Are you looking for more information about the SC I295 Form? If so, this blog post is here to help! The SC I295 form is an application from the South Carolina Department of Motor Vehicles that can be used to apply or update existing driving privileges. In this post, we will discuss what information and documents are required when filling out the SC I295 Form, as well as how long it typically takes before you can receive your new license or updated driver's license. From start to finish, read on for a comprehensive guide on everything you need to know about this important DMV form.

| Question | Answer |

|---|---|

| Form Name | Sc I295 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | south carolina form i 295 instructions, sc form i 295, sc i 295, sc i 295 fillable |

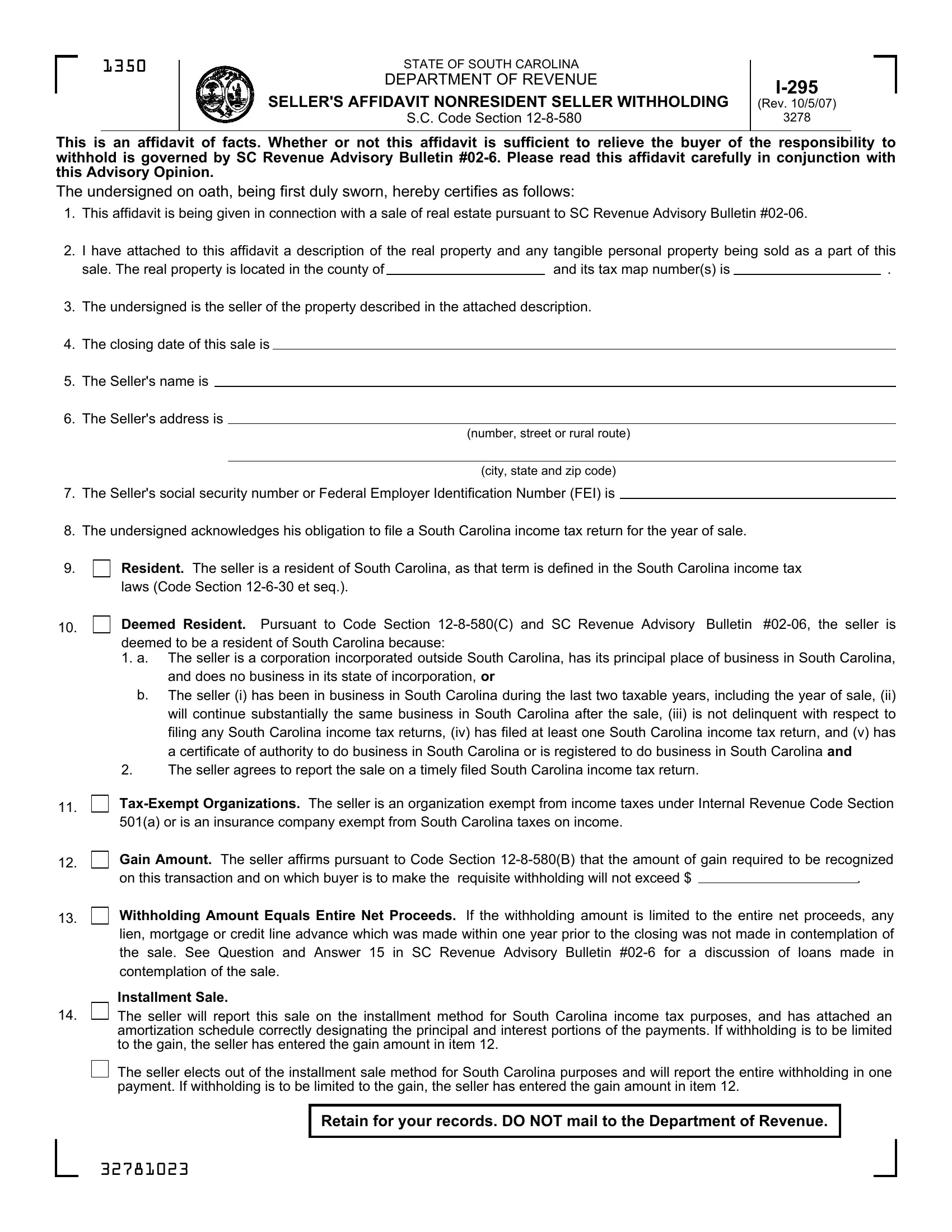

1350

STATE OF SOUTH CAROLINA

DEPARTMENT OF REVENUE

SELLER'S AFFIDAVIT NONRESIDENT SELLER WITHHOLDING

S.C. Code Section

(Rev. 10/5/07)

3278

This is an affidavit of facts. Whether or not this affidavit is sufficient to relieve the buyer of the responsibility to withhold is governed by SC Revenue Advisory Bulletin

The undersigned on oath, being first duly sworn, hereby certifies as follows:

1.This affidavit is being given in connection with a sale of real estate pursuant to SC Revenue Advisory Bulletin

2.I have attached to this affidavit a description of the real property and any tangible personal property being sold as a part of this

sale. The real property is located in the county of |

|

and its tax map number(s) is |

|

. |

3.The undersigned is the seller of the property described in the attached description.

4.The closing date of this sale is

5.The Seller's name is

6.The Seller's address is

(number, street or rural route)

(city, state and zip code)

7.The Seller's social security number or Federal Employer Identification Number (FEI) is

8.The undersigned acknowledges his obligation to file a South Carolina income tax return for the year of sale.

9.

10.

11.

12.

13.

14.

Resident. The seller is a resident of South Carolina, as that term is defined in the South Carolina income tax laws (Code Section

Deemed Resident. Pursuant to Code Section

1.a. The seller is a corporation incorporated outside South Carolina, has its principal place of business in South Carolina, and does no business in its state of incorporation, or

b.The seller (i) has been in business in South Carolina during the last two taxable years, including the year of sale, (ii) will continue substantially the same business in South Carolina after the sale, (iii) is not delinquent with respect to filing any South Carolina income tax returns, (iv) has filed at least one South Carolina income tax return, and (v) has a certificate of authority to do business in South Carolina or is registered to do business in South Carolina and

2.The seller agrees to report the sale on a timely filed South Carolina income tax return.

Gain Amount. The seller affirms pursuant to Code Section

on this transaction and on which buyer is to make the requisite withholding will not exceed $ |

. |

|

|

|

|

Withholding Amount Equals Entire Net Proceeds. If the withholding amount is limited to the entire net proceeds, any lien, mortgage or credit line advance which was made within one year prior to the closing was not made in contemplation of the sale. See Question and Answer 15 in SC Revenue Advisory Bulletin

Installment Sale.

The seller will report this sale on the installment method for South Carolina income tax purposes, and has attached an amortization schedule correctly designating the principal and interest portions of the payments. If withholding is to be limited to the gain, the seller has entered the gain amount in item 12.

The seller elects out of the installment sale method for South Carolina purposes and will report the entire withholding in one payment. If withholding is to be limited to the gain, the seller has entered the gain amount in item 12.

Retain for your records. DO NOT mail to the Department of Revenue.

32781023

15.

Principal Residence or Involuntary Conversion - Nonrecognition of Gain. The sale of the property will not be subject to taxes because of Internal Revenue Code Section 121 (sale of a principal residence) or Internal Revenue Code Section 1033 (involuntary conversions.) If the seller fails to comply with Section 1033, the seller acknowledges an obligation to file an amended South Carolina income tax return for the year of the sale.

16.

17.

Like Kind Exchange.

In a simultaneous exchange, the entire gain is deferred under Internal Revenue Code Section 1031.

A gain will be partially recognized. Enter the gain amount in item 12.

The gain is intended to be deferred under Internal Revenue Code Section 1031 using a qualified intermediary and the steps required by SC Revenue Advisory Bulletin

Employee Relocation. The transaction involves the sale of an employee's property which is being sold by an employer or relocation company in connection with the employee's transfer. For income tax purposes the sale is treated as a sale by the employer or relocation company.

The undersigned understands that this affidavit may be disclosed to the Department and that any false statement contained herein could be punished by fine, imprisonment, or both.

(Signature) |

(Name - Please Print) |

If the person making the affidavit is not the Seller, complete the following:

(Affiant's Social Security Number or FEI Identification Number)

(Affiant's number, street or rural route)

(Affiant's city, state and zip code)

SUBSCRIBED AND SWORN to

Before me this |

|

day of |

|

, year of

(Notary Public)

My Commission Expires:

Social Security Privacy Act Disclosure

It is mandatory that you provide your social security number on this tax form if you are an individual taxpayer. 42 U.S.C 405(c)(2)(C)(i) permits a state to use an individual's social security number as means of identification in administration of any tax. SC Regulation

The Family Privacy Protection Act

Under the Family Privacy Protection Act, the collection of personal information from citizens by the Department of Revenue is limited to the information necessary for the Department to fulfill its statutory duties. In most instances, once this information is collected by the Department, it is protected by law from public disclosure. In those situations where public disclosure is not prohibited, the Family Privacy Protection Act prevents such information from being used by third parties for commercial solicitation purposes.

Our Internet address is: www.sctax.org

32782021