yourcreditonline4istheentireamountoftaxonpage1,line3,ColumnC.

2.If the amount on page 1, line 3, Column C is $5,400 or over, no credit is allowed. Enter “0” on page 1, line 4, Column C.

3.If the amount on page 1, line 3, Column C is over $3,400 but less than $5,400, your credit is computed by the following formula:

|

tax on page 1, line 3, Column C X ( $5,400 minus tax on page 1, line 3, Column C ) = ___________ |

||||||||

|

|

|

$2,000 |

|

|

(your credit) |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MAILING INSTRUCTIONS |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Attachcopiesoffederaland/orNewYorkStatechangesandexplanationofitems. |

|

ALLRETURNSEXCEPTREFUNDRETURNS |

|

|

REMITTANCES |

|

RETURNSCLAIMINGREFUNDS |

|

|

Makeremittancepayabletotheorderof NYCDEPARTMENTOFFINANCE |

|

NYC DEPARTMENT OF FINANCE |

|

|

|

NYC DEPARTMENT OF FINANCE |

||

|

PaymentmustbemadeinU.S.dollars,drawnonaU.S.bank. |

|

P.O. BOX 5564 |

|

|

AT NYC.GOV/ESERVICES |

|

P.O. BOX 5563 |

|

|

Toreceivepropercredit,youmustenteryourcorrectEmployerIdentification |

|

BINGHAMTON, NY |

|

|

OR |

|

BINGHAMTON, NY |

|

|

|

|

|

Mail Payment and Form |

|

||||

|

Numberand/orSocialSecurityNumberonyourtaxreturnandremittance. |

|

|

|

|

NYC DEPARTMENT OF FINANCE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

P.O. BOX 3646 |

|

|

|

|

|

|

|

|

|

|

|

|

|

60121591 |

|

|

|

|

|

NEW YORK, NY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

Page 3 |

|

|

IMPORTANT INFORMATION CONCERNING FORM

Payments may be made on the NYC Department of Finance website at nyc.gov/eservices, or via check or money order. If payingwithcheckormoneyorder,donotincludethesepaymentswithyourNewYorkCityreturn.Checksandmoneyorders

GENERAL INFORMATION

(Pursuant to Title 11, Chapter 5 of theAdministrative Code of the City of NewYork)

FortaxableyearsbeginningpriortoJanuary1,2015.

This form is to be used by unincorporated businesses for reporting adjust- mentsintaxableincomeresultingfromanInternalRevenueServiceauditof yourfederalincometaxreturn,and/orNewYorkStateDepartmentofTaxa- tion and Finance audit of your NewYork State income tax return and must be filed within 90 days after a final determinationor as required by the De- partmentofFinance. Itmustbeaccompaniedbytheamountofadditionaltax due. ExplainfederalorNewYorkStateadjustmentsindetailonScheduleA of this form and attach an exact copy of the entire report of federal and/or NewYorkStatefindings. Ifyoudisagreewiththeresultsofafinaldetermi- nationinafederalorStateaudit,completetheformshowingtheamountfrom column 1incolumn3,and attach a schedule showingthe additional tax(or refund)duereportingthechangesinaccordancewiththefinaldetermination andattachastatementexplainingwhyyoubelievetheadjustmentsareerro- neous. Ifnosuchstatementisattached,theamountoftheNewYorkCitytax resultingfromthefederalorStatedeterminationreportedonthisformasdue willbedeemedassessedonthedatethisformisfiled. Thisformistobefiled separately.Donotattachittoanytaxreturn.

Thisformisrequiredifthetaxpayerexecutesawaiverofrestrictions on assessments as provided in IRC section 6213(d) or NYS Tax Law section681(f).

AnamendedNewYorkCityreturnmustbefiledwithin90daysafter filinganamendedfederalorNewYorkStatereturn.

NOTE:

FortaxyearsbeginningonorafterJanuary1,2012,alltaxpayersmust allocateunincorporatedbusinesstaxableincomeusingformulaalloca- tion.Tax year2011 is the last taxable yearin which eligible taxpayers

ChangestotheUnincorporatedBusinessTaxineffectfortaxyearsbe- ginning on or after January 1, 2009, include: single factor allocation

For information regarding depreciation deductions for “qualified property,” “qualified New York Liberty Zone property,” “qualified New York Liberty Zone leasehold improvements” and "qualified ResurgenceZoneproperty"placedinserviceafterSeptember10,2001,

Forinformationregardingdepreciationdeductionsforpropertyplaced in service outside New York after 1984 and before 1994, see Finance

PreparerAuthorization: IfyouwanttoallowtheDepartmentofFinance todiscussyourreturnwiththepaidpreparerwhosignedit,youmustcheck the"yes"boxinthesignatureareaofthereturn.Thisauthorizationapplies onlytotheindividualwhosesignatureappearsinthe"Preparer'sUseOnly" section of your return. It does not apply to the firm, if any, shown in that section. Bycheckingthe"Yes"box,youareauthorizingtheDepartmentof Finance to call the preparer to answer any questions that may arise during theprocessingofyourreturn. Also,youareauthorizingthepreparer to:

lGive the Department any information missing from your return,

lCalltheDepartmentforinformationabouttheprocessingofyourre- turn or the status of your refund or payment(s), and

lRespondtocertainnoticesthatyouhavesharedwiththepreparer about math errors, offsets, and return preparation. The notices will notbe sent to the preparer.

You are not authorizing the preparer to receive any refund check, bind you to anything (including any additional tax liability), or otherwise rep- resent you before the Department. The authorization cannot be revoked, however, the authorization will automatically expireno laterthan the due date(withoutregardtoanyextensions)forfilingnextyear'sreturn. Fail- uretochecktheboxwillbedeemedadenialofauthority.

SPECIFIC INSTRUCTIONS

CALCULATION OFTAX

In ColumnAenter amounts from the latest NewYork City report or final New York City Department of Finance adjustment prior to the filing of this return. If you filed an amended return or if the amounts shown on your original return were changed pursuant to a final Department of Fi- nance adjustment, attach documentation reflecting the New York City changes and a schedule showing your calculations.

If you originally filed Form

LINE1

IncolumnAenterthesumoftheamountofthetotalbusinessincomeyou reported on line 1, ScheduleA, Form

In column B enter the net reportable changes from line 11 of ScheduleA on page 2 of this form.

In column C add or subtract the amount in column B from columnA.

LINE2

IncolumnAentertheamountoftaxableincomeyoureportedonline16of

LINES3through8

In column A enter the amount reported on the corresponding lines of Schedule A, Form

Form |

Page 4 |

|

|

nallyfiledorpreviouslyadjusted. IncolumnCrecalculatethoseamounts |

||

and enter appropriate amounts. For line 4, compute the revised business |

Theamountenteredonline5(columnF)shouldbethenetadjustmentsmade |

|

tax credit by completing Schedule B on page 2 of this form. |

by a federal or New York State audit before taking into consideration any |

|

NewYorkCitychangesapplicablethereto.Notethatarecomputationorre- |

||

visionofyourfederalorNewYorkStatereturnincreasingnetprofit(orloss) |

||

Interest on the additional tax due, entered in column D, line 10, is com- |

||

fromabusinessorprofessionorpartnershipincomereportedthereon,which |

||

puted from the due date of the original tax return to the date paid. Leave |

resultsinareductionofanoverpaymentorrefundclaimed,mustbereported |

|

columnD,line12blankiftheamountofinterestcomputedislessthan$1. |

on this form even though you receive a refund or overpayment credit fol- |

|

Theapplicableprescribedinterestrateorratesareavailablefromtheinter- |

||

estratetablesetforthontheDepartmentofFinance’sinternetwebsiteat: |

|

Fortherateofinterestonoverpayments,forarateofinterestnotshownontheweb- |

IfanyfederalorNewYork StateitemreportedincolumnFissubjecttoa |

||

modificationincreasingordecreasingthatitemforNewYorkCitytaxpur- |

|||

site and for interest calculations, call 311. If calling from outside of the five NYC |

poses pursuant to Section |

||

boroughs, please call |

|||

of NewYork, show the details and enter the NewYork City net change at |

|||

|

|

||

line 10. If a NewYork City business allocation percentage or investment |

|||

a) |

Alate filing penalty is assessed if you fail to file this form when |

allocation percentage is utilized, submit allocation schedule. |

|

|

due,unlessthefailureisduetoreasonablecause. Foreverymonth |

||

|

or partial month that this form is late, add to the tax (less any pay- |

||

|

ments made on or before the due date) 5%, up to a total of 25%. |

||

b) |

If this form is filed more than 60 days late, the above late filing |

ACCESSING NYC TAX FORMS |

|

|

penaltycannotbelessthanthelesserof(1)$100or(2)100%ofthe |

By Computer - Download forms from the Finance website at: |

|

|

amountrequiredtobeshownontheform(lessanypaymentsmade |

nyc.gov/finance |

|

|

by the due date or credits claimed on the return). |

||

|

|

||

c) |

Alatepaymentpenaltyisassessedifyoufailtopaythetaxshownon |

By Phone - call 311. If calling from outside of the five NYC boroughs, |

|

|

thisformbytheprescribedfilingdate,unlessthefailureisduetorea- |

please call |

|

|

sonablecause. Foreverymonthorpartialmonththatyourpaymentis |

Mail all returns, except refund returns: |

|

|

late,addtothetax(lessanypaymentsmade)1/2%,uptoatotalof25%. |

||

d) |

ThetotaloftheadditionalchargesinAandCmaynotexceed5%for |

NYCDepartmentofFinance |

|

|

any one month, except as provided for in B. |

P.O.Box5564 |

|

Ifyouclaimnottobeliablefortheseadditionalcharges,attachastatement |

|||

to your return explaining the delay in filing, payment or both. |

|||

|

|

||

or Mail payment and Form |

|||

|

|||

Where the federal or New York State change in business income would |

NYCDepartmentofFinance |

||

P.O.Box3646 |

|||

vided it is accompanied by a complete copy of the federal and/or New |

NewYork,NY |

||

York StateAudit Report or Statement ofAdjustment. |

|

||

EffectivefortaxableyearsbeginningonorafterJanuary1,1989,ifthisre- |

Returns claiming refunds: |

||

portisnotfiledwithin90daysafterthenoticeofthefinalfederal(orNew |

NYCDepartmentofFinance |

||

YorkState)determination,nointerestshallbepaidontheresultingrefund. |

|||

|

|

P.O.Box5563 |

|

SCHEDULEA |

|||

LINES1THROUGH4 |

|

||

PRIVACYACTNOTIFICATION |

|||

TheFederalPrivacyActof1974,asamended,requiresagenciesrequestingSocialSecurityNumbers |

|||

|

This is the amount of federal gross income from federal Schedule C, |

toinformindividualsfromwhomtheyseekthisinformationwhethercompliancewiththerequestis |

|

|

Form1040,lessdeductions. Therefore,anyfederalorNewYorkState |

voluntaryormandatory,whytherequestisbeingmade,andhowtheinformationwillbeused. Thedis- |

|

|

adjustmentaffectingnetprofit(orloss)fromabusinessorprofession |

||

|

mustbereportedonthisform,eventhoughthebusinessisnotsubject |

theAdministrativeCodeoftheCityofNewYork. Suchnumbersdisclosedonanyreportorreturnare |

|

|

requestedfortaxadministrationpurposesandwillbeusedtofacilitatetheprocessingoftaxreturnsand |

||

|

to federal or state tax. For example, the disallowance of a deduction |

toestablishandmaintainauniformsystemforidentifyingtaxpayerswhoareormaybesubjecttotaxes |

|

|

increasesnetprofitfromabusinessorprofessionandtheallowanceof |

administeredandcollectedbytheDepartmentofFinance,and,asmayberequiredbylaw,orwhenthe |

|

|

an additional deduction not claimed on the original return decreases |

taxpayer gives written authorization to the Department of Finance for another department, person, |

|

|

agencyorentitytohaveaccess(limitedorotherwise)totheinformationcontainedinhisorherreturn. |

||

|

net profit from a business or profession. |

|

|

AnyfederalorNewYorkStateadjustmentsmadetoitemsofincome, gain,lossordeductionaffectingpartnershipincomefromfederalForm 1065 or

Any Federal or NewYork State adjustments made to items of invest- mentincomeorlossoftheunincorporatedbusinessalsoshouldbere- ported here.