Please do not use this space

If this is your final return, please check here

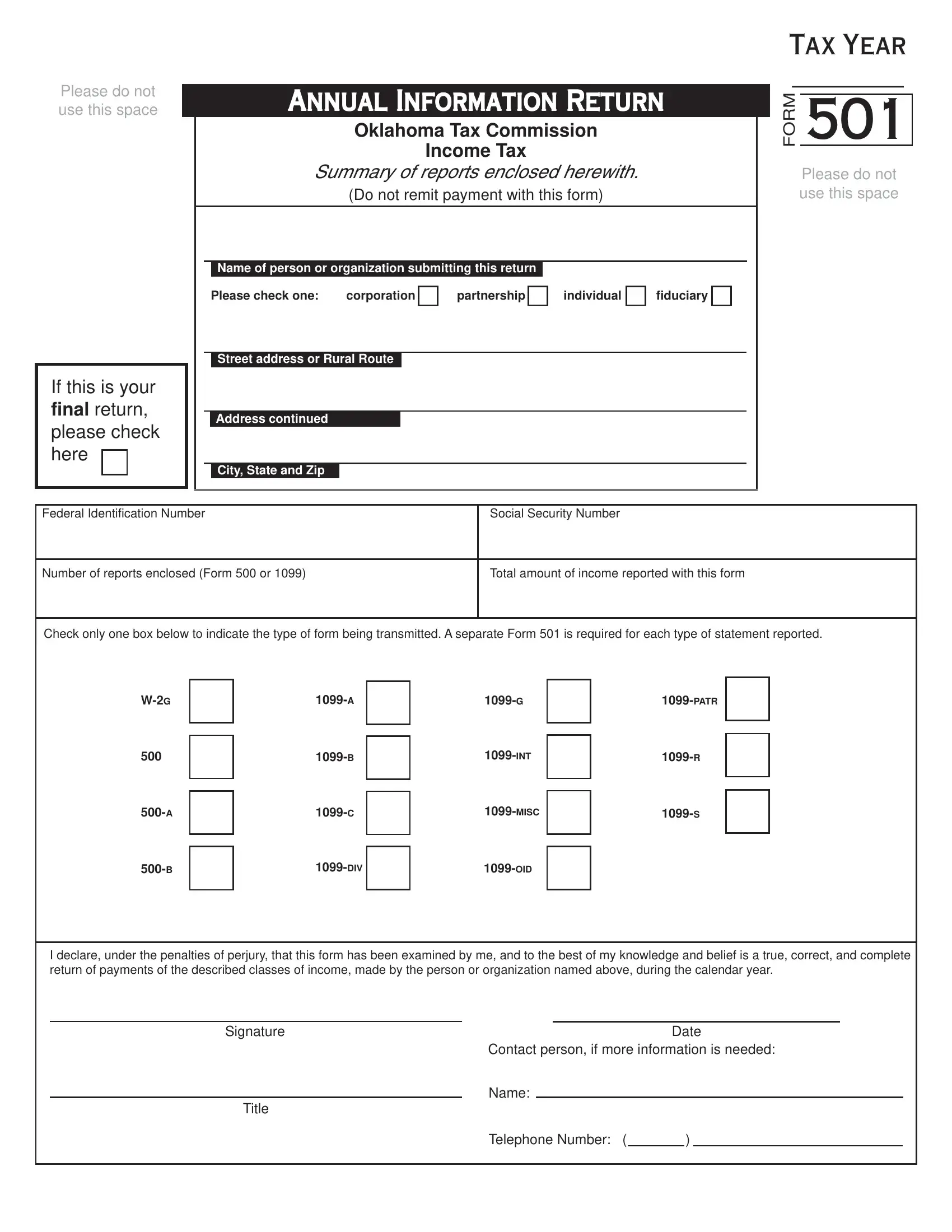

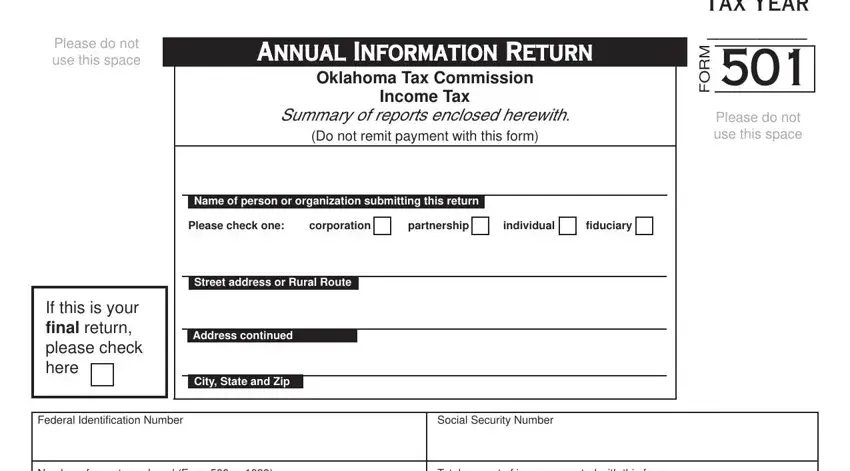

ANNUAL INFORMATION RETURN

Oklahoma Tax Commission

Income Tax

Summary of reports enclosed herewith.

(Do not remit payment with this form)

Name of person or organization submitting this return |

|

|

Please check one: |

corporation |

partnership |

individual |

fiduciary |

Street address or Rural Route

Address continued

City, State and Zip

TAX YEAR

________

FORM 501

Please do not use this space

Federal Identification Number |

Social Security Number |

|

|

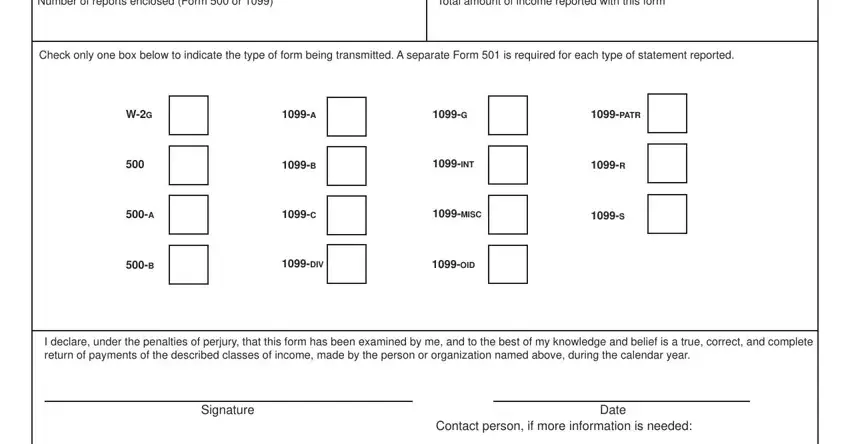

Number of reports enclosed (Form 500 or 1099) |

Total amount of income reported with this form |

|

|

Check only one box below to indicate the type of form being transmitted. A separate Form 501 is required for each type of statement reported.

W-2G |

|

1099-A |

|

1099-G |

|

1099-PATR |

500 |

|

|

|

1099-INT |

|

1099-R |

|

|

|

|

1099-B |

|

|

500-A |

|

1099-C |

|

1099-MISC |

|

1099-S |

|

|

|

|

|

|

500-B |

|

1099-DIV |

|

1099-OID |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I declare, under the penalties of perjury, that this form has been examined by me, and to the best of my knowledge and belief is a true, correct, and complete return of payments of the described classes of income, made by the person or organization named above, during the calendar year.

Signature |

Date |

|

Contact person, if more information is needed: |

|

Name: |

|

|

|

|

Title |

|

|

|

|

Telephone Number: ( |

|

) |

|

FORM 501 INSTRUCTIONS

WHO SHALL REPORT...

All payors, including but not limited to churches, charitable organizations, labor unions, lodges, fraternities, sororities, school districts, state, county and municipal departments, cooperatives and any other tax exempt organization, shall report these payments.

DUE DATES...

This return together with the reports enclosed must be forwarded so as to reach the Oklahoma Tax Commission before February 28 of the succeeding calendar year except where indicated below.

•Every remitter, required to withhold income tax from royalty payments made to nonresident royalty owners, shall furnish this return together with either Forms 1099-MISC or Forms 500-A to the Oklahoma Tax Commission by January 31 of the succeed- ing calendar year. Each person to whom such payment was made shall also be furnished either Form 1099-MISC or Form 500-A by January 31. Title 68 O.S. Section 2385.26.

•Every pass-through entity, required to withhold income tax from the Oklahoma share of income distributed to nonresident members, shall furnish this return together with Forms 500-B to the Oklahoma Tax Commission by the due date, including extensions, of the pass-through entity’s income tax return. Each person to whom such payment was made shall also be furnished Form 500-B by such date. Title 68 O.S. Section 2385.30.

PAYMENTS TO BE REPORTED WHEN PAID TO RESIDENTS...

All persons (individuals, trusts, estates, corporations and partnerships) acting as payor, and including lessees, mortgagors of real and personal property, employers, officers and employees of the state or any political subdivision thereof, should report the following payments when these payments amount to $750 or more in the calendar year: interest, rent, dividends, annuities, gambling winnings, or other fixed or determinable or periodical gains, profits or income.

PRODUCTION PAYMENT RULES (RESIDENT • NONRESIDENT)...

The Oklahoma Tax Commission requires the reporting of “production payments” made to individuals, corporations, partnerships, trusts or estates whether made to a resident or nonresident. For purposes of Title 68 O.S. 2369, production payments means payments of proceeds generated from mineral interests in this state, including, but not limited to, a lease bonus, delay rental, royalty and working interest payment, and overriding royalty interest payment. Income from real property should be reported only when the property is located within Oklahoma, whether the recipient is a resident or nonresident. Amounts to report: $750 or more except $10 or more for royalties. However, all payments with Oklahoma withholding must be reported. State code “OK” must be entered in box 17 of form 1099-MISC to designate that the property is located in Oklahoma. Do not remit payment with this form.

DIVIDEND OR INTEREST PAYMENTS...

Corporations paying to individuals interest on bonds, mortgages, deeds of trusts and other similar obligations or dividend payments, should report these when they exceed $100; other persons (individuals, trusts, estates and partnerships) should report interest payments of $750 or more, when paid to an individual. Brokers or agents in stocks, bonds, and security or stock transactions will report, on Form 500, the total amount of commodity or security sales or the total market value of the securities exchanged for the customer, when they were $25,000 or more in the calendar year. This includes banks which handle orders for depositors or custodian accounts.

NONRESIDENTS...

Persons making payments to nonresident individuals, partnerships, trusts, corporations or estates of fixed or determinable income, from property owned, business or trade carried on in Oklahoma or gambling winnings won in Oklahoma, totaling $750 or more in the calendar year should report such payments. Also see production payment rules for nonresidents.

PROFESSIONAL PAYMENTS...

Persons making payments to professional individuals should report them when they amount to $750 or more and are made to an Oklahoma resident or to a nonresident providing professional services within the State of Oklahoma.

PASS-THROUGH ENTITIES...

Oklahoma requires withholding from distributions made to nonresident members (partners, members, shareholders or beneficiaries) of pass-through entities (partnerships, S corporations, limited liability companies or trusts). Report the income distributed and the income tax withheld on Form 500-B.

GENERAL INFORMATION...

The foregoing instructions are in conformity with the provisions of the Oklahoma statutes, requiring information returns to be filed in accordance with rules and regulations prescribed and adopted by the Tax Commission. The Oklahoma Tax Commission is not required to notify taxpayers of changes in any state tax law.

MAILING ADDRESS...

Please forward this return and accompanying reports to: Oklahoma Tax Commission, 2501 North Lincoln Blvd., Oklahoma City, Oklahoma 73194-0009.