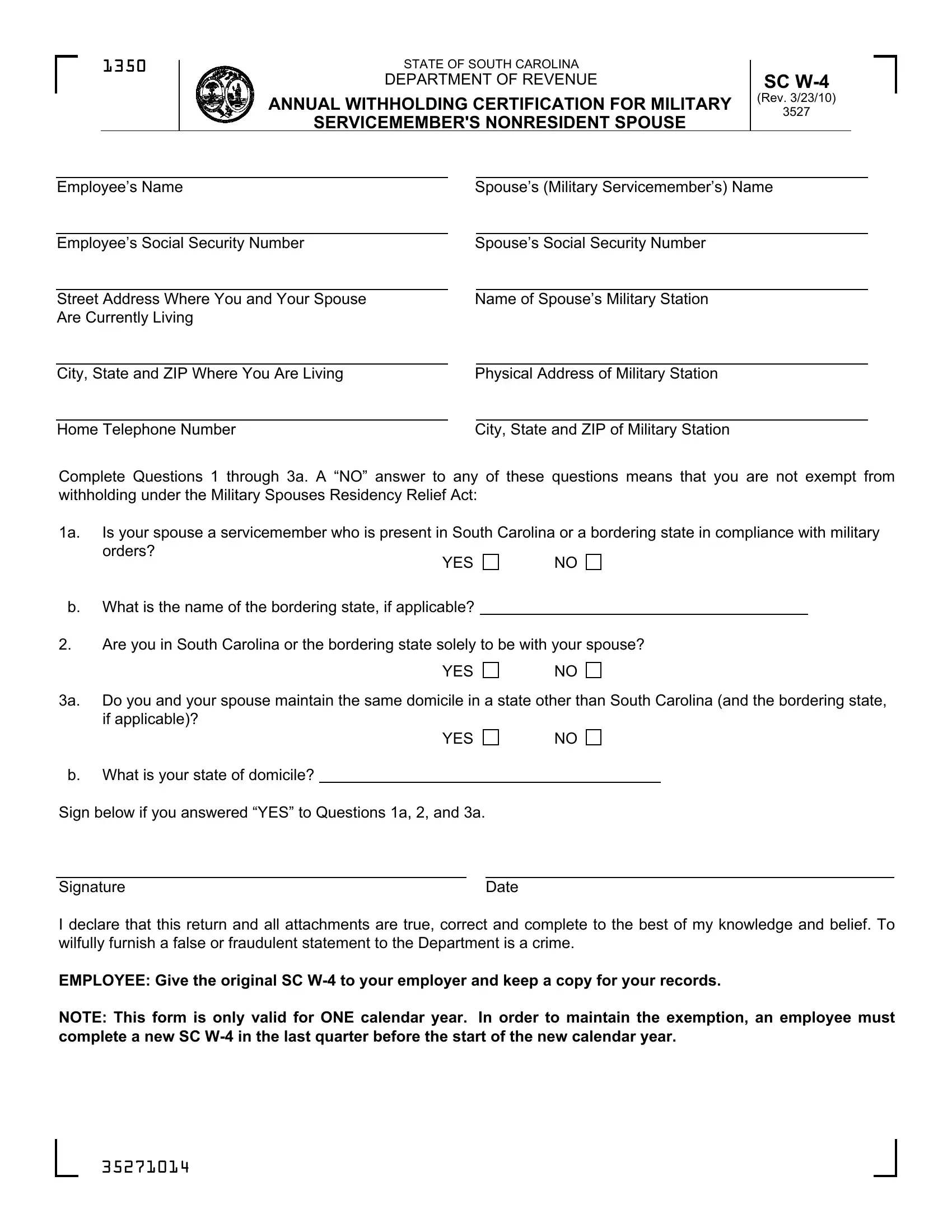

Understanding the complexities and legal requirements associated with tax forms is essential for individuals to ensure compliance and optimize their financial responsibilities. The SC W-4 form, issued by the State of South Carolina Department of Revenue, serves a very specific demographic: the nonresident spouses of military servicemembers. This form plays a crucial role in allowing these individuals to claim exemptions from South Carolina withholding tax each year, under specific conditions outlined by the Servicemembers Civil Relief Act, as amended by the Military Spouses Residency Relief Act. The form requires detailed information about the servicemember and their spouse, including their names, social security numbers, current living address, and the physical address of the military station. Critical to obtaining the withholding tax exemption, the form asks several eligibility questions that the filer must answer accurately; a misstep here could result in loss of eligibility for the exemption. Additionally, the document informs about the annual nature of this exemption, the conditions under which the SC W-4 becomes invalid, and the steps required for revocation should the spouse's exempt status change. It underscores the employer's responsibilities in verifying the exemption's legitimacy and retaining pertinent documentation, highlighting the importance of both employer and employee diligence in maintaining compliance. This form, therefore, not only facilitates tax compliance but also represents a targeted fiscal consideration for the unique circumstances faced by military families, effectively acknowledging and addressing their mobility and residency challenges.

| Question | Answer |

|---|---|

| Form Name | Sc W 4 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | sc tax withholding form, sc w4 2019, sc state tax withholding form, south carolina w4 form 2019 |

1350

STATE OF SOUTH CAROLINA

DEPARTMENT OF REVENUE

ANNUAL WITHHOLDING CERTIFICATION FOR MILITARY

SERVICEMEMBER'S NONRESIDENT SPOUSE

SC

(Rev. 3/23/10)

3527

Employee’s Name

Employee’s Social Security Number

Street Address Where You and Your Spouse Are Currently Living

City, State and ZIP Where You Are Living

Home Telephone Number

Spouse’s (Military Servicemember’s) Name

Spouse’s Social Security Number

Name of Spouse’s Military Station

Physical Address of Military Station

City, State and ZIP of Military Station

Complete Questions 1 through 3a. A “NO” answer to any of these questions means that you are not exempt from withholding under the Military Spouses Residency Relief Act:

1a. Is your spouse a servicemember who is present in South Carolina or a bordering state in compliance with military orders?

YES |

NO |

b.What is the name of the bordering state, if applicable?

2.Are you in South Carolina or the bordering state solely to be with your spouse?

YES

NO

3a. Do you and your spouse maintain the same domicile in a state other than South Carolina (and the bordering state, if applicable)?

YES

NO

b.What is your state of domicile?

Sign below if you answered “YES” to Questions 1a, 2, and 3a.

Signature |

Date |

I declare that this return and all attachments are true, correct and complete to the best of my knowledge and belief. To wilfully furnish a false or fraudulent statement to the Department is a crime.

EMPLOYEE: Give the original SC

NOTE: This form is only valid for ONE calendar year. In order to maintain the exemption, an employee must complete a new SC

35271014

Purpose of SC

Expiration of SC

Revocation of SC

Employer’s Responsibilities.

An employer is not exempt from its withholding requirements unless the employee completes federal Form

Photocopy of servicemember’s latest Leave and Earning Statement. An employee claiming this exemption must provide an original of the servicemember’s latest Leave and Earning Statement (LES). The LES assignment location must match the information provided on SC

Photocopy of Employee’s Military ID Card. An employee claiming this exemption must provide an original of the employee’s current Military Identification Card, identifying the employee as a military spouse. Military Identification Cards are issued every four years. Therefore, a Military Identification Card that is more than four years old does not meet this requirement.

Employee’s Completed SC

See SC Temporary Revenue Ruling

Social Security Privacy Act Disclosure

It is mandatory that you provide your social security number on this tax form. 42 U.S.C 405(c)(2)(C)(i) permits a state to use an individual's social security number as means of identification in administration of any tax. SC Regulation

The Family Privacy Protection Act

Under the Family Privacy Protection Act, the collection of personal information from citizens by the Department of Revenue is limited to the information necessary for the Department to fulfill its statutory duties. In most instances, once this information is collected by the Department, it is protected by law from public disclosure. In those situations where public disclosure is not prohibited, the Family Privacy Protection Act prevents such information from being used by third parties for commercial solicitation purposes.