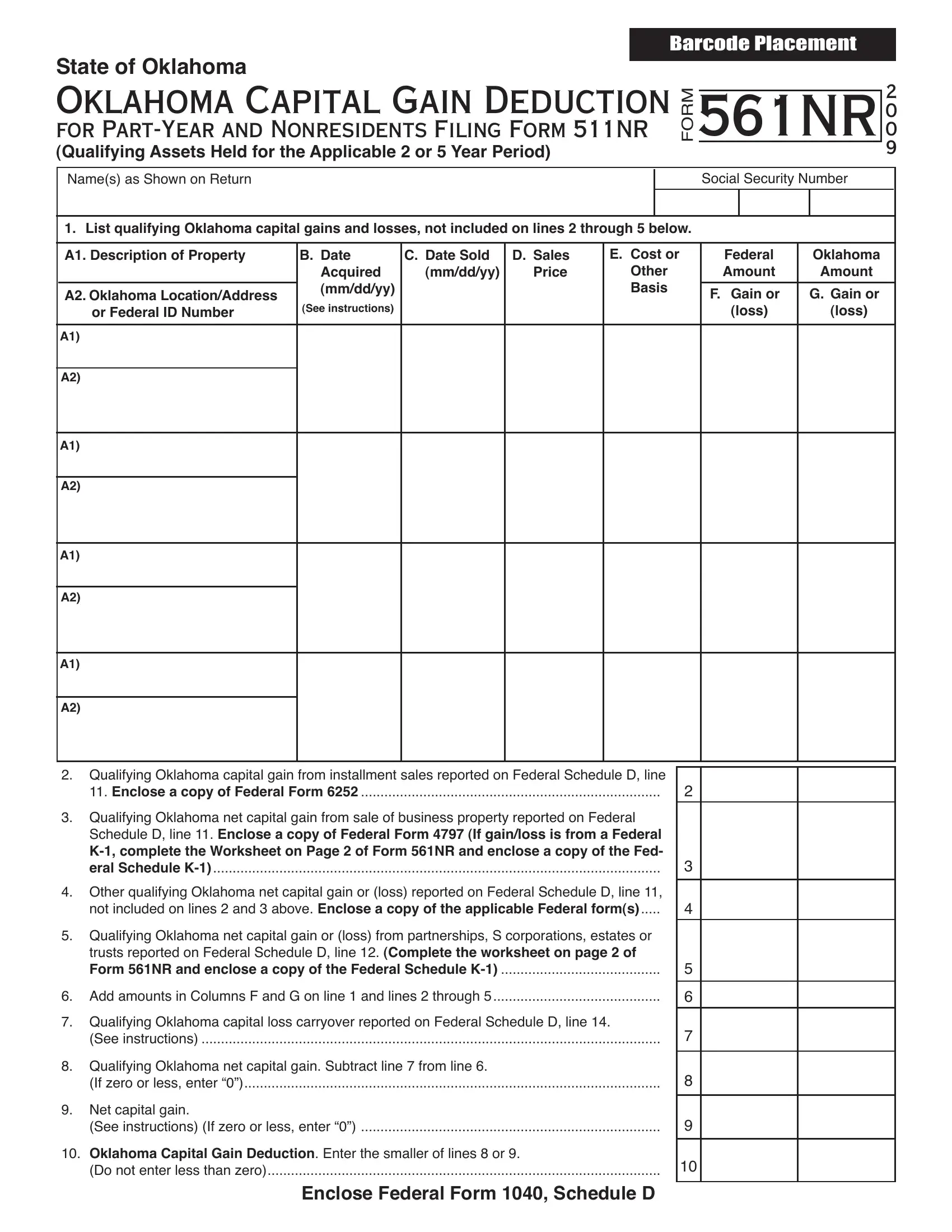

In the landscape of taxpayer obligations and benefits, the Oklahoma 561Nr form emerges as a significant document for part-year and nonresidents tasked with the intricacies of filing Form 511NR. This specific form serves a vital role in delineating Oklahoma capital gain deductions, encapsulating both the opportunity and the complexity inherent in tax reporting for qualifying assets held over stipulated periods—either two or five years. It meticulously outlines the steps to list qualifying Oklahoma capital gains and losses, with a nuanced approach to various categories of gains, including those from installment sales, sale of business property, among others. Moreover, the form extends into the realm of capital loss carryovers and how they intersect with Oklahoma net capital gains, highlighting the conditions under which taxpayers can mitigate their taxable income. Accompanied by sections that require the enclosement of Federal forms and adhering to specific instructions, the 561Nr form stands as a comprehensive guide for navigating the tax implications of capital gains and ensuring taxpayers accurately capture their eligibility for deductions within Oklahoma's tax framework. This document not only underscores the state's tax policy nuances but also reflects the broader challenges and responsibilities of tax reporting for individuals navigating the intricacies of residency and income sourcing.

| Question | Answer |

|---|---|

| Form Name | Oklahoma Form 561Nr |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | 511NR, K-1, oklahoma capital gain deduction, Barcode |

State of Oklahoma

BARCODE PLACEMENT

OKLAHOMA CAPITAL GAIN DEDUCTION

FOR

(Qualifying Assets Held for the Applicable 2 or 5 Year Period)

FORM

561NR

2

0

0

9

Name(s) as Shown on Return |

|

|

|

|

|

Social Security Number |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. List qualifying Oklahoma capital gains and losses, not included on lines 2 through 5 below. |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

A1. Description of Property |

B. Date |

C. Date Sold |

D. Sales |

E. Cost or |

Federal |

|

Oklahoma |

||

|

Acquired |

(mm/dd/yy) |

Price |

Other |

Amount |

|

Amount |

||

A2. Oklahoma Location/Address |

(mm/dd/yy) |

|

|

Basis |

F. Gain or |

|

G. Gain or |

||

|

|

|

|

|

|

||||

or Federal ID Number |

(See instructions) |

|

|

|

|

(loss) |

|

(loss) |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

A1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2.Qualifying Oklahoma capital gain from installment sales reported on Federal Schedule D, line 11. Enclose a copy of Federal Form 6252 .............................................................................

3.Qualifying Oklahoma net capital gain from sale of business property reported on Federal Schedule D, line 11. Enclose a copy of Federal Form 4797 (If gain/loss is from a Federal

4.Other qualifying Oklahoma net capital gain or (loss) reported on Federal Schedule D, line 11, not included on lines 2 and 3 above. Enclose a copy of the applicable Federal form(s).....

5.Qualifying Oklahoma net capital gain or (loss) from partnerships, S corporations, estates or trusts reported on Federal Schedule D, line 12. (Complete the worksheet on page 2 of Form 561NR and enclose a copy of the Federal Schedule

6.Add amounts in Columns F and G on line 1 and lines 2 through 5...........................................

7.Qualifying Oklahoma capital loss carryover reported on Federal Schedule D, line 14.

(See instructions) ......................................................................................................................

8.Qualifying Oklahoma net capital gain. Subtract line 7 from line 6.

(If zero or less, enter “0”)...........................................................................................................

9.Net capital gain.

(See instructions) (If zero or less, enter “0”) .............................................................................

10.Oklahoma Capital Gain Deduction. Enter the smaller of lines 8 or 9.

(Do not enter less than zero).....................................................................................................

2

3

4

5

6

7

8

9

10

Enclose Federal Form 1040, Schedule D

Form 561NR - Page 2

BARCODE PLACEMENT

OKLAHOMA CAPITAL GAIN DEDUCTION

FOR

Title 68 O.S. Section 2358 and Rule

Worksheet - (Enclose with Form 561NR)

Name(s) as Shown on Return

Social Security Number

FORM 561NR WORKSHEET FOR (CHECK ONE): LINE 3

OR LINE 5

Complete a separate worksheet for each piece of property sold. Enclose a copy of the Federal Schedule

Name of

Description of property sold: ______________________________________________________________________

Location of property: ____________________________________________________________________________

Date acquired: ______________________________________ Date sold: __________________________________

Date(s) you acquired ownership in the

General Information

Individual taxpayers can deduct qualifying gains receiving capital gain treatment which are included in Federal adjusted gross income. “Qualifying gains receiving capital treatment” means the amount of net capital gains, as deined under Internal Revenue

Code Section 1222(11). The qualifying gain must result from:

1.the sale of the real or tangible personal property located within Oklahoma that has been owned for at least ive uninter- rupted years prior to the date of the transaction that gave rise to the capital gain;

2.the sale of stock or an ownership interest in an Oklahoma company, limited liability company, or partnership where such stock or ownership interest has been owned for at least two uninterrupted years prior to the date of the transaction that gave rise to the capital gain; or

3.the sale of real property, tangible personal property or intangible personal property located within Oklahoma as part of the sale of all or substantially all of the assets of an Oklahoma company, limited liability company, or partnership or an Oklahoma proprietorship business enterprise where such property has been owned by such entity or business enter- prise or owned by the owners of such entity or business enterprise for a period of at least two uninterrupted years prior to the date of the transaction that gave rise to the capital gain.

An Oklahoma company, limited liability company, partnership or proprietorship business enterprise is an entity whose primary headquarters has been located in Oklahoma for at least three uninterrupted years prior to the date of sale.

A capital loss carryover from qualiied property reduces the current year gains from eligible property.

Capital gain from qualifying property, as described above, held by a

deduction, provided the individual has been a member of the

prior to the date of the transaction that created the capital gain. The type of asset sold, as shown in

whether the applicable number of uninterrupted years is two or ive. The

Installment sales...

Qualifying gains included in an individual taxpayer’s Federal adjusted gross income for the current year which are derived from installment sales are eligible for exclusion, provided the appropriate holding periods are met.

Speciic Instructions

Line 1:

List qualifying Oklahoma capital gains and losses from Federal Schedule D, line 8 or from Federal Schedule

Column A, line A1 enter the description of the property as shown in Federal Column A and on line A2 enter either the Oklahoma location of the real or tangible personal property sold or the Federal Identiication Number of the company, limited liability

Form 561NR - Page 3

OKLAHOMA CAPITAL GAIN DEDUCTION FOR

Title 68 O.S. Section 2358 and Rule

Speciic Instructions - continued

company or partnership whose stock or ownership interest was sold. Complete Columns B through F using the information from the corresponding columns of the Federal Schedule D or

In Column G enter the qualifying Oklahoma capital gains and losses reported in Column F which were sourced to Oklahoma on Form 511NR, line 7 “Oklahoma Amount” column.

Line 2:

Column F: If Federal Form 6252 was used to report the installment method for gain on the sale of eligible property on the Fed- eral return, compute the capital gain deduction using the current year’s taxable portion of the installment payment. Enclose Fed- eral Form 6252. Capital gain from an installment sale is eligible for the Oklahoma capital gain deduction provided the property was held for the appropriate holding period as of the date sold.

In Column G enter the capital gain from an installment sale of eligible property reported in Column F which was sourced to Okla- homa on Form 511NR, line 7 “Oklahoma Amount” column.

Line 3:

Column F: Enter the qualifying Oklahoma net capital gain from the Federal Form 4797 which was reported on Federal Schedule D. Enclose a copy of the Federal Form 4797. If reporting a gain/loss from a Federal Schedule

In Column G enter the other qualifying Oklahoma capital gain from Federal Form 4797 reported in Column F which was sourced to Oklahoma on Form 511NR, line 7 “Oklahoma Amount” column.

Line 4:

Column F: Enter other qualifying Oklahoma capital gains reported on Federal Schedule D, line 11. Enclose the applicable Fed- eral form(s). If not shown on the Federal form, enclose a schedule identifying the type and location of the property sold, the date of the sale, and the date the property was acquired.

In Column G enter the other qualifying Oklahoma capital gains reported in Column F which were sourced to Oklahoma on Form 511NR, line 7 “Oklahoma Amount” column.

Line 5:

Column F: Enter qualifying Oklahoma net capital gain or loss from partnerships, S corporations, trusts and estates. Complete the worksheet on page 2 of Form 561NR and enclose a copy of the Federal Schedule

In Column G enter the qualifying Oklahoma net capital gain or loss from

sourced to Oklahoma on Form 511NR, line 7 “Oklahoma Amount” column.

Line 7:

Column F: Enter the total qualifying Oklahoma capital loss carryover from the prior year’s return.

In Column G enter the qualifying Oklahoma capital loss carryover reported in Column F which was sourced to Oklahoma on Form 511NR, line 7 “Oklahoma Amount” column.

Line 9:

Column F: The Oklahoma capital gain deduction, in the “Federal Amount” column, may not exceed the net capital gain included in Federal adjusted gross income. The term “net capital gain” means the excess of the net

Column G: The Oklahoma capital gain deduction, in the “Oklahoma Amount” column, may not exceed the portion of the net capital gain sourced to Oklahoma. This is the net capital gain from Form 511NR, line 7 “Oklahoma Amount” column. If there is no net capital gain, enter “0”.

Note: The net capital gain must be decreased for any capital gain or increased for any capital loss from the sale of state and municipal bonds exempt from Oklahoma income tax.

Line 10:

Column F: Compare lines 8 and 9. Enter the smaller amount here and on Form 511NR, Schedule

Column G: Compare lines 8 and 9. Enter the smaller amount here and on Form 511NR, Schedule