When you wish to fill out 4220 form, you don't have to download any software - simply make use of our online PDF editor. The editor is continually maintained by our team, getting awesome features and growing to be better. With a few basic steps, you can begin your PDF editing:

Step 1: Access the PDF form in our tool by clicking the "Get Form Button" above on this webpage.

Step 2: When you access the online editor, you'll notice the document ready to be filled out. Aside from filling in various blank fields, it's also possible to perform other sorts of actions with the file, including writing custom text, modifying the initial textual content, inserting images, putting your signature on the form, and much more.

This PDF will require particular info to be typed in, hence make sure to take the time to type in what's expected:

1. The 4220 form necessitates specific details to be inserted. Ensure that the following fields are filled out:

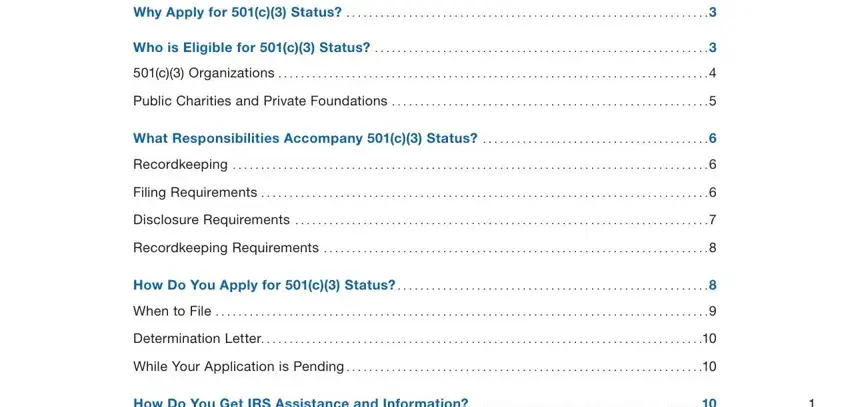

2. The next stage is usually to fill in these particular blank fields: Why Apply for c Status, Who is Eligible for c Status, c Organizations, Public Charities and Private, What Responsibilities Accompany c, Recordkeeping, Filing Requirements, Disclosure Requirements, Recordkeeping Requirements, How Do You Apply for c Status, When to File, Determination Letter, While Your Application is Pending, and How Do You Get IRS Assistance and.

Be very attentive when filling out Disclosure Requirements and Filing Requirements, since this is where many people make a few mistakes.

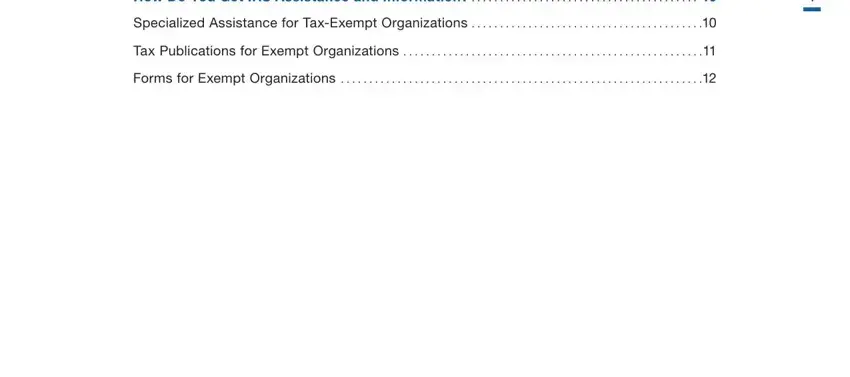

3. Completing How Do You Get IRS Assistance and, Specialized Assistance for, Tax Publications for Exempt, and Forms for Exempt Organizations is essential for the next step, make sure to fill them out in their entirety. Don't miss any details!

4. All set to begin working on this next segment! In this case you've got all of these exemption from federal income tax, Publication, TaxExempt Status for Your, and want to consult a tax adviser form blanks to fill out.

5. This pdf has to be concluded with this particular part. Further you will find an extensive set of blanks that need accurate information for your document submission to be complete: tions nondenominational ministries, may qualify for exemption These, Publication Tax Guide for, Public Charities and Private, Every organization that qualifies, For some organizations the primary, and Organizations statutorily.

Step 3: Before moving forward, double-check that form fields have been filled in right. The moment you establish that it's fine, click “Done." Obtain your 4220 form after you sign up for a 7-day free trial. Immediately view the pdf form within your FormsPal cabinet, together with any modifications and adjustments being conveniently synced! At FormsPal, we endeavor to guarantee that all your details are maintained private.