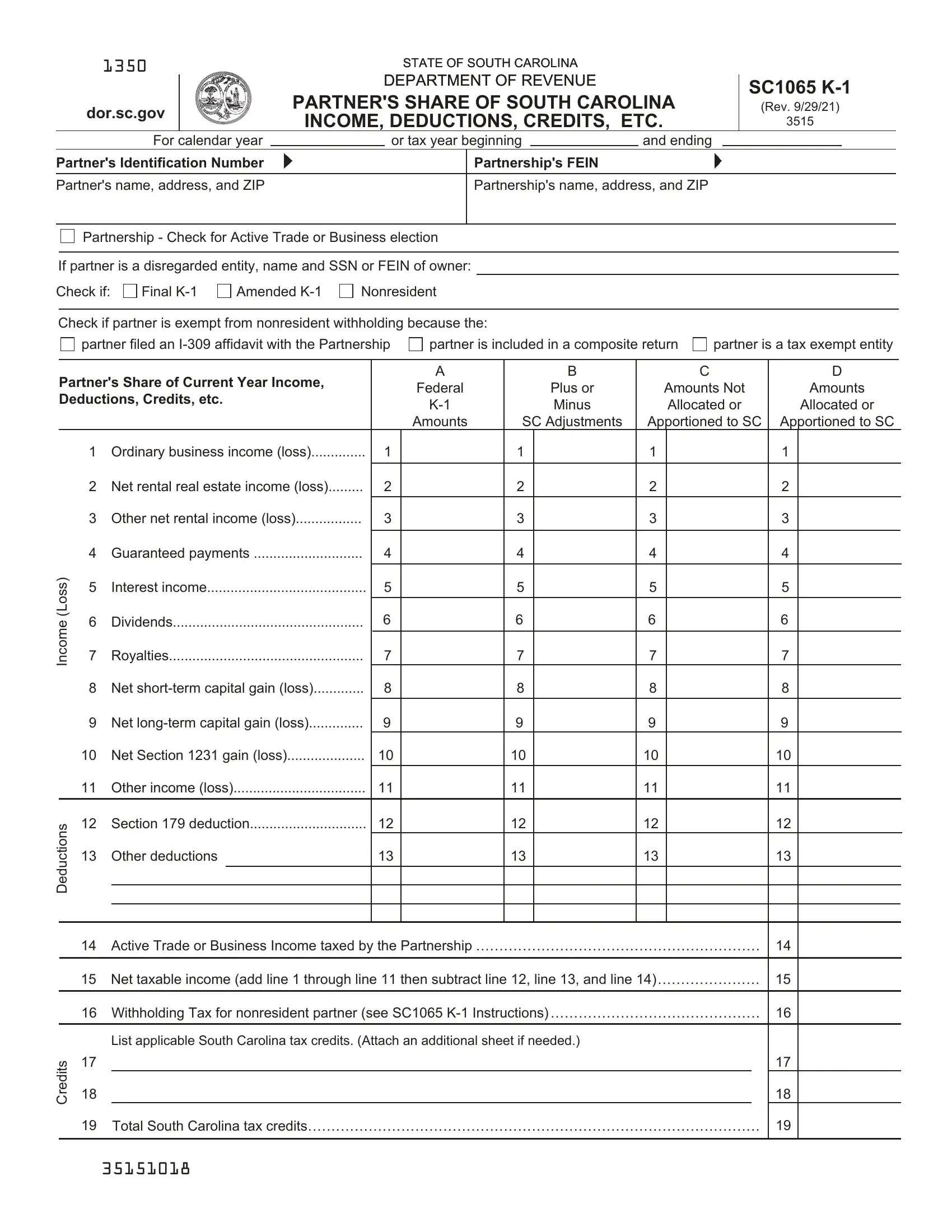

The SC1065 K-1 form, revised on June 15, 2020, by the South Carolina Department of Revenue, outlines a partner's share of income, deductions, credits, etc., from the partnership's operations that are allocated or apportioned to South Carolina or to other states. The form is a critical document for partners to understand their tax obligations and benefits related to their share of the partnership's operations. It begins with the partner’s identification details and includes comprehensive sections for reporting ordinary business income or loss, net rental real estate income, interest income, dividends, and various other types of earnings and losses. Guaranteed payments to partners, as well as the partner’s share of federal plus adjustments to income, allocated to South Carolina and other states, are meticulously detailed. Moreover, the form addresses partnership requirements for withholding tax on nonresident partners, signifying the state’s effort to ensure tax compliance. Furthermore, it details the steps for reporting South Carolina tax credits, underlying the state's tax provisions and incentives for businesses. Clear instructions are provided for both partnerships and partners, emphasizing the importance of accurate reporting and submission of the SC1065 K-1 forms along with the partnership return and how partners should incorporate this information into their personal tax filings. The document also touches on mandatory legal disclosures regarding the use of Social Security Numbers and the protections afforded to personal information under the Family Privacy Protection Act, epitomizing the balance between stringent tax administration and individual privacy rights.

| Question | Answer |

|---|---|

| Form Name | Sc1065 K 1 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | sc 1065 k 1, sc1065 form 2019, sc sc1065 k1, 2020 sc k 1 |