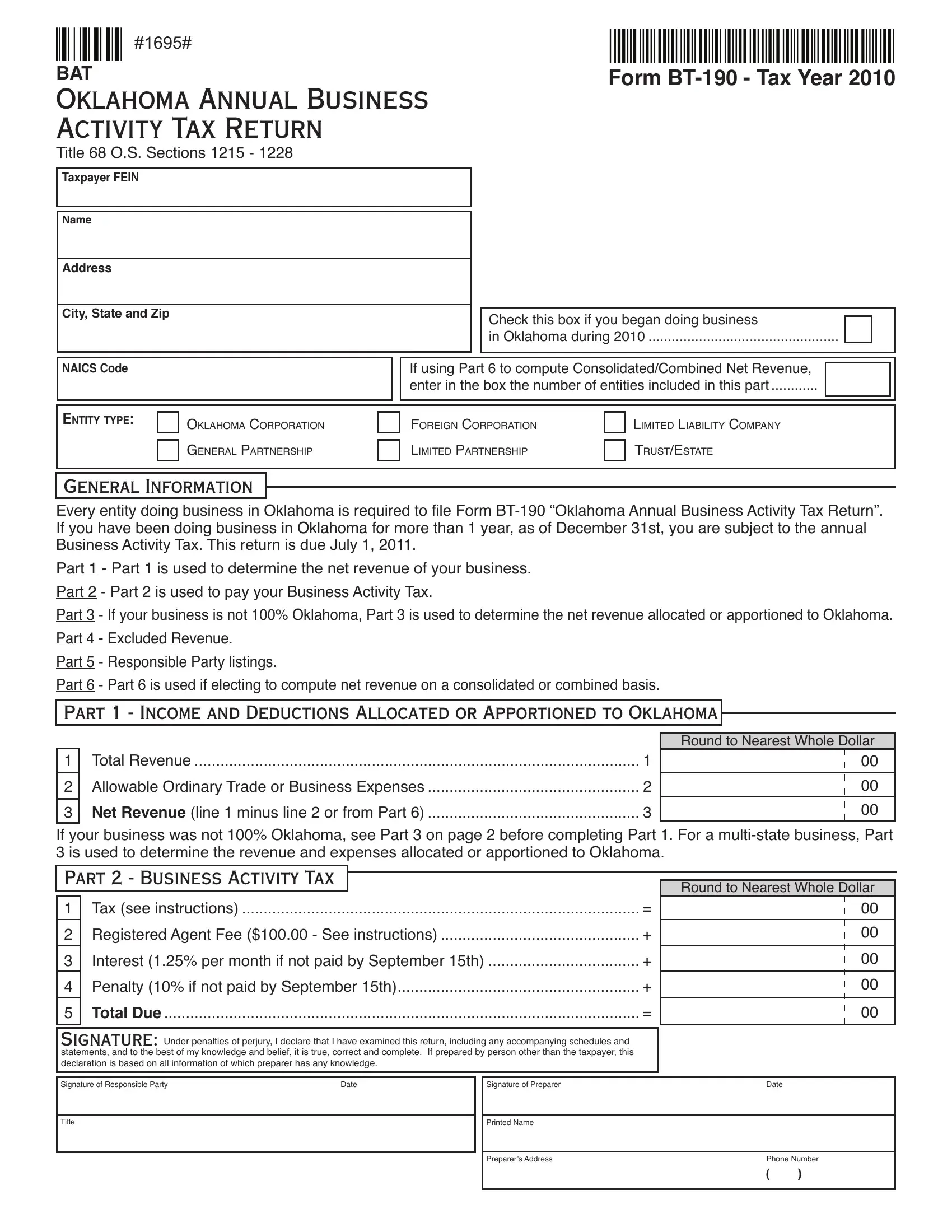

The Oklahoma BT-190 form, officially titled as the Oklahoma Annual Business Activity Tax Return, plays a critical role for entities conducting business within the state. Governed by Title 68 O.S. Sections 1215 - 1228, this mandatory document is intricately designed to capture the financial dynamics of businesses for a specific tax year, with the version at hand pertaining to the tax year 2010. Entities, regardless of their formation type—ranging from Oklahoma corporations, general partnerships, foreign corporations, limited partnerships, limited liability companies, to trusts or estates—are required to file this return if they have been operational in Oklahoma beyond a span of one year as of December 31st. This comprehensive form begins with Part 1 for determining the net revenue of the business, transitioning to Part 2 for the actual computation and payment of the Business Activity Tax (BAT). Subsequent sections like Part 3 assist businesses in allocating or apportioning their net revenue specifically for operations within Oklahoma, emphasizing on the multi-state business scenarios. Moreover, Part 4 addresses excluded revenue, ensuring certain types of income are properly documented and exempted from the tax calculation. Responsible party listings and an optional section for computing consolidated/combined net revenue round off this elaborate tax return instrument. Notably, the form concludes with necessary declarations and signature lines to uphold its integrity and validity, including declarations under penalty of perjury by the responsible party and the preparer, further emphasizing the form's significance in the state's taxation landscape.

| Question | Answer |

|---|---|

| Form Name | Oklahoma Form Bt 190 |

| Form Length | 6 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 30 sec |

| Other names | oklahoma bt 190, FEINs, Apportionment, 15th |